A reader asks:

What do you think of Build Better Bond Ladders with iShares – BlackRock, for building bond ladders instead of using a bond fund/ETF such as BND? How exactly do they work when they mature and send the money back to you in terms of the money you get back? If I buy $1K of the ETF, do I get the $1K back in the year the ETF matures? Since you can buy/sell at any time, it doesn’t seem that the value would stay stable like it would if I bought a bond directly.

There are a lot of target maturity bond funds now.

Invesco has them. State Street has these bonds. Vanguard too. I’m sure there are others.

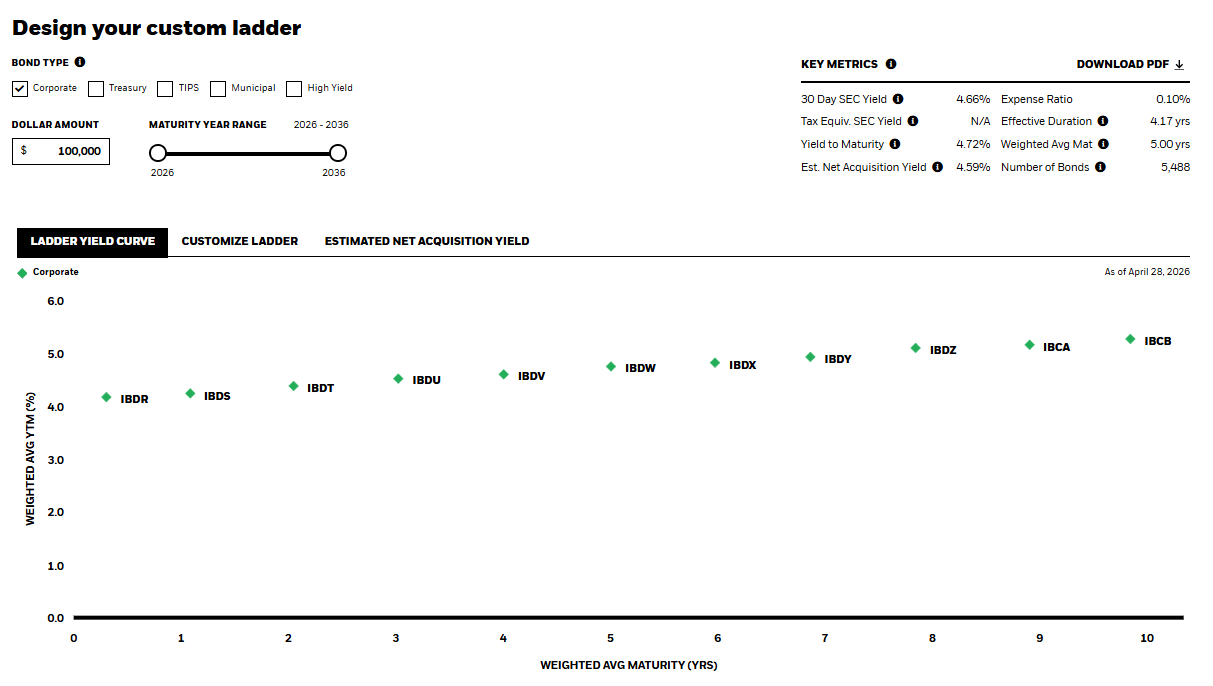

iShares has a tool that allows you to build a bond ladder using these ETFs:

You can toggle between different types of bonds — corporates, treasuries, TIPS, munies and high yield — while defining how far out you’d like to go out in terms of maturity. As you change between different types of bonds and maturity levels you can see how it will impact your yield, duration, etc.

It’s pretty neat that you can do this as opposed to going in and buying the individual bonds yourself (which can be tricky if you’ve never done it before).

So why would you buy bond funds with a target maturity?

The reason for these bonds is twofold:

1. You have a specific goal that you need money for at a specific time. If you know you need the money in 3 years for a house down payment, you could invest in a 2029 fund. If you know you’ll be paying your child’s college tuition bill in 5 years, you could buy a fund with a 2031 maturity date.

2. You want to create a bond ladder. A bond ladder is a fixed income strategy where you stagger the maturity dates of your portfolio rather than putting your money into a perpetual bond fund or a single security.

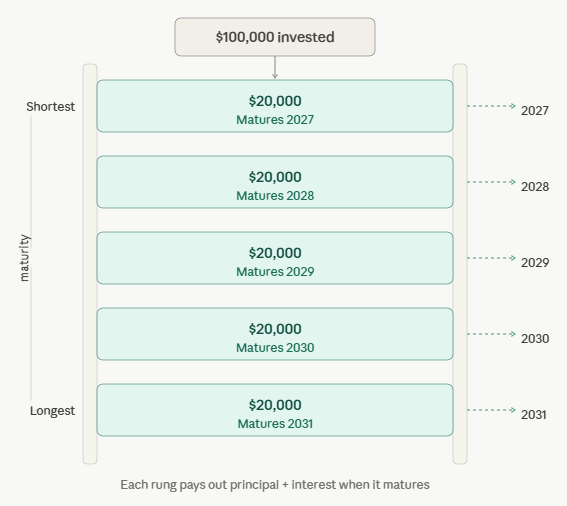

Let’s say you have $100,000 to invest.

Instead of investing it all in a single bond or fund you might create a bond ladder that goes out 5 years. You put $20,000 to work using funds with maturity dates of 2027, 2028, 2029, 2030 and 2031. It’s called a bond ladder because each maturity level is a step up to a new rung.

When those bond funds mature you could either use the proceeds for spending purposes or reinvest them back into a new bond with a 5 year maturity.

What’s the point of a bond ladder?

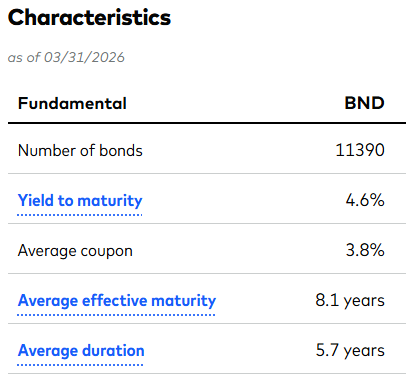

When you buy a fund like BND it’s perpetual, meaning the fund never fully matures. Currently, BND has an average maturity of around 8 years and an average duration of 5.7 years.

Those numbers can change a bit as the types of bonds in the fund may evolve over time. But the maturity of a perpetual bond fund like this never approaches zero, unlike an individual bond or one of the target-maturity ETFs.

The bond managers sell securities in the fund and buy new ones as they mature, keeping the average duration/maturity relatively consistent.

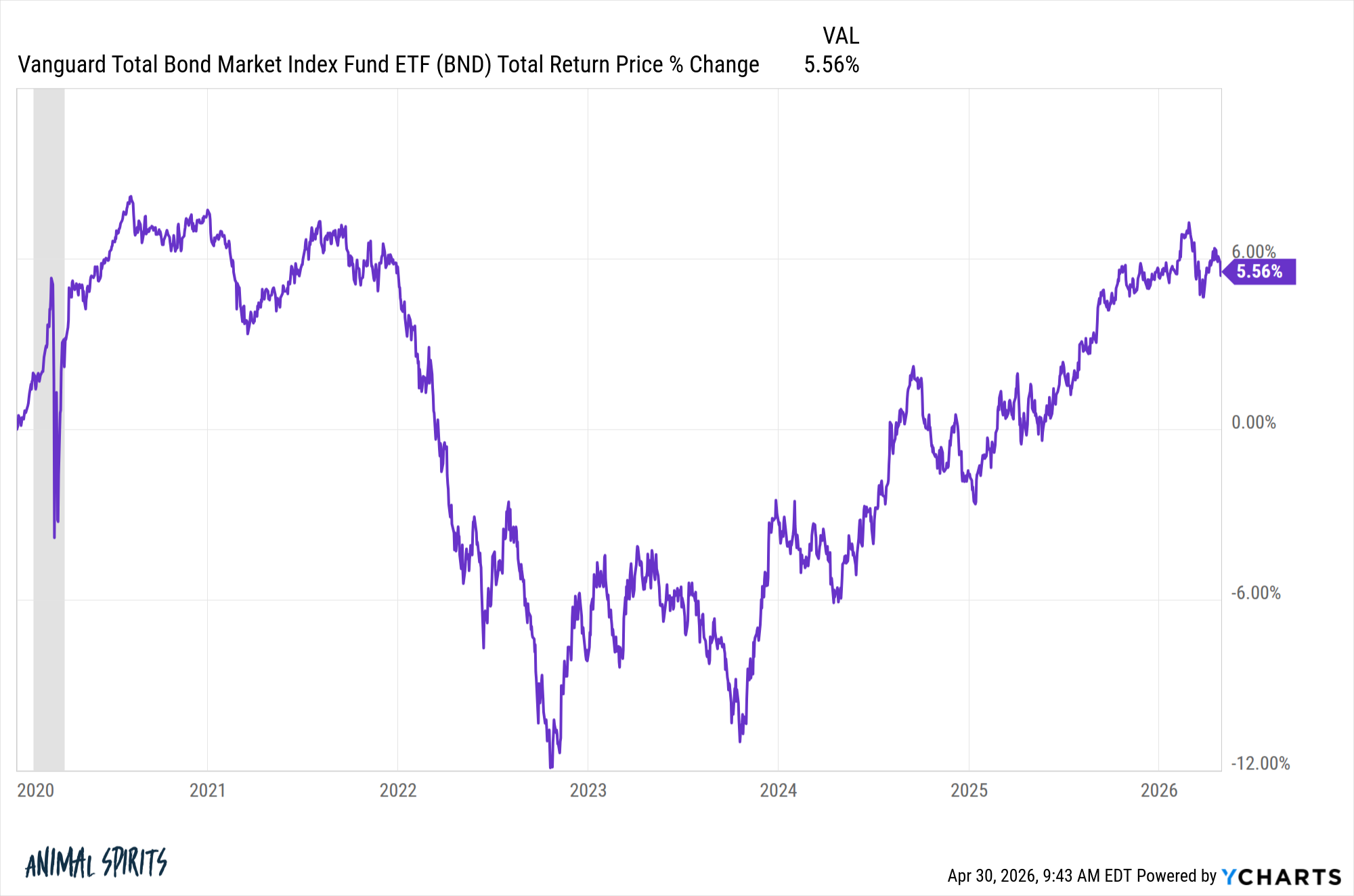

If rates rise, a fund like BND can fall in value, and it could take some time to recover. Even with income included, BND sustained a decent drawdown when rates rose in 2022:

In a recessionary environment, you would expect to see the opposite, with rates falling and this fund giving your portfolio a boost. You won’t get much of a boost in a bond ladder unless you sell the funds, which defeats the purpose.

The underlying target maturity funds will still see some movement in price as variables such as interest rates, inflation and economic growth change. But as they approach maturity, the volatility falls. Price sensitivity is lower as the par payout becomes more predictable, regardless of market conditions.

And yes, you should more or less receive par value at maturity assuming there are no defaults along the way.

A bond ladder can help when it comes to interest rate risk since you would be diversifying your entry points at different rate levels. In many ways, a bond ladder is a form of dollar-cost averaging across different yields and maturities.

However, there is reinvestment risk if you reinvest the proceeds of a maturing fund and current yields are lower.

A bond ladder can make sense for any investor who desires stable, predictable cash flows without trying to concentrate in a single point on the yield curve.

There is more maintenance involved with a bond ladder as well. You have to reinvest the maturing bonds, determine how far out you’ll go on the maturity spectrum, choose the types of bonds you want to invest in and so forth.

It’s a little more complicated.

If you need money at a specific time or you just like the comfort of knowing when your bonds mature, a bond ladder can make sense. Many retirees like a bond ladder for peace of mind.

If you would prefer more general fixed income exposure with less active management, something like BND or another bond fund makes more sense.

One option is not better or worse than the other. They each have pros and cons.

I answered this question on this week’s all-new Ask the Compound:

We also covered questions from viewers about the CAPE ratio, international diversification, how to overcome financial anxiety, and paying up for an actively managed portfolio.

Further Reading:

Individual Bonds vs. Bond Funds