“The future ain’t what it used to be.” – Yogi Berra

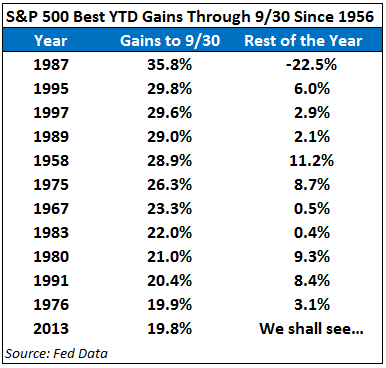

Despite a correction in the works because of those lovely politicians in DC, 2013 continues to be a great year for US stocks. The S&P 500 was up nearly 20% through the end of September.

I thought it would be interesting to see where that would put this year’s returns historically. Here’s a list of the best returns through September 30 since 1956 for the S&P 500:

With stocks at all-time highs and two large crashes in the rearview mirror, many investors seem to be predicting or even waiting for the next shoe to drop. And you can see that in 1987, that’s exactly what happened. Stocks got crushed in the 4th quarter after rising so far so fast (although almost all of that loss came on one day – Black Monday).

The rest of the years don’t look that bad though. In fact, out of the ten best years up to the end of the 3rd quarter, nine times the market continued its move higher. I’m not here to make a prediction…just trying to put things in a historical context. We could crash and burn or continue to climb the wall of worry.

The interesting thing about the markets is that no one really knows.

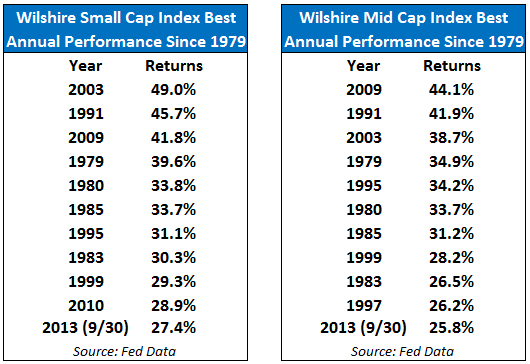

SMALL & MID CAP STOCKS CONTINUE TO DOMINATE

The S&P 500 includes mostly large, global companies. On the other hand, the small and mid cap indexes are made up of mainly domestic companies that derive their revenues from the US. These companies continue to do much better than the S&P 500 this year.

Here are the best annual returns for the Wilshire Small and Mid Cap Indexes since 1979 along with the performance for this year through 9/30:

So with a full quarter to go, the performance of these two markets already ranks near the best of the last 30+ years.

Now if only I was able to predict how things will shake out for the rest of the year I’d be all set.

A Wealth of Common Sense is a blog that focuses on wealth management, investments, financial markets and investor psychology. I manage portfolios for institutions and individuals at Ritholtz Wealth Management LLC. More about me here. For disclosure information please see here.

Get Some Common Sense

Categories

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.