As Warren Buffett was closing in on age 60 in 1989, his net worth was $3.8 billion according to the Forbes List. This year, as Buffett approaches his mid-80s, he’s worth $58.5 billion. That means nearly 94% of Buffett’s current net worth was created after his 60th birthday.

I’ll come back to these facts again after we go through a simple example.

Most retirement calculators offer you fairly simple inputs. You basically enter in the amount you currently have saved, your future saving projections and a return assumption. Then the calculator spits out a future value based on those assumed inputs.

This isn’t a perfect way to determine exactly how much money you will have saved up by retirement because it’s impossible to precisely map out the future when the markets and your life are in a constant state of flux. That’s why retirement planning is more about accuracy (in the ballpark) than precision (bulls-eye).

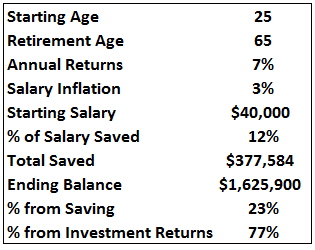

With that in mind, here are some basic assumptions for a hypothetical young person with a long time horizon ahead of them that you might see in a typical retirement calculator:

You can see that a steady diet of a double-digit savings rate coupled with decent investment returns and a healthy dose of compound interest can turn our hypothetical saver into a millionaire by the time they retire.

Looking at these numbers would lead you to believe that your investment returns carry the bulk of the weight, considering almost 80% of your ending balance comes from compounded investment gains.

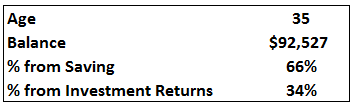

But breaking out these results by different periods tells us a much different story. Here’s how things look by age 35:

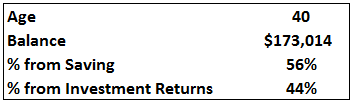

And again at age 40:

Ten and Fifteen years in and the amount you save is still the most important factor in this portfolio’s growth. In fact, it’s not until somewhere between the ages of 43 and 44 that our retirement saver sees investment gains overtake the amount they have saved over time.

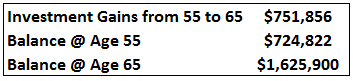

So in this example, it takes almost 20 years for investment returns to take over from the amount saved. And here’s a little secret about the compound interest in these retirement calculations — the majority of the growth comes once a large balance gets built up as you get closer to actual retirement age. Here’s the growth in the final decade before retirement using my assumptions:

Remember, in this example, this person continues to save right up until retirement, but the performance doesn’t really start to build the balance until there the law of large numbers comes into play.

This is where the Buffett example from the above comes into play. Obviously, it’s a bit of an obnoxious comparison because Buffett is one of the richest people in the world. But this does show that saving money slowly can build upon itself until all of the sudden compound interest explodes.

This is where real wealth comes from. It takes time and it’s not easy. It could take decades to see extraordinary results, which is much longer than most people would like. As life expectancy continues to increase the virtue of patience and an understanding of your time horizon become more important than ever.

A few more lessons from this basic example:

- It’s more exciting to focus on milking a few extra basis points of investment returns out of the financial markets, but this shows that the amount you save in the first few decades of your career is much more important for all but the very best investors.

- Increasing the % of salary saved in this example from 12% to 15% has nearly the same effect on the ending balance as increasing investment performance by 1% a year. Up the amount saved to 20% of salary and it equates to an extra 2% a year in market returns. Based on decades of academic research, earning more in the markets is much more difficult than saving more money.

- Markets don’t give you the same returns year-in and year-out like you see in retirement calculators and this illustration. Nothing moves in a straight line. Average market performance is anything but average. Since you have no control over total market returns or the sequence of those returns (which also plays a huge role in your ending balance at retirement) you must focus your energy on that which is within your control.

- That means how much money you save is much more important than most investors assume. Your initial returns as you start out definitely help plant the seeds, but the greatest investment strategy in the world means nothing if you have no capital to invest in it.

- Deconstructing compound interest into different time frames shows the power of sticking with a long-term plan. It may seem like every tick in the market is going to make or break your portfolio, when in reality the fairly simple action of saving more money can have an enormous impact on the size of your portfolio.

[…] Savings Trump Investing […]

As a financial advisor (and the author of a monthly magazine article on personal finance), I enjoy reading your common-sense ideas for wealth-building. This post is one of the best I’ve read so far. Thanks for sharing it.

Mike Rich

Pontchartrain Investment Management

Thanks Mike. I appreciate the feedback.

Another way of looking at this phenomenon is that longer your investment horizon, the larger the opportunity cost of consumption. While the price may be the same, the opportunity cost of buying something when you are young is vastly greater than when you are old.

Drive a used Honda when you are 25 so you can drive a new Mercedes when you are 60.

Great point. I’m a huge advocate for saving money and think that you are really helping out your future self. Has to be a balance of having some fun now but not over-doing it to the detriment of your future Benz.

I love #2. Totally agree. Saving gets you the best return on your money over the long term. Period.

Right, but I don’t want to completely trivialize the investing side of things. You still need to take risks to be able to earn those compounded returns. You can’t simply sit on a savings account and expect to get rich.

[…] When Saving Trumps Investing (Wealth of Common Sense) […]

Warren Buffet didn’t increase his wealth from 3B to 58B by keeping his money in a .5% savings account. His stake in Berkshire increased his wealth due to investing. I understand you are talking about the benefits of compounding, and I agree wholeheartedly, but perhaps Buffet wasn’t the best example to use.

I think you missed the point. You can’t earn those compounded returns in savings account no matter how much you save. You still have to take risk. That’s why the return assumption is 7%. Without taking risk (investing in stocks) you’ll never be able to compound your savings.

Great article and good points right there.It really is amazing what those two — saving and investing — can do to one’s finances.

[…] When Saving Trumps Investing – A Wealth of Common Sense […]

[…] When savings trumps investing. (A Wealth of Common Sense) […]

[…] When saving trumps investing – A wealth of common sense […]

[…] Courtesy of AWealthofCommonSense.com: […]

Excellent post! thank you for such a great articulation of TVM and it’s power. I think this concept is not universal knowledge for most people and it should be. You give me great conversation ideas for clients and I really appreciate it

You’re right. Too many people try for the easy way out instead of the slow and steady.

I’m glad to hear that you’re finding good talking points here. Thanks for the feedback.

[…] Remember — in most cases saving trumps investing. […]

[…] (3) Calculate investment performance. This one seems obvious, but it’s something that most investors don’t do. One study showed that investors overestimate both their absolute and relative performance to the market by an average of 5% a year, so it’s a good way to keep your ego in check. Calculating performance numbers allows you to see how much of your change in market value is driven by investment performance versus how much is due to the money you save. […]

I love your columns and agree with your main points. It’s very important advice. But I did want to say that those totals are just not right or misleading regarding the amounts. I realize that there are different ways of counting things and you are just doing a quick calculator, apparently in nominal terms (though they still don’t add up to me). But for what it’s worth, if you assume 3% inflation and further assume that the man earns $40K per year with even a 3% real raise (6% nominal), and then further assume that he contributes 12% each year based on his new salary every year (which is going up 6% nominal, annually), then you you see a total–in today’s dollars–of $721,761 at the end of his 64th year. He’s not really a millionaire by today’s standards, but that is a lot of money. And this does not contradict your main point I don’t think. He contributes $361,924 in today’s dollars over his lifetime. This means $359,387 in today’s dollars is earnings (50%). For what it’s worth.

Yes these are nominal results. Yes, inflation is a huge risk over the long-term. And obviously that nominal value won’t buy a person nearly as much in the future.

$1.625 million today is only worth $265K in 1970 dollars. But does that mean that someone that started saving in 1970 is worse off today because their money isn’t worth as much now because of inflation?

Of course inflation effects how much each dollar buys you over time. I don’t see what you’re getting at here.

[…] week I found an interesting post on the A Wealth of Common Sense blog called “When Saving Trumps Investing” that reminded me how important it is to continue saving money even while you’re investing. […]

This is a great article. The UK government now forces employers to automatically enrol workers into a workplace pension scheme if they are aged between 22 and tate Pension age earn more than £10,000 a year.

This enourages young people to actively consider their retirement, which let’s face it, isn’t a top priority for young people.

Of course investing a managed pension scheme and playing the markets yourself are two completely different things.

Now if only I could get back thouse 7 years I’ve missed by not saving/investing 😉

I hadn’t heard that before. Thanks for sharing. Unfortunately, some people need to be forced to do this to make it stick. People don’t realize how important it is until later in life.

[…] Click here to read! […]

[…] Further Reading: Putting Passive Inflows Into Context When Saving Trumps Investing […]

[…] Reading: When Saving Trumps Investing A Simple Way to Reduce Portfolio […]

[…] Further Reading: When Saving Trumps Investing […]