Every year I do some back-of-the-envelope investment planning to set some goalposts.

It’s a useful process to take stock of where you are, where you’ve been and where you’re going.

I take our current net worth and savings rate. Then I make some assumptions about future savings rates, income and return expectations. Those return expectations exist in a range because it’s impossible to predict the future.

Then I model all of these numbers going out 5, 10, 15 and 20 years. I’ve been doing this exercise since I was 25. The object here is not certainty about my financial future. I’m just trying to set up some road markers along the financial journey to see where things stand for planning purposes.

The assumptions are almost always going to be wrong because the financial markets (and life for that matter) aren’t linear. They’re lumpy.

Once the expectations turn into reality I can see if we’re doing better or worse than my projected range of outcomes.

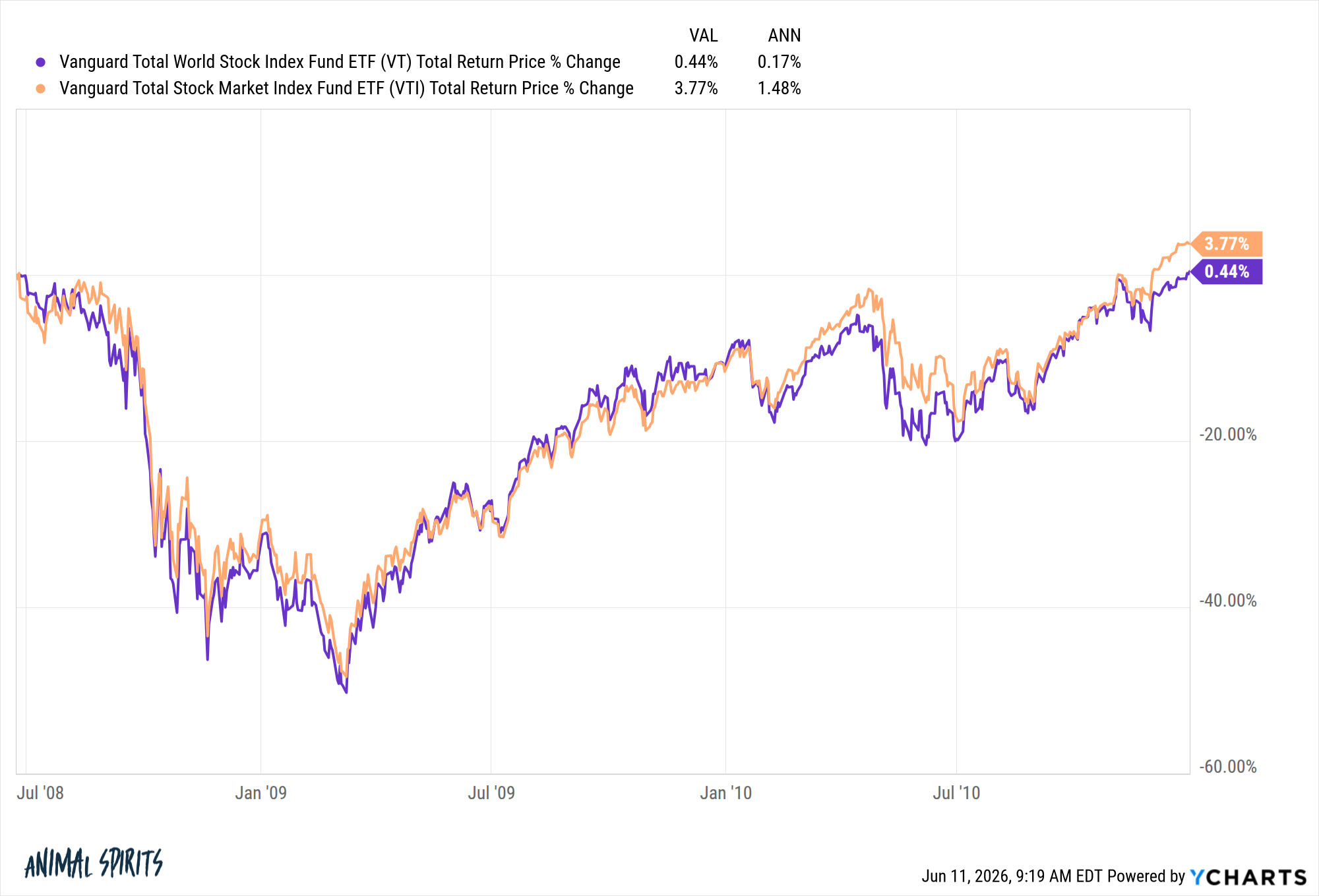

For example, in the first 5-7 years of planning the actual output fell far short of my assumptions. Why? The stock market fell nearly 60% in the Great Financial Crisis. Returns were abysmal.

From 2005 to 2010, when I first started investing in my retirement accounts, stocks essentially went nowhere:

It was a ferocious bear market.

I still dutifully made retirement contributions but saw little progress in terms of investment returns and market value.

That type of environment can make you feel dumb as an investor. The good news is I got to buy periodically at lower prices in a highly volatile market.

Since then the returns have been much better.

Since 2009, the S&P 500 is up more than 15% per year. A global stock portfolio has experienced annual returns of around 12%. If I wanted to get really specific, the U.S. stock market is up 16.9% per year from the bottom of the Great Financial Crisis in early 2009.

No one builds a financial plan with return assumptions this high.

I certainly didn’t.

No one in their right mind could have predicted the bull market would last as long as it has.

Because of the lengthy bull market, my portfolio is now much larger than my original assumptions. In fact, the current reality didn’t even exist in my range of outcomes.

But here’s the thing — I’m not smarter because the markets have been going up. Sure, I had to stay invested but it’s not my raw intelligence that increased my portfolio to heights I didn’t plan on 5, 10 and 15 years ago.

Bull markets don’t mean you’re a genius just like bear markets don’t make you an idiot. I wasn’t a dumb investor during the Great Financial Crisis. I did what I was supposed to do.

I bought and I held and everything went straight down.

Bull markets don’t make you a smarter investor. Bear markets don’t make you a dumber investor.

The problem is your emotions can often grab the steering wheel when markets are going up or down.

Bear markets can make you question your plan.

Bull markets can lead to overconfidence.

I don’t know when the current bull market will end or why.

Maybe it lasts 5 more years. If it does that doesn’t make you a smarter investor.

It could end tomorrow. If it does that doesn’t make you a dumber investor.

One of the ways I like to remind myself how dumb I can be is to write stuff down.

Here’s what I’m going to do and why I’m going to do it. Here’s what I think might happen.

This is a great way to keep yourself grounded and avoid being outcome-based.

Process over outcomes.

Further Reading:

Tops and Bottoms