A reader asks:

I would like your opinion on a recent Wall Street Journal article: “You’re Probably Overinvested in Bonds.” My request focuses on the following paragraph:

“Plenty of people should hold bonds. If you are retired and subsisting on your investment income, or if you would have to sell a significant chunk of your investments to cover living expenses in a bad year, you should have more in high-quality bonds. But that probably isn’t true for two large groups: The six million to seven million Americans with $1 million or more in investable assets and other households with more than $100,000 in investable assets whose noninvestment income covers their cost of living.”

My wife and I are retired and in our early seventies. We fit this description. We have traditionally had a 80/20 stock/cash split and haven’t held bonds. What do you think of Mr. Posen’s conclusions?

I’ve been getting lots of questions from retirees about how to handle their fixed income allocation in retirement.

Some people would like to hold cash rather than bonds. Some people would like to know if keeping all of your money in stocks makes sense.

The Wall Street Journal article from Mr. Posen has a similar tone.

The idea is that a balanced 60/40 portfolio gives up too much on the upside. A 90/10 portfolio, on the other hand, is based on the idea that the stock market has generally trounced bonds over the long-term.

Of course, you don’t get that upside without some downside, which Mr. Posen addresses:

Stock declines are relatively infrequent and typically are followed by increases–a recurring pattern over the past 60 years.

This is true, on average.

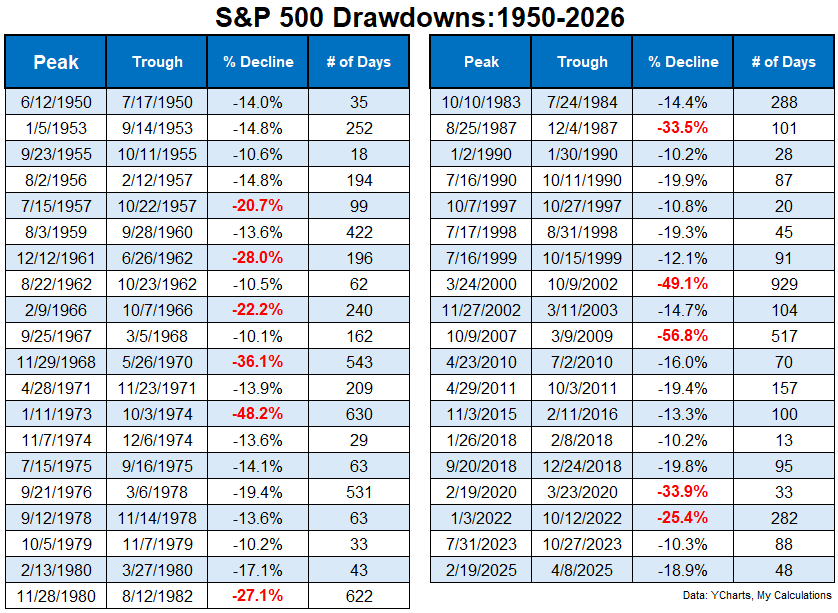

By my count there have been 39 double-digit stock market corrections on the S&P 500 since 1950. That’s one correction every two years, on average.

Here are the numbers:

The average drawdown for the S&P 500 in those instances was -20%. The average peak-to-trough decline took 193 days.

So that doesn’t sound like the end of the world.

However, that’s just the peak-to-trough drawdown. Even though stocks bottom at that point and begin moving higher, you would still be underwater.

The average number of days it has taken to breakeven during these corrections is 306 days. Put it all together and that’s nearly 500 days in a drawdown while waiting for new highs again.1

And that’s just the average.

What if you get hit with a long bear market at an inopportune time?

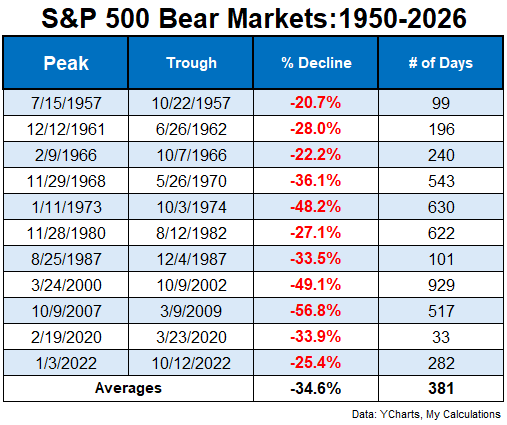

These are all of the bear markets since 1950:

The average drawdown is much steeper and it takes much longer to bottom. It can also take a lot longer to reach new highs again.

It took almost 6 years to breakeven following the 1973-74 bear market. The dot-com bust took four-and-a-half years to recover from the bottom. The Great Financial Crisis peak was in the fall of 2007. New highs weren’t breached again until 2013.

Of course, the Covid crash took less than 150 days to recover. Maybe the speed of markets will make these downturns shorter in the future? It’s certainly possible. Most of the time the recovery is a matter of months, not years.

In most cases, you would probably be fine in a 90/10 portfolio. And you would end up with way more money too!

But it’s a risk to have such a high allocation to stocks in retirement if you don’t have some sort of back-up plan.

For investors still putting money into the market on a regular basis, lengthy drawdowns are an opportunity, not a risk. You get to buy stocks at lower prices.

You have a much smaller margin of safety in retirement.

There is no more income from a job to buy stock when they’re on sale.

You don’t have nearly as much time to wait out a painful bear market.

And if you don’t have a big enough fixed income position, you don’t have any dry powder to lean into the pain and buy stocks.

If you happen to live through an outlier bear market it could severely impact your plan. If you spend down your 10% in money markets, you now have to replenish that allocation which could mean selling stocks when they’re down.

I do agree with the author that retirees likely need to take more equity risk than the textbooks would tell you. People are living longer. You might have 20 to 30 years in retirement to keep up with inflation. You still need to take some risk.

I just think you need to have a really good handle on your spending if you’re going to keep an outsized allocation to stocks in retirement. It could be dangerous if you’re taking too much risk at the worst possible time when you don’t have more money to put to work in the market or wait out a prolonged bear market.

You could be leaving money on the table by taking less risk in retirement.

But you only get one shot at it.

I discussed this question on an all new episode of Ask the Compound:

Bill Sweet helped us answer questions about timing the sale of your stocks for a vacation property, housing as an inflation hedge for young people, down payment size and what financial gift to give for a Sweet 16 birthday.

Further Reading:

The 4 Year Rule For Retirement Spending

1It is worth pointing out I’m using price-only data here. So on a total return basis with dividends included that would shorten the time a bit. But not a ton.