Bond yields are rising again.

This has many people worried.

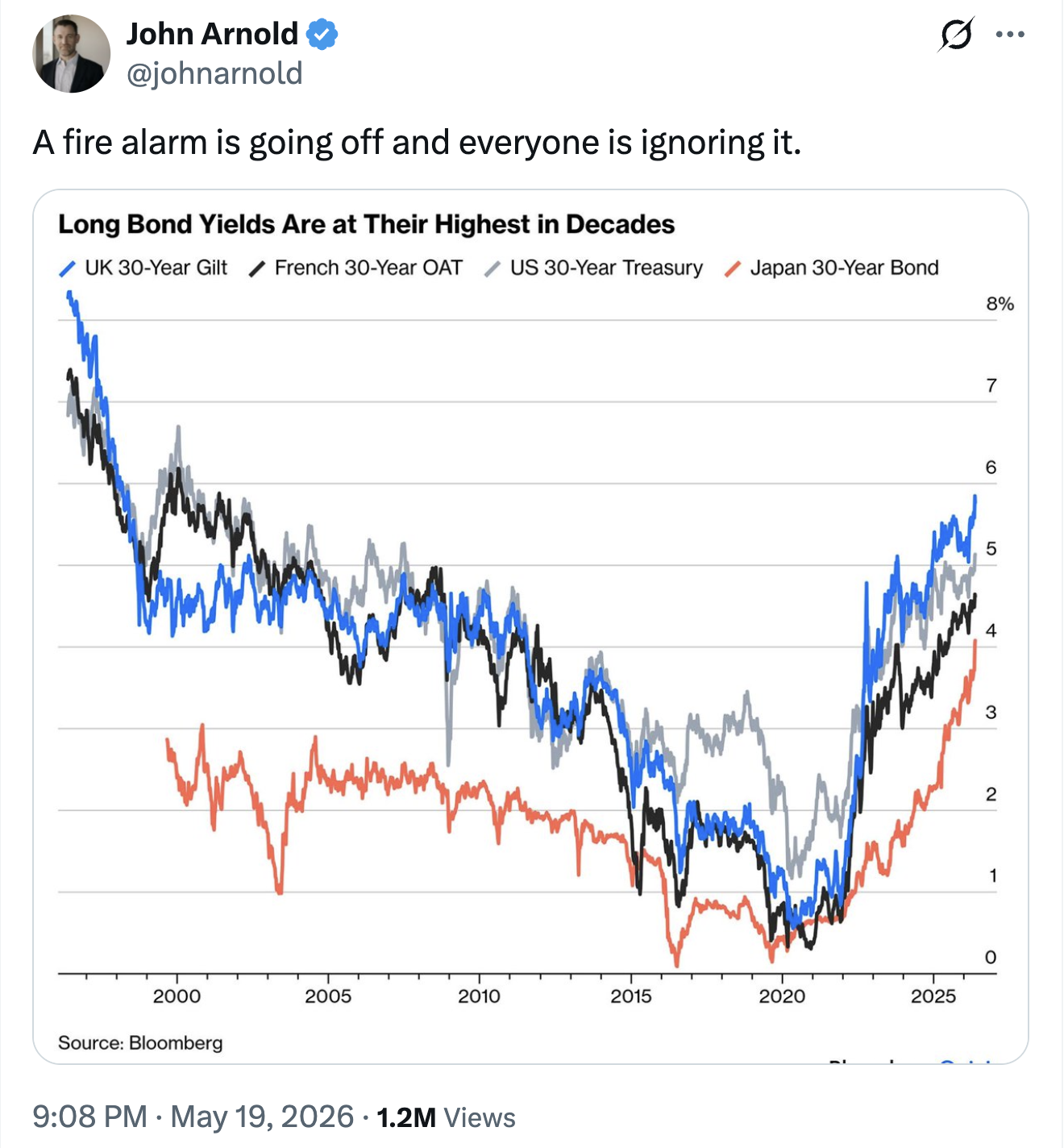

Here’s John Arnold’s take:

The 30 year Treasury yield is at its highest level since just before the Great Financial Crisis in 2007. Japanese long-term bond yields haven’t been this high all century.

Why does this have people worried?

Government debt levels are much higher so higher yields will only increase the amount of the budget that goes towards interest expense. Some think people are losing faith and trust in the government’s ability to rein in spending. Others are worried this is a sign inflation is moving much higher.

Some of these concerns are valid. But it’s not all doom and gloom. There are pros and cons when it comes to higher bond yields. There’s more nuance required here than a five alarm fire.

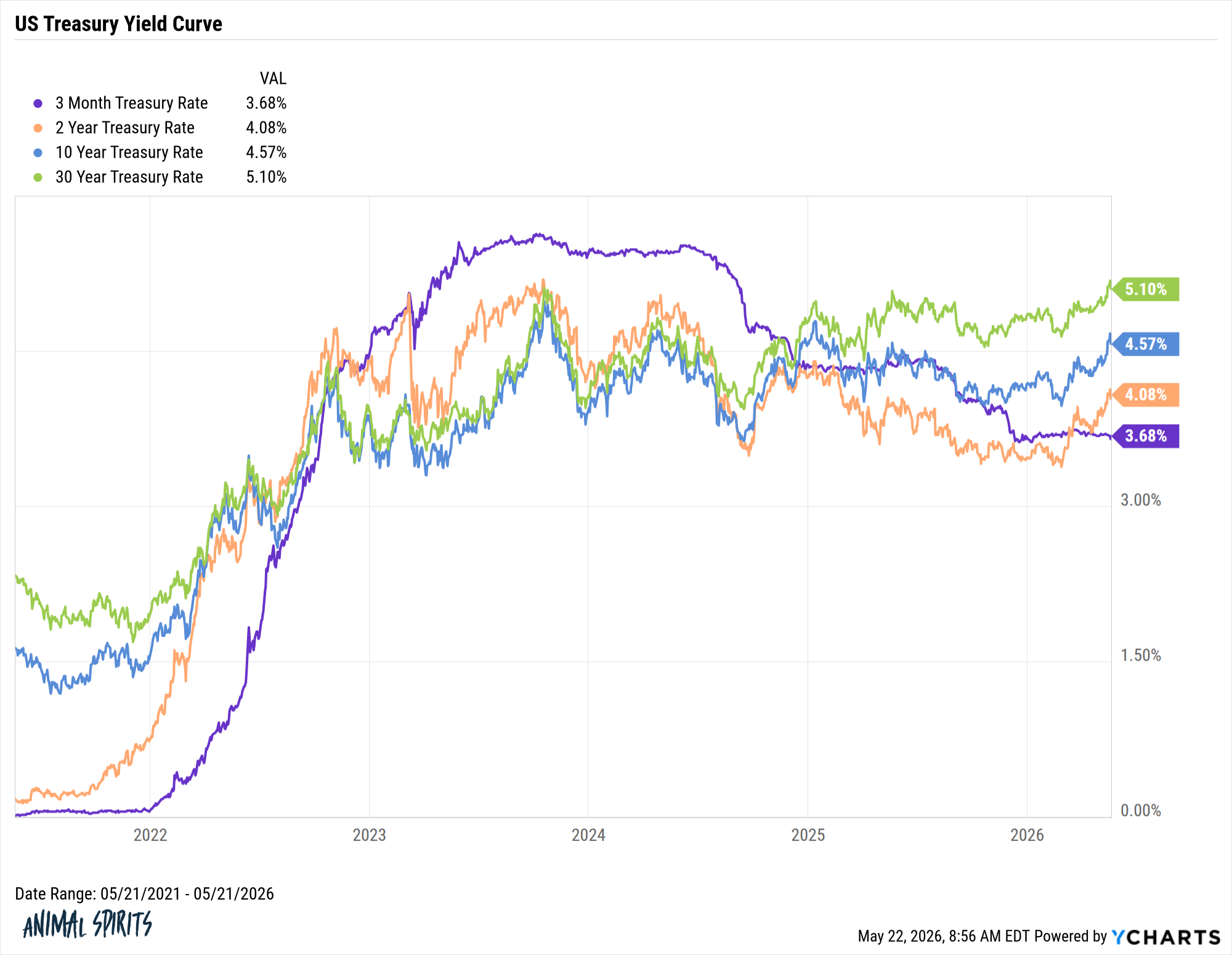

The first thing to consider is that we’re finally getting back to a more normalized yield environment. For around 3 years the yield curve was inverted, meaning short-term rates were higher than long-term rates. That is not a normal state of affairs. It’s worth pointing out, many pundits were predicting a recession that never came because the yield curve was inverted.

Now look at it:

Long-term bond yields should be higher than short-term bond yields to compensate investors for the risks. Nature is healing.

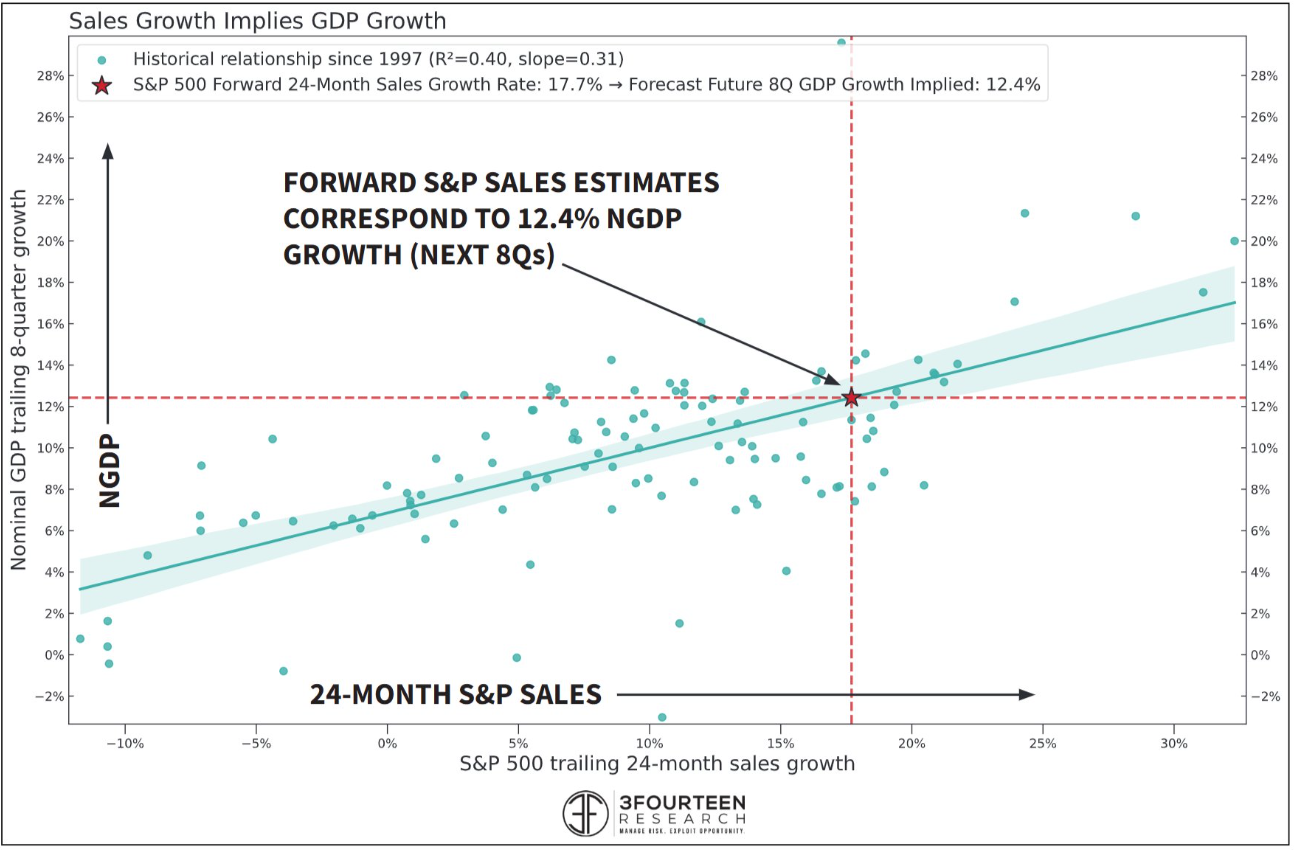

The bond market could also be signaling we are in an environment of higher economic growth and inflation. Warren Pies has a chart that links nominal economic growth with sales growth on the S&P 500:

Higher sales growth implies higher economic growth. When growth is high, interest rates tend to be higher.

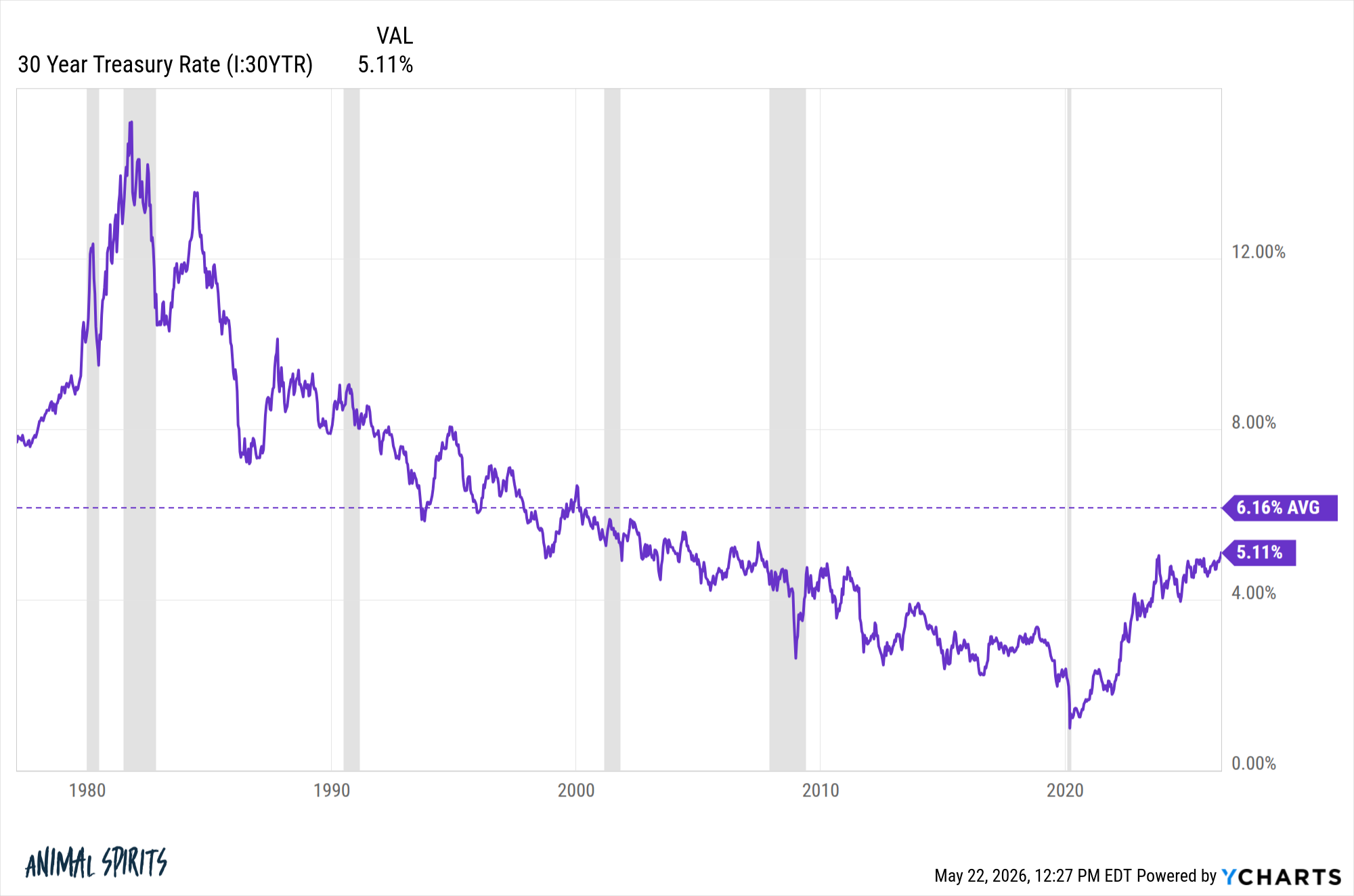

The 30 year Treasury rate has averaged 6.2% over the past 50 years or so:

In this context, 5% doesn’t seem all that high.

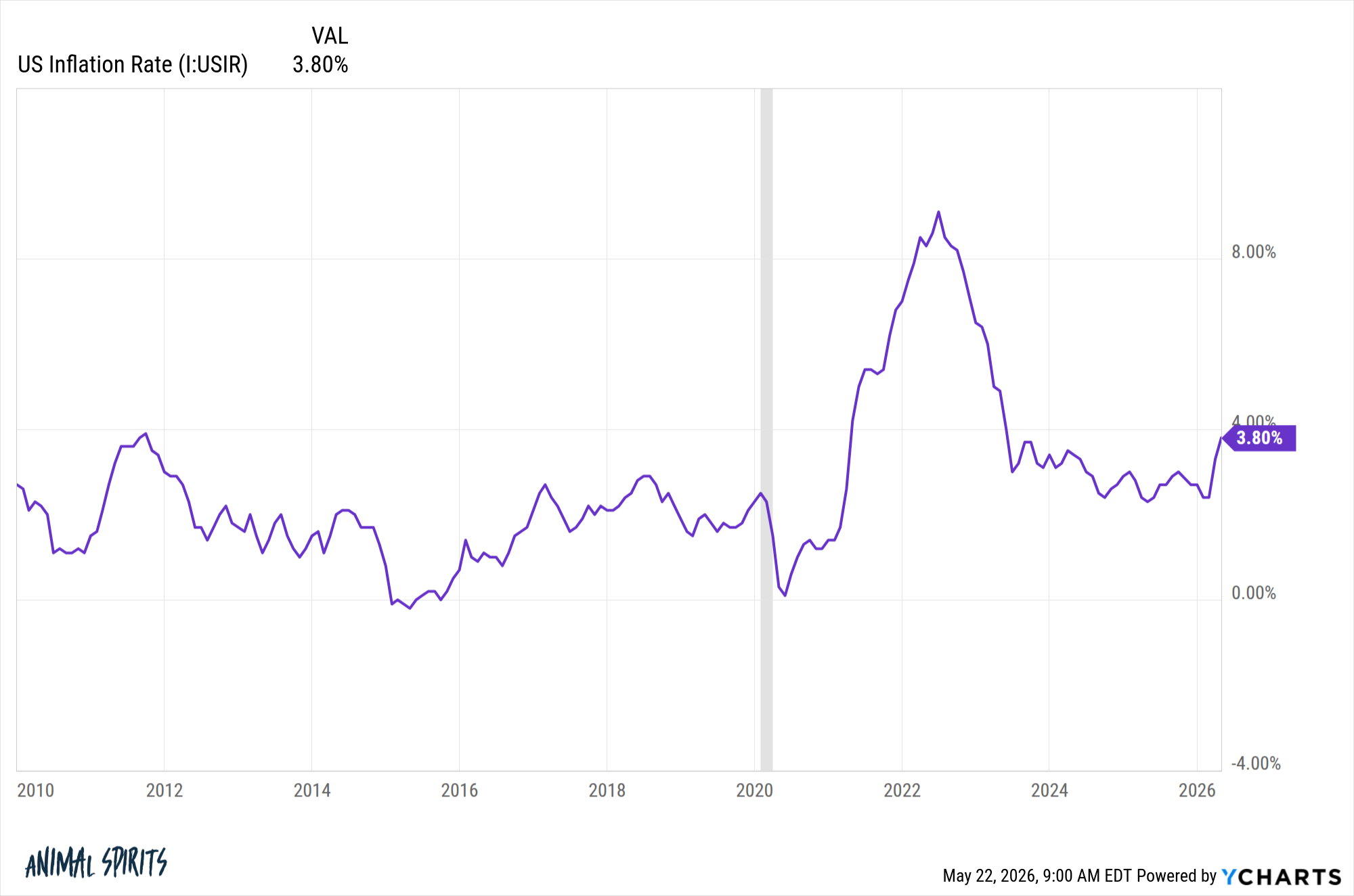

Throughout much of the 2010s, inflation was much lower. We could be entering an environment where we’ve moved from 2% inflation to 3% inflation:

Inflation is a big risk for bond investors who get paid back in nominal terms. The bond market could simply reflect expectations for a higher inflation environment.

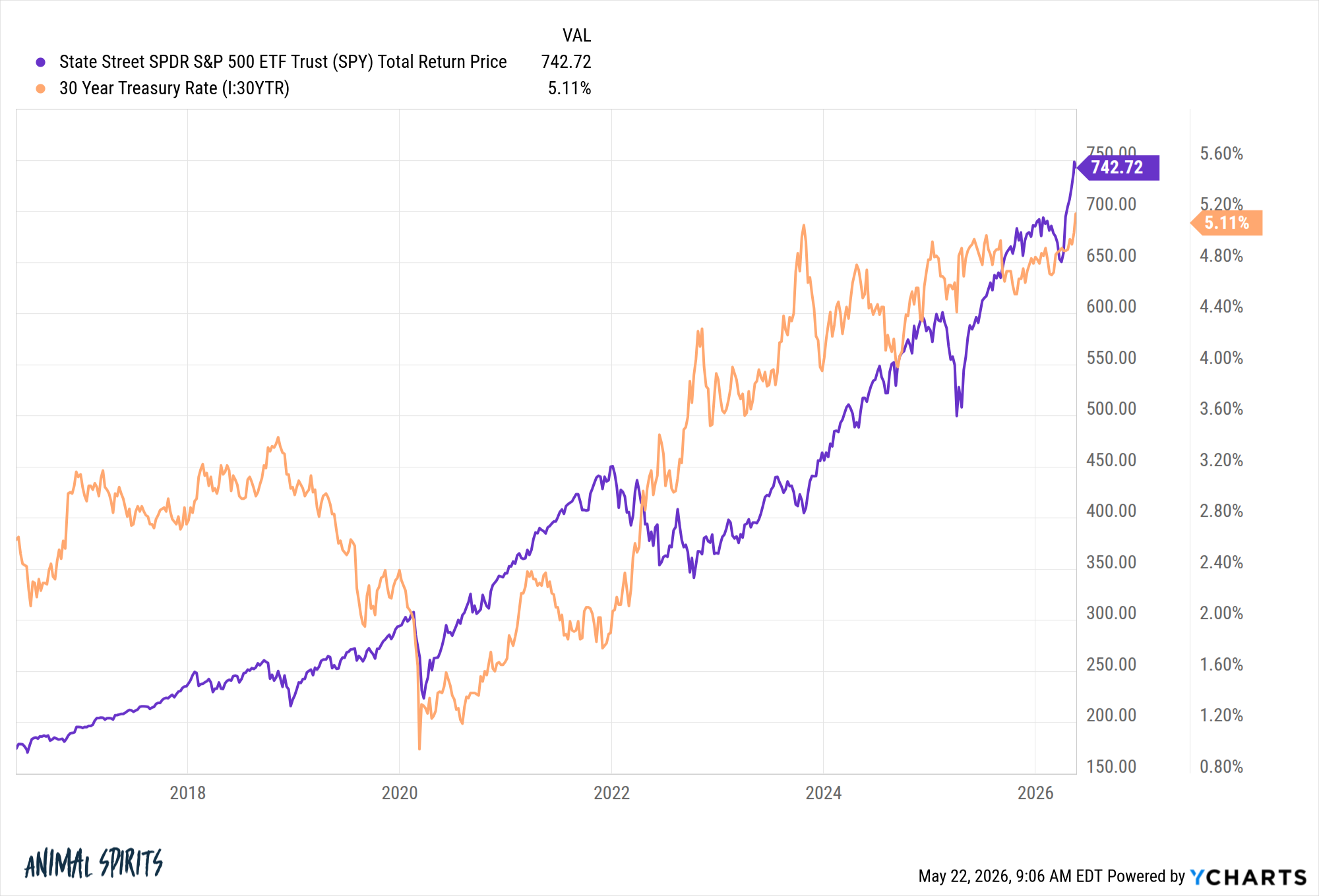

One place where there are no concerns about rising interest rates is the stock market.

The S&P 500 is not yet concerned about higher bond yields:

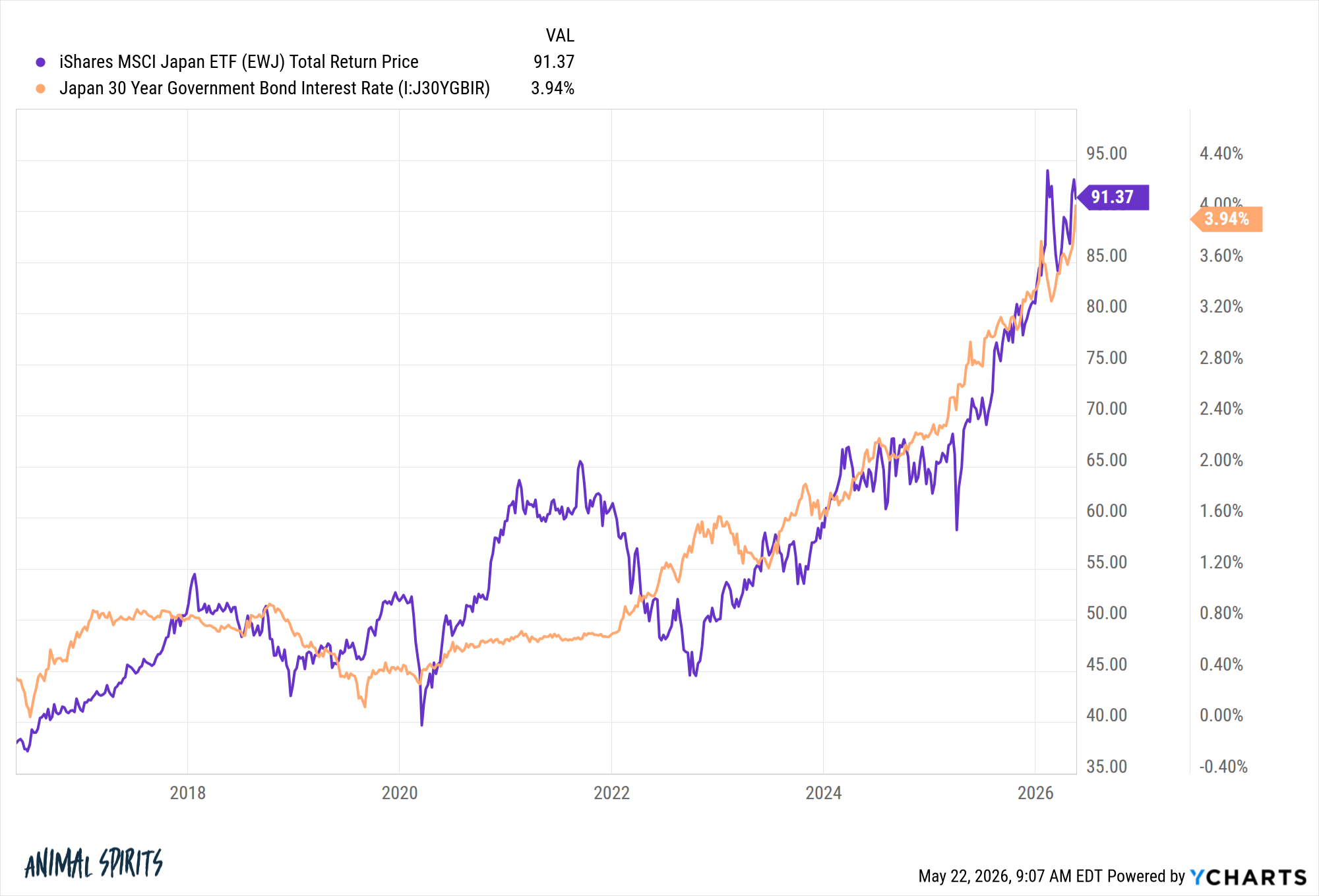

The stock market in Japan isn’t worried either:

It keeps breaking out to new all-time highs along side 30 year bond yields.

Maybe the stock market actually likes higher economic growth potential?

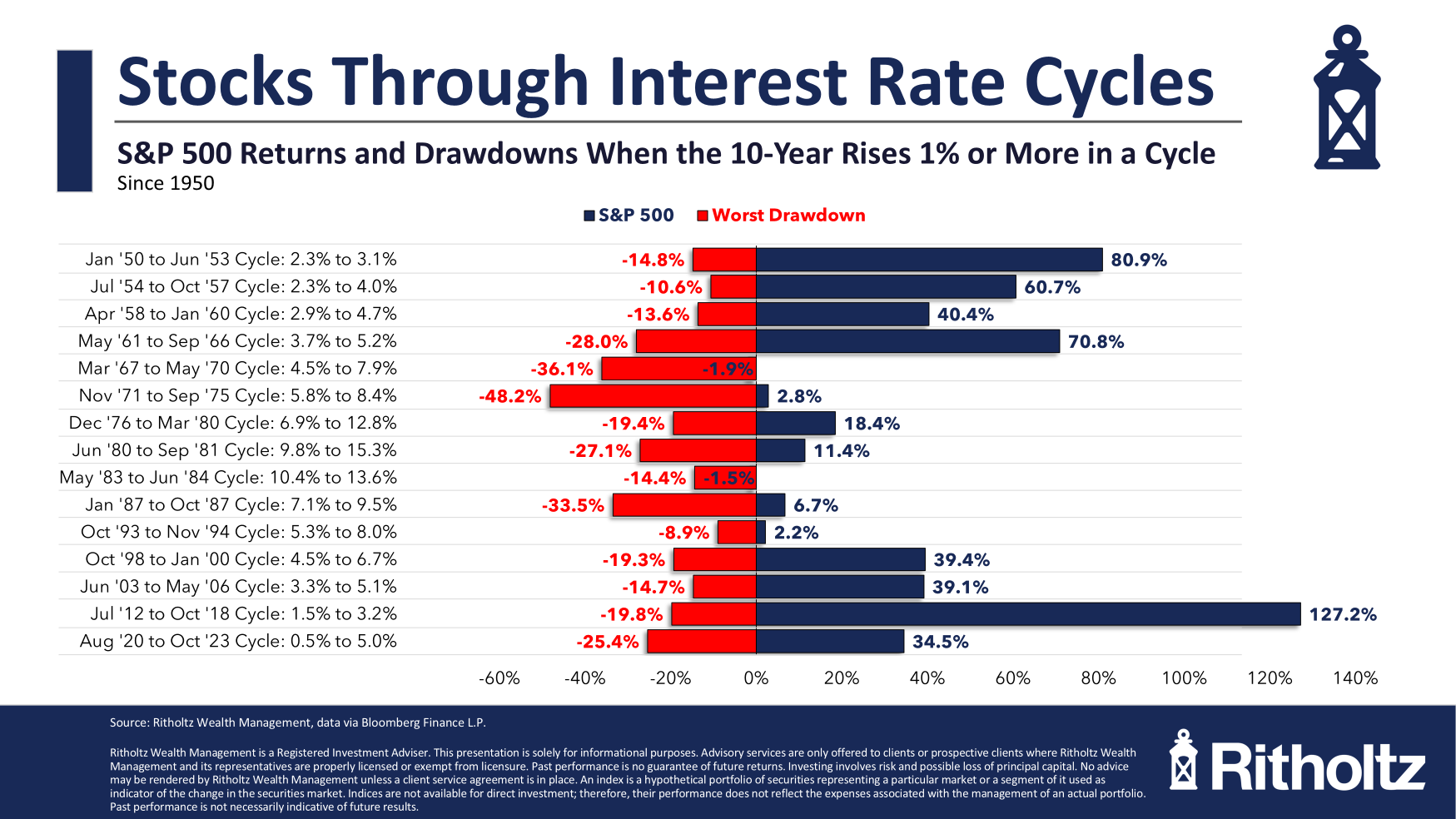

When interest rates rise in rapid fashion the stock market tends to do OK but there is also a history of corrections during these periods. Here’s a look at every rising rate cycle on the 10 year treasury along with corresponding total returns for the S&P 500 and max drawdown:

Rising rates can cause some volatility in the stock market but the longer-term results are pretty good if you can hold on.

It’s also true that rising rates are a double-edged sword for fixed income investors. Bond prices and rates are inversely related, meaning higher rates lead to lower prices.

But those new higher rates also mean higher expected returns going forward. You’re trading short-term pain for long-term gain.

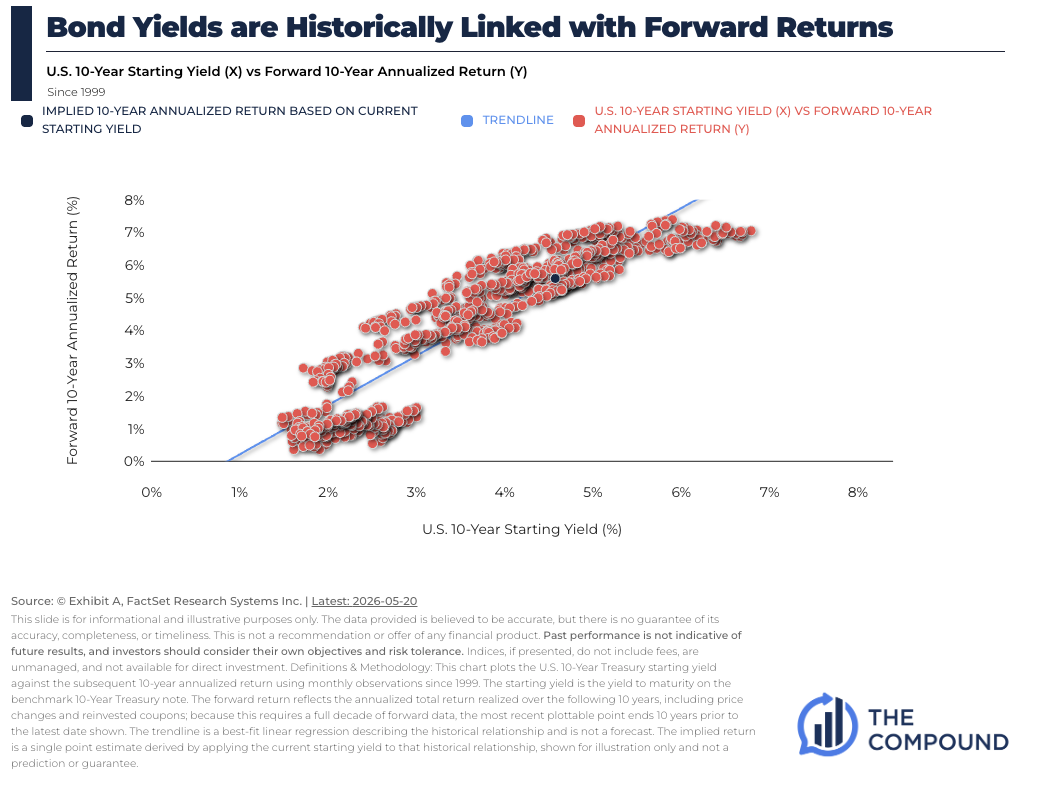

Check out the Exhibit A chart of the week:

The starting yield on a bond is a pretty good predictor of forward returns. You’re getting around 5% in high quality bonds right now.

That’s not bad.

Of course, this also means higher borrowing costs. Mortgage rates are back at 6.7%.

There is no definitive answer when it comes to rising rates. Some good. Some bad. Some unknowns.

But higher bond yields, in and of themselves, don’t necessarily spell doom for the economy or the stock market.

Michael and I talked about rising government bond yields and much more on this week’s Animal Spirits video:

Subscribe to The Compound so you never miss an episode.

Further Reading:

Buy When There’s Bonds in the Street?

Now here’s what I’ve been reading lately:

- Pretending money doesn’t matter (Contessa)

- This time next century (Monevator)

- The meaning of life (Bull & Baird)

- Perfect or better (Seth Godin)

- Software vs. semis (Chart Kid Matt)

- What you will lose when you retire (Humans vs. Retirement)

Books:

Podcast book tour: