Gold is one of those investments that attracts extreme viewpoints and ideological arguments that favor narratives over substance. I think the reason for this is because the U.S. was once on the gold standard, which was more or less replaced by the Federal Reserve as a form of monetary policy.

Anytime politics and government is involved, there are bound to be irrational people and emotional arguments made both for and against that topic. Gold has become the de facto us vs. the system investment over the years and this has only intensified as the role of central banks in the markets has grown in recent years.

It’s rare to find a simple historical account of the yellow metal that doesn’t involve highly politicized or biased points of view, so I thought I would take a look back at the history of gold’s performance as an investment over the years.

In August of 1971, when Richard Nixon ended the convertibility of the U.S. dollar to gold, the price was roughly $40 an ounce. From there it grew all the way to $850 an ounce by early 1980, for a return of more than 2000%. In a decade that saw subpar returns on both stocks and bonds in the U.S. along with sky high inflation, it was by far one of the best investments in that time. The price didn’t move much before Nixon removed the peg so it’s very possible that this was a catch-up period in terms of price.

From that point on, over the next 20 years or so, the price of gold fell over 70% until it finally bottomed in late-1999. The annualized 20 year return from 1980 to 1999 was just shy of -6% a year. From 1971 to 1999 the total return was close to 6% per year, which shows how much of the total return up to that point occurred in the 1970s.

From a price of just over $250 an ounce in late-1999, gold then grew to just over $1,900 and ounce by late-2011, for a gain of almost 650% or an annualized return of more than 18%. Gold only had a closing price above $1,900/ounce for a single day before staging a fairly quick retreat from that record price. From the peak in September of 2011, gold is now down 42%.

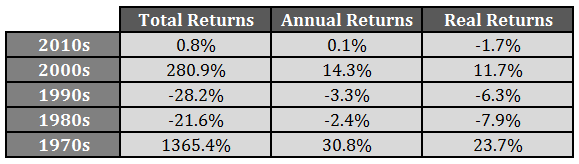

I broke down the returns into different time frames to give you a sense of how gold has performed over the different decades:

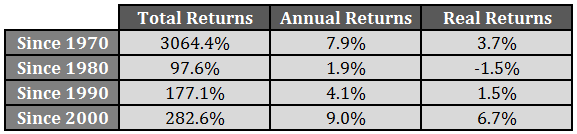

There’s still plenty of time remaining in the current decade, but if things continue as they have over the past few years, it’s possible that gold could have negative real returns in three out of the past five decades. The starting point for the performance measurement also plays a large role in the total performance numbers:

There’s still plenty of time remaining in the current decade, but if things continue as they have over the past few years, it’s possible that gold could have negative real returns in three out of the past five decades. The starting point for the performance measurement also plays a large role in the total performance numbers:

Had you invested in 1980, following the huge surge in gold in the 1970s, you would have lost money to inflation over the ensuing 35 years. Since 2000, gold has actually outperformed the S&P 500. Both of these statements are true, but you’ll be hard pressed to hear both from gold’s most ardent supporters or detractors. As with all investments, if you change the time frame, almost any argument can be made either for or against, depending on how the information is presented. Depending on your time frame gold has either been a terrible investment or a solid (no pun intended) diversifier.

Even after the most recent crash, gold is actually up around 10% per year over the past decade. But it’s unlikely many individuals actually participated in this rise unless they held physical gold. The Gold ETF (GLD) only had around $3 billion in assets in 2005. It then grew to nearly $80 billion by the peak in 2011-12, before falling back down to less than $25 billion more recently. Unfortunately that means many of the bandwagon investors got sucked in very late to the bull market and lost a lot of money in the ensuing crash.

Here’s the only thing I’m sure of after looking back on the history of the price of gold — it’s extremely volatile and cyclical. Other than that, I’m not sure I can deduce much from the yellow metal that seems to evoke such passion from certain corners. I’ve seen some strong arguments that can be made for a relationship between gold and real interest rates, but that’s the kind of thing that can come and go as it pleases.

My stance on gold has always been that I have no idea what’s going to happen with it in the future. No one else does either.

Further Reading:

What About the 1970s?

GLD’s Fall From Grace

[…] A history of gold returns. (awealthofcommonsense) […]

The only other thing I would add is that gold can be a hedge against currency weakness. It’s down ~15% in USD terms in the last year or so, but if you’re a Canadian or European or Japanese investor with most of your wealth in your domestic currency, you’d actually still be up marginally on your gold position factoring in the declines in those currencies this year. It’s one more factor to consider if preserving international purchasing power matters to you.

Right, international owner of US stocks have been doing great the past few years, but I get your point. It’s another form of currency diversification for foreign investors. I’ve never done an analysis of gold vs USD but it might make sense to take a look.

Real rates/yields drive Gold which is inversely correlated. That is about 90% of what determines Gold’s trend and performance. Over the past 4 years real yields/rates have increased thus exacerbating the fundamentals for Gold, which also had a historic 11 year run without a down year. With sovereign debt burdens extremely sensitive to rates, we will have negative real rates for a long time until debt is inflated away. When rates can be normalized again, Gold will fall back into a secular bear and equities will prosper. Just my opinion of course.

Could be. I just wonder if central bank policies have messed with traditional interest rate relationships. Maybe not, but it’s worth considering.

I think CB policies have accentuated market moves. In the last 20 years there have been extreme moves in various assets on both sides. Stocks have seen their 2 worst bears since WW2, yet climbed to new ATH and have kept going. And that was after a full blown tech mania. Gold went up 12 years in a row (calendar wise). Bookending that was the two worst bear markets ever for the mining industry. Doesn’t even include 2008 crash. The two worst bear markets ever for commodities & also a huge boom. A 75% decline for Silver then a 6-fold move in 3 years then another 75% decline..all in 6-7 years. This is just not normal.

A recovery from 2008 was to be expected but policy has extended it quite a bit. Fed policy has allowed corporations to juice earnings through buybacks. Its allowed disinflation to persist, the best environment for stocks. By not raising rates sooner, they run the risk of more extreme cycles in the near future.

[…] A Wealth of Common Sense […]

Any idea how a portfolio with 10-15% gold (mainstream advice) works with a 85-90% S&P 500 does?

I keep about 5% gold ETF

You can run different asset allocations on this site:

https://www.portfoliovisualizer.com/backtest-asset-class-allocation#analysisResults

I’m pretty sure historically it’s helped dampen volatility a bit from the rebalancing/diversification effects.

[…] Given the current theme of commodity prices and gold, here is a piece from one of our favourite bloggers – A History of Gold Returns […]

[…] – Bloomberg Is Gold a Stupid “Pet Rock” or a Bedrock Asset? – Mining.com A History of Gold Returns – A Wealth of Common […]

[…] Falling So Hard It Looks Like Capitulation (Barron’s) see also A History of Gold Returns (A Wealth of Common Sense) • Are the stock shares you own really yours? Not according to the state […]

[…] – A history of gold returns. […]

Great article. I had a conversation recently with someone about gold and the returns it has provided. Like any investment window, it depends upon the frame you are looking through. Long-term, gold is not a great asset but within certain years, it has been tremendous.

I don’t own any G yet but the entry point of around $17 is appealing.

Cheers,

Mark

Amazing how far these things can overshoot in either direction. Fun to watch as a casual observer.

The same could be true for stocks! The 70’s were bad for stocks. The 80’s and 90’s were good…the 2000-2008 was bad for stocks….then QE helped to artificially stimulate things….If you look at all asset classes in isolation, they can look crazy. But we cannot predict the future, so it would make sense to keep an allocation of uncorrelated assets. The worst you would want to be is 100% in assets during a market crisis, and being forced to sell. If you had some gold and it shot up in value, and you needed money, you can sell off a winning asset class at least! Gold is crazy looking at it on it’s own, but it makes sense as being part of a diversified portfolio.

That’s what makes diversification so great and so terrible at the same time — you’ll always end up hating something.

[…] Wealth of Common Sense had a recent post on a history of gold returns. His key message is this: investing in gold is highly dependent on the period you start investing […]

[…] is a poor investmentGold has had an awful year, and that’s not unusual if you take the long […]

[…] The edited excerpts above, and those below, are from an article* by Ben Carlson (awealthofcommonsense.com) entitled A History of Gold Returns which can be read in its entirety HERE. […]

Great article, I love the way the author presented both the good and the bad of precious metals investing. Most authors only tell one side of the story using cherry picked data to support their position. This is especially true with silver, which was run up in price 35 years ago when a couple of millionaires artificially drove up the price by trying to corner the market on silver. I often hear advertisements talking about how silver has not recently reached the highs of that era, as though this means the metal is underpriced, while leaving out that the high price was set only because of market manipulation. It may not be illegal to leave out this information but it is sure dishonest.

Watching the market for many years I’ve concluded that precious metals are at best a very risky financial investment, and that most people would likely make more money investing elsewhere. For example, a friend of mine owns a number of rentals that he bought during periods when real estate was way down. He bought his houses very cheap over a 20 year period and on average they are worth about 2 to 3 times what he paid for them. But he also makes several thousand dollars per month renting them out, so if he ever decides to sell his houses the profit will just be the icing on the cake.

So while I don’t buy precious metals to invest in them, I do buy them for the same reason I buy insurance, to provide some protection in case the very worst happens. The probability of a major financial meltdown in any given year is very small but it still exists, and the increasingly irresponsible financial mismanagement by the U.S. government makes the likelihood of a crisis greater each year. Our currency will be good as long as most people believe in it, but the day could come when this faith is gone. Looking at examples of financial collapses in other nations, often the general public is mostly unaware a crisis is brewing until things suddenly collapse, when it is too late to prevent loss of savings and other investments.

My goal is to put about 10% of my savings into precious metals, which are stored in a vault outside the commercial banking system, because in the event of a crisis the government is likely to prevent people from accessing safe deposit boxes and may even confiscate gold and other items from them. If the crisis never happens these precious metals can be used as last resort savings in my retirement years, and if not needed I’m sure my heirs will be delighted to inherit them. But if a crisis ever does happen and my savings and other investments are lost, this modest investment in precious metals may be all that I have left.

So when considering precious metals, keep in mind that they can also be insurance against disaster as well as a financial investment.

[…] to what many people think, it was refreshing to read this article about gold returns. “Had you invested in 1980, following the huge surge in gold in the 1970s, you would have […]

[…] https://awealthofcommonsense.com/a-history-of-gold-returns/ […]

[…] A History of Gold Returns […]