Young people have it tough in a lot of ways, financially speaking.

Housing is expensive. Student loans. Inflation. The cost of daycare. Etc. Etc.

I know there is worry of disillusionment and financial nihilism among the Gen Z cohort but I have faith in young people.

This group already has some things figured out.

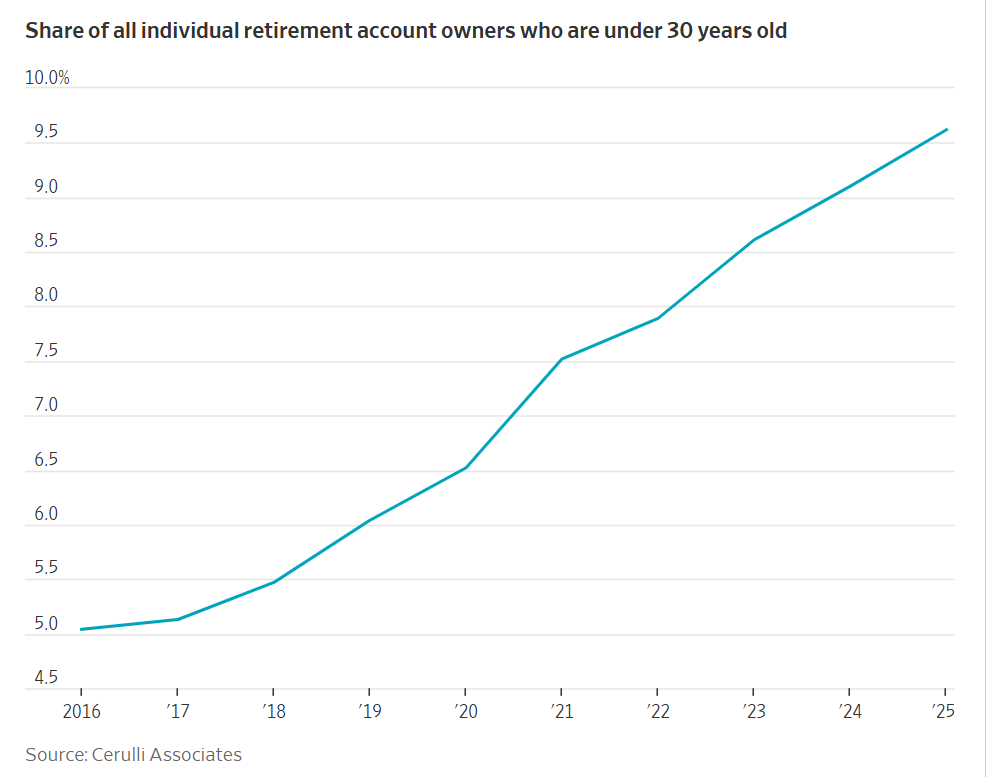

The Wall Street Journal shows people under 30 are taking advantage of tax-deferred retirement accounts:

The share of IRA accounts held by those under 30 has nearly doubled in the last 10 years.

Here’s some more data:

Among Gen Z investors, total IRA contributions grew 65% year-to-year in the first quarter of 2026, compared with a 31% increase for millennials. Three-quarters of people age 35 and under chose Roths, compared with less than half in that age group a decade ago, according to Fidelity Investments.

This is great news!

Young people are saving and investing for their future. If they don’t interrupt the compounding in these accounts, the wealth will be wonderful many decades from now.

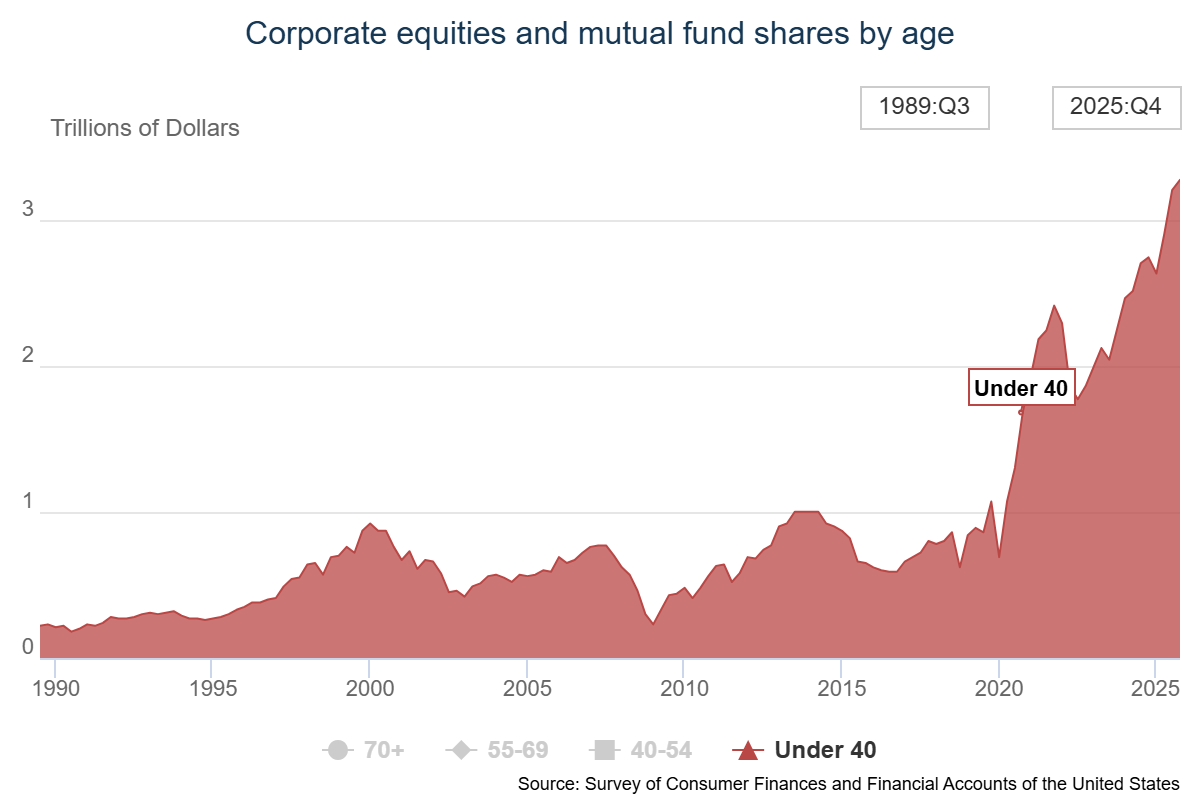

The great thing about qualified retirement accounts is that they are perfect vehicles for long-term investments… like stocks!

Young people have developed a taste for stocks.

Just look at the change in value of stocks owned by people under 40:

It’s up 3x since 2020. The share of equities owned by people under 40 is still relatively low (6%) but it has doubled this decade.

That’s progress.

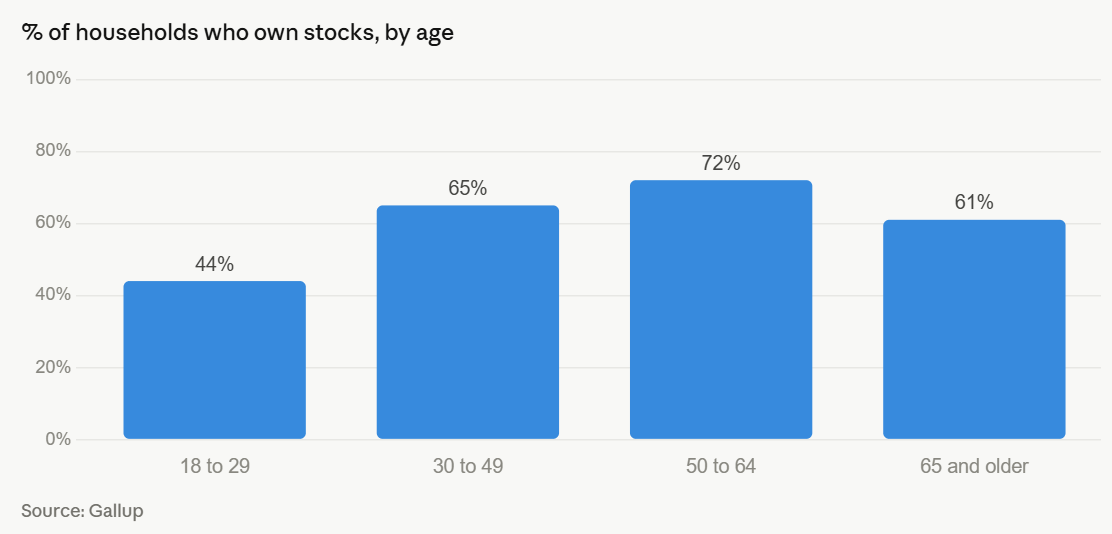

Here’s a breakdown of household stock market ownership by various age groups:

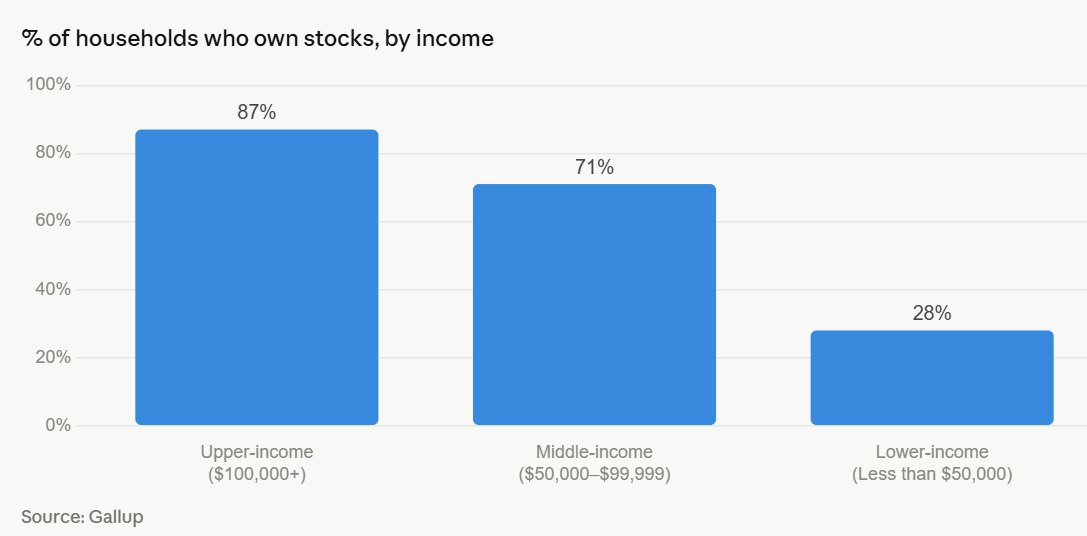

Now here it is by income level.

If you wanted to take a glass-is-half-empty view of the world, you could say young households and low income households (which have a lot of overlap) have a much lower level of ownership than older people and those with higher incomes.

That’s true of course.

However these numbers require context.

I wrote a whole chapter in Risk & Reward about the history of stock market ownership in America.

In the early-1950s just 4% of households owned stocks in any form. By the early-1980s it was just 19%. It wasn’t until the 1990s that things really took off in terms of the masses buying stocks.

From a glass-is-half-full perspective, young and low income households now have a higher ownership in stocks than the entire country did back in the day. The numbers are moving in the right direction even if the top 10% still owns most of the shares.

Of course, part of the reason more young people are investing in the stock market is because housing is so expensive. If you’re not building equity in a home or saving up for a down payment, there’s more disposable income available to invest in equities.

But this is also about a breaking down of the barriers to entry in the financial markets.

Technology makes it easier to invest. Fees have come down. Minimums are non-existent. Investors are more knowledgeable.

We need more people invested in the stock market. The earlier the better.

This is great news for young people.

Further Reading:

Are Young People Screwed?