“The goal of the advisor shouldn’t be to beat the market by picking stocks or winning funds. Advisors add value by providing the discipline required for successful investing. They add value in areas like tax efficiency, risk management, estate planning and retirement planning.” – John Bogle

Investors on Wall Street are obsessed with beating the market. And usually when we talk about “the market” it means the S&P 500. The S&P 500 is simply a stock market index weighted by market capitalization of 500 of the largest publicly traded companies.

Based on historical active mutual fund performance, beating this simple index can prove to be quite difficult. According to the latest S&P SPIVA Scorecard report, over 80% of large cap funds failed to beat the S&P 500 in the past 5 years. Over longer time frames, the numbers get even worse.

The easy solution here would be to invest in the Vanguard 500 index fund (VFINX) and pay ridiculously low fees to basically equal the performance of the S&P 500.

But is another way to beat the 500 index fund over the long-term…simply invest in the Vanguard Total Stock Market Index Fund (VTSMX).

While the S&P 500 index fund holds only large companies, the total stock market fund holds small and medium sized companies as well.

Historically, there has been a premium on small and mid cap stocks over their larger brethren. Currently, VTSMX has about 72% in large caps, 19% in mid caps and 9% in small caps.

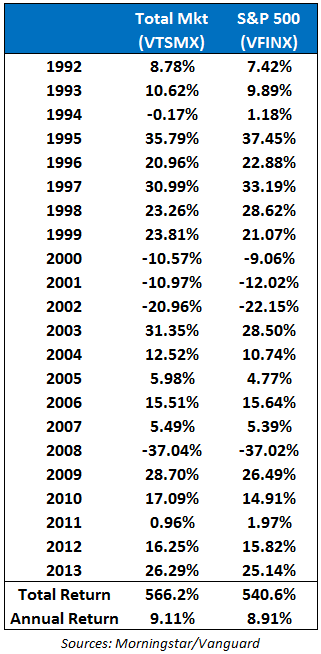

Here are the performance numbers for these two funds going back to 1992 when the fund was started through October 31, 2013:

The total market fund outperformed the 500 fund in 13 of the 22 years or about 60% of the time. The outperformance isn’t huge, at 0.20% per year, but if you started in 1992 with $50,000 invested in each fund you would have almost $14,000 more in the total market fund by 2013.

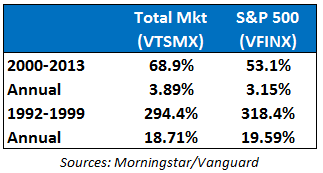

These funds are cyclical, so there can be long periods of time when one fund or the other looks better on a relative basis. Here are the returns broken down into the two longest cycles:

Investors went bonkers for large cap stocks in the 1990s so they outperformed small and mid caps stocks. But since 2000 the trend has reversed and small and mid caps have led the outperformance of the total market fund.

It’s difficult to tell when these trends will end but you could make the case that small and mid cap stocks are getting pricey when compared to large cap stocks at the moment.

But over very long time frames, the riskier small and mid cap stocks have historically added to performance (see Why Diversification Works).

The point of this exercise is not necessarily that you should choose between either of these two funds for investment purposes (although you could do much worse than simply holding these funds for the long haul).

The point is that you should be skeptical when a financial advisor or investment manager claims to consistently “beat the market.”

You need to make sure they are benchmarking your performance correctly instead of just showing you your results against a single index that could have a very different make-up than your actual portfolio.

Adding smaller companies as well as value stocks has been shown to increase stock returns historically, but they could also increase the risk of your portfolio. Your results are not only a factor of your returns, but also of the amount of risk you take.

I think benchmarking is important to make sure you aren’t overpaying for sub par investment advice, but it shouldn’t be the only way you measure your portfolio.

Most advisors and wealth managers assume it’s their job to beat certain benchmarks to prove their worth. They would have more success if they focused on achieving the goals of their clients instead of consistently trying to measure themselves against the market.

The focus should be on lowering costs, ignoring short-term noise in the markets, thinking long-term and emphasizing process over outcomes.

If the goal is only to beat the market (outcome) you can lose sight of your overall goals (process).

Source:

SPIVA Scorecard

Thank you for all interesting information about investment. I would like to see if you can help me with some question that I have. I have a portfolio that include three funds:

Fidelity Spartan total market

fidelity Spartan international

Fidelity Spartan U.S. Bond

Now my wife portfolio include include only two funds:

Fidelity Spartan Extended market

Fidelity Spartan Short Term bond

My question is that the fidelity extended market that my wife own is already include on my portfolio, fidelity total market, that include mid cap and small cap, like you already said. The way I see it is that my wife and I like to put more weight on mid cap and small cap. Do you think this wrong? My wife also have the fidelity short term bond, because I told her it would be a better choice in case interest rate rise, short term bonds would be safer.Also I thinking if it would be a better choice for for my wife to pick a high income bond fund (junk bond) like fidelity capital & income, but that probably to risky. Your attention to this matter will greatly be appreciated.

It all depends on your risk profile and time horizon. If you can stomach the potential wider swings in price from small & mid caps then it has made sense in the past to have more in these funds for the larger returns. You just have to understand that they can have larger losses at times as well.

Your extended mkt fund adds additional exposure to small & mid caps that you already have in the total market fund.

For high yield, just remember that those are typically the riskiest bonds and compensate you with higher returns along with higher risks. Again, you have to make sure you are comfortable investing in HY over the long term before making that decision. The risk profile for HY is actually closer to stocks than it is to bonds.

As long as you understand the risks involved in these asset classes and plan to hold them for the long term (or rebalance occasionally) you should be able to add them to your portfolio. Just remember that risk and return are joined at the hip. You don’t get one without the other.

[…] is a huge distinction for those that try to beat the market on a regular basis. This isn’t something you can just learn overnight either. It takes time, […]

[…] Reading: How to beat the market over 20 years Why diversification […]

Our company recently switched 401k plans to Vanguard, so I can invest in those funds now, which obviously I do.

But only a portion.

Other money I invested in an income funds paying 3.6% dividends. i believe with those dividends I can get better results.

Good move by your employer. 401k fees can be outrageous and Vanguard is one of the lowest fee providers. Sounds like the index funds can at least be a diversifier for your dividend stocks and funds.

Definitely it is a diversifier, so I also invested in some sectors as well and one income oriented fund.

[…] Beating the market is nice if you can do it, but it shouldn’t be very high on the list of goals for your investment plan. […]