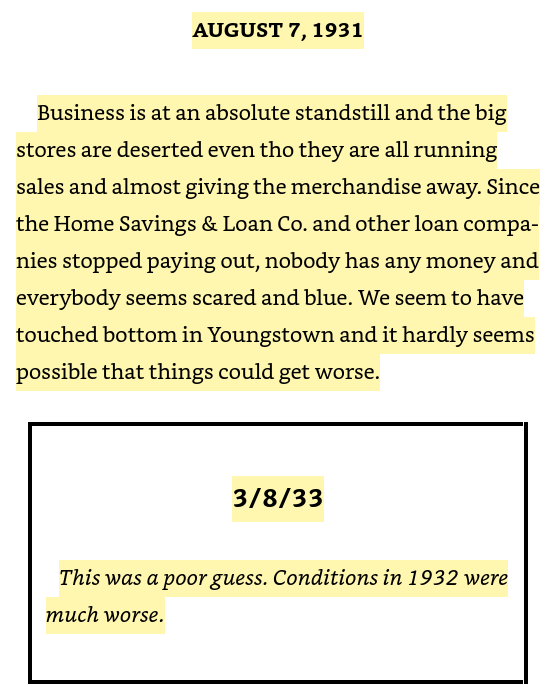

The Great Depression: A Diary is the best book ever written about the worst crash in history.

Most history books are written with the benefit of hindsight but this was a real-time account from a lawyer in Ohio about what it was like to live through the depression. Benjamin Roth also went back and made notes on previous passages as he went along.

This one provides a good example of what it was like to live through this period of unending economic strife:

That constant beatdown of the Great Depression left scars on an entire generation of people.

Studies have found that Depression Babies experienced long-term negative effects on their education, earnings, and health. People who lived through that period were also less willing to take risks, were more frugal with their money and less likely to own stocks.

At the outset of the pandemic, some people pondered whether we would experience a similar outcome of a lower appetite for risk. The unemployment rate soared to more than 14%. It looked like all sorts of businesses were doomed. The stock market crashed in an instant. Things were bleak.

Then governments around the globe threw trillions of dollars at businesses, municipalities and households. We were off to the races.

The assumption was that the speculative attitudes ignited by the pandemic spending binge would be short-lived. People have been calling for the end of these actions for years now.

Just wait until professional sports betting comes back. Then people will give up on the stock market.

Just wait until the meme stock craze comes to an end. Retail will go home with their tail between their legs.

Just wait until all of the pandemic excess savings go away. That will stop all the consumer spending.

Just wait until inflation hits. That will get households to batten down the hatches.

Just wait until we get a bear market. Then everyone is going to panic sell.

All of these self-imposed pundit deadlines have come and gone yet household appetite for risk remains strong.

Now it’s just wait until there’s a once-in-a-lifetime crash like the Great Recession. Sure, but those crashes are rare by definition.

Everyone is thinking about this idea through the lens that this behavior is cyclical.

My question is this: What if it’s secular?

What if an entire generation of people experiences the opposite of the Depression Babies? What if the pandemic flipped a switch in people who are more willing to take risk?

What does that mean going forward?

I’m still pondering the potential implications but let’s look at some of the evidence first.

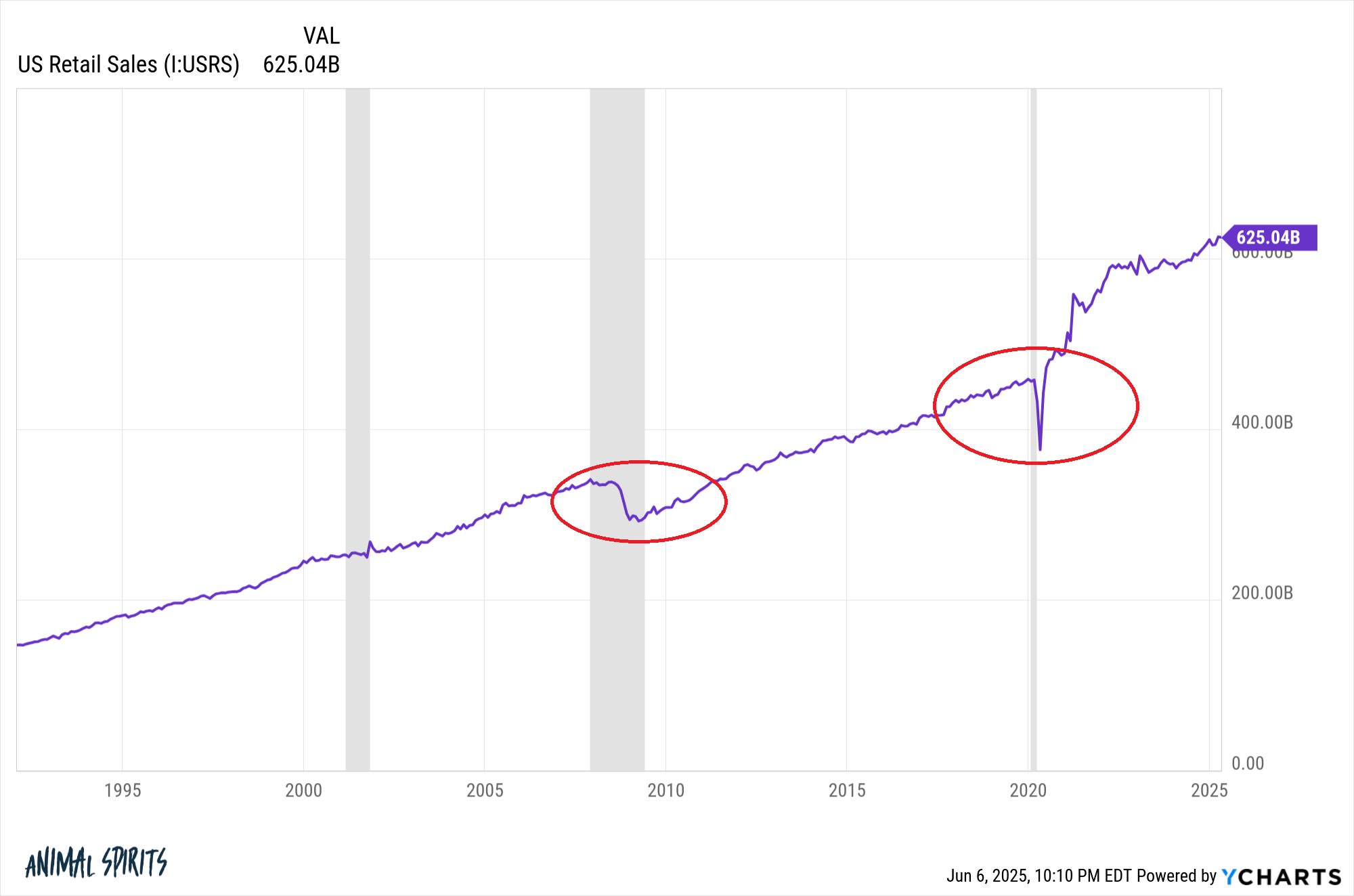

Consumer spending was knocked down a peg following the Great Recession. Spending took off like a rocketship in the 2020s1 and set off on a new trajectory:

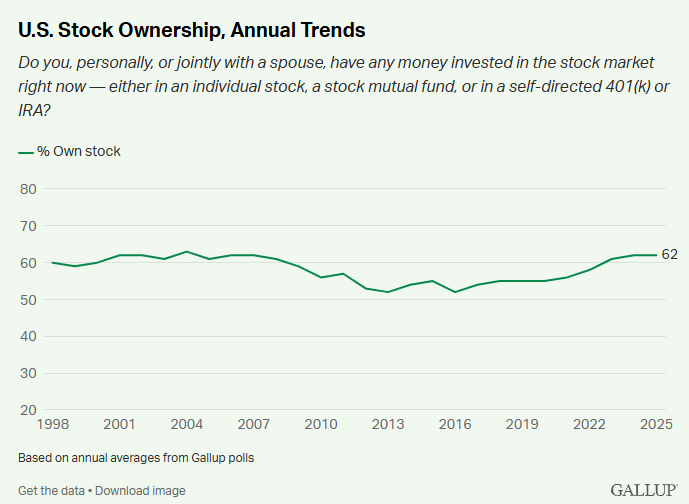

Gallup has been tracking household stock market ownership for years now:

After peaking at 63% in 2004 following a massive increase in stock market ownership from the 1990s boom times, the household share of stocks fell to 52% by 2016. The 2008 crisis also left some scars.

Now it’s all the way back up to 62% as a new generation of investors has entered the market.

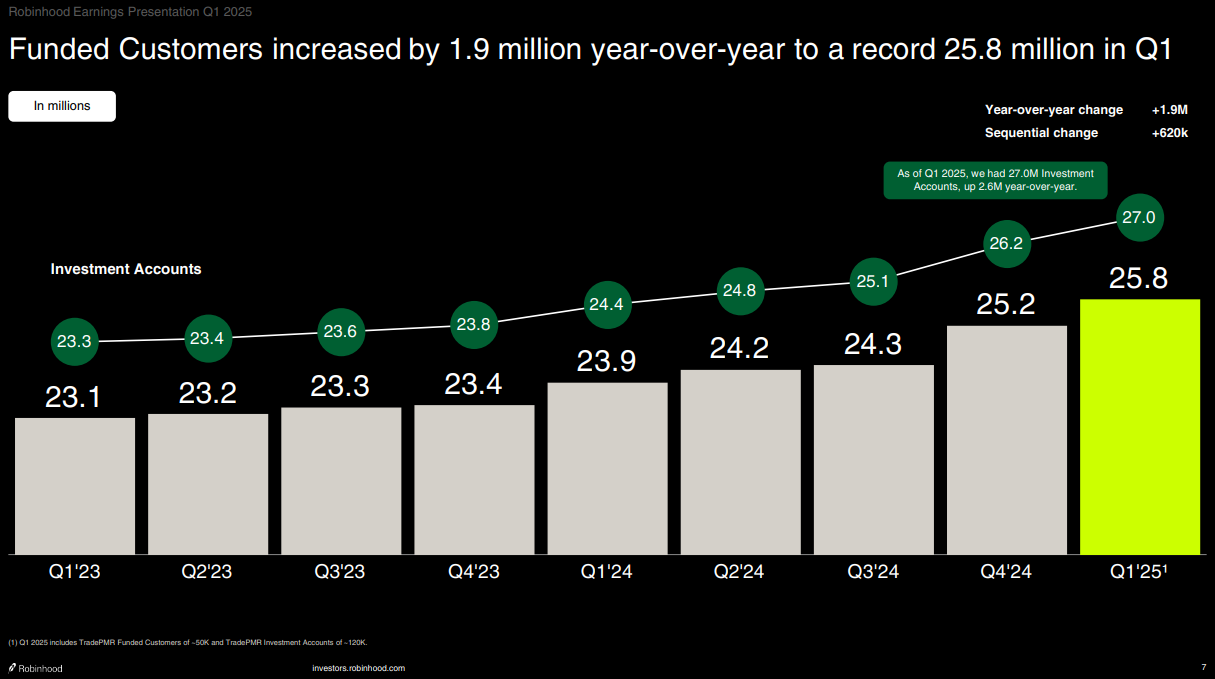

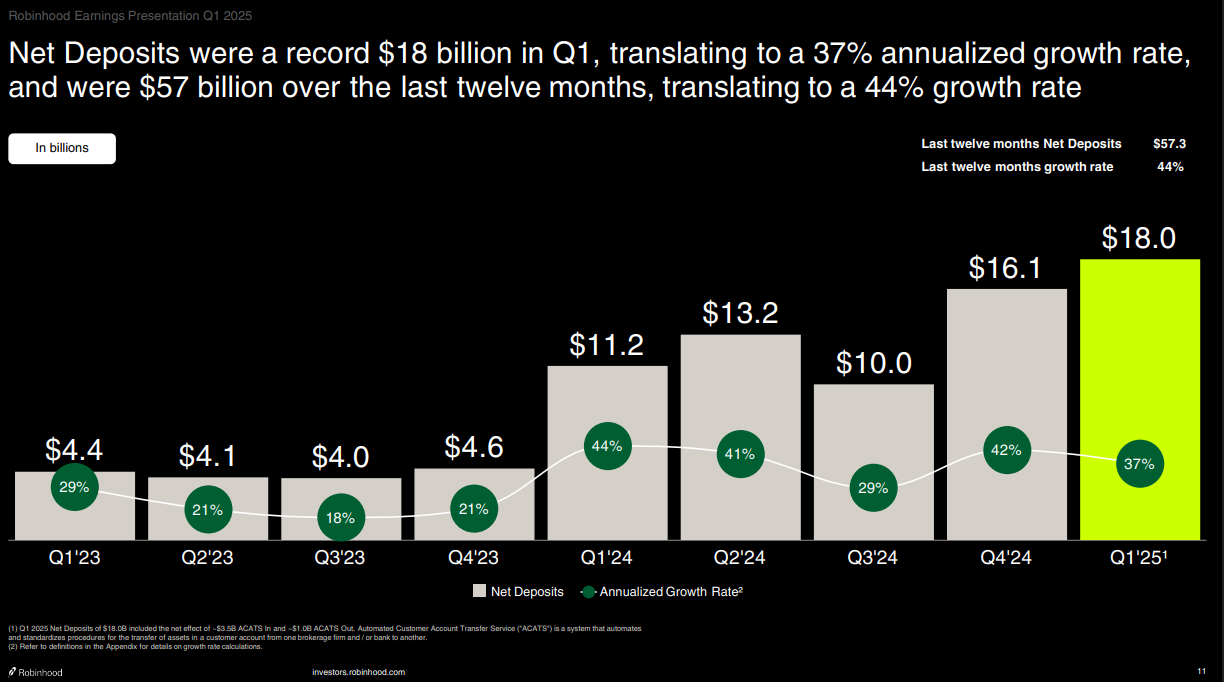

Robinhood now has nearly 26 million customers:

For around half of those customers, it’s their first-ever brokerage account. And they keep funneling money into their accounts to invest more:

It’s not just stocks either.

Bitcoin is likely the first ever financial asset that was owned by retail before institutional investors. Many of the early bitcoin investors are younger. They’ve been rewarded with gigantic returns but also some bon-crushing crashes:

Bitcoin has fallen by 75% or more twice in the last eight years. Most investors have held on despite the huge losses.

In 2019, the amount of money wagered on sports betting was less than $1 billion. In 2024, it was nearly $150 billion.

People are more comfortable with risk. They’re more comfortable with volatility. They’re more comfortable spending money.

Now, maybe this renewed appetite for risk will be extinguished during the next recession. We haven’t had a real recession in over 15 years.2 It’s certainly possible all it will take for risk attitudes and consumer spending behavior to slow down will be a slap on the wrist in the form of an economic downturn.

But what if we only get a run-of-the-mill recession?

What if this acceptance of risk is here to stay?

Could it lead to more asset bubbles?

Could it lead to more frequent volatility and bear markets?

Could it lead to more V-shaped recoveries?

I don’t know the answers to these questions because it’s difficult to predict how experiences will shape the future and how the future will shape people’s behavior.

But this has been going on for long enough that it’s worth considering the idea that we could be witnessing an entire generation of people who are more willing to take risks.

It could have long-lasting implications for the economy and the markets for years to come.3

We talked about this idea and much more on a live recording of The Compound and Friends from the Chop Shop in Chicago this week:

Further Reading:

Two of the Biggest Trends This Decade

1Some of this is from inflation of course but the point remains.

2The pandemic recession doesn’t count. It was over too quickly and even people who lsot their jobs were made whole by higher unemployment insurance.

3And if we get a recession that completely changes people’s behavior? Well, that’s human nature for you.