A reader asks:

Every bull market it seems that there are people who like to remind us that the market’s valuations are historically high and unsustainable and they love to point out that the historical average PE is 15-20 depending on how you calculate it. We’re getting a good taste of that now – the S&P 500 PE is currently quite high so the doomers are out there predicting trouble on the horizon. However, in my opinion, comparing valuations now to historical averages requires a bit of nuance. While it’s true that the average PE of the S&P 500 is around 17ish, the average PE since 1990 is much higher than than that. Have we been in a 35 year bubble that’s sure to pop or is there some reason valuations are higher since 1990 (ie “this time it’s different”)? Ben loves delving into market history, so I would like to hear his thoughts.

I do love a good delve into market history and this is a worthwhile topic.

The greatest book ever written about the concept of risk is Against the Gods by Peter Bernstein.

He has an entire chapter on regression to the mean that applies here.

In the book Bernstein writes about Sir Francis Galton’s experiments with peapods. Galton planted seeds of different sizes — small, medium and large — to see how it impacted the size of their offspring. Galton noticed that the offspring of very large seeds tended to be smaller than their parents, while the offspring of very small seeds tended to be larger than their parents.

Both above-average and below-average tended to move back to average over time.

This is what many investors have been wondering about for years now when it comes to stock market valuations. When does that regression to the long-term mean finally hit the U.S. stock market?

Here’s the monkey wrench — Bernstein also wrote about why regression to the mean can be so tricky outside of science:

There are three reasons why regression to the mean can be such a frustrating guide to decision-making. First, it sometimes proceeds at so slow a pace that a shock will disrupt the process. Second, the regression may be so strong that matters do not come to rest once they reach the mean. Rather, they fluctuate around the mean, with repeated, irregular deviations on either side. Finally, the mean itself may be unstable, so that yesterday’s normality may be supplanted today by a new normality that we know nothing about.

That last point is the thread I want to pull on some more.

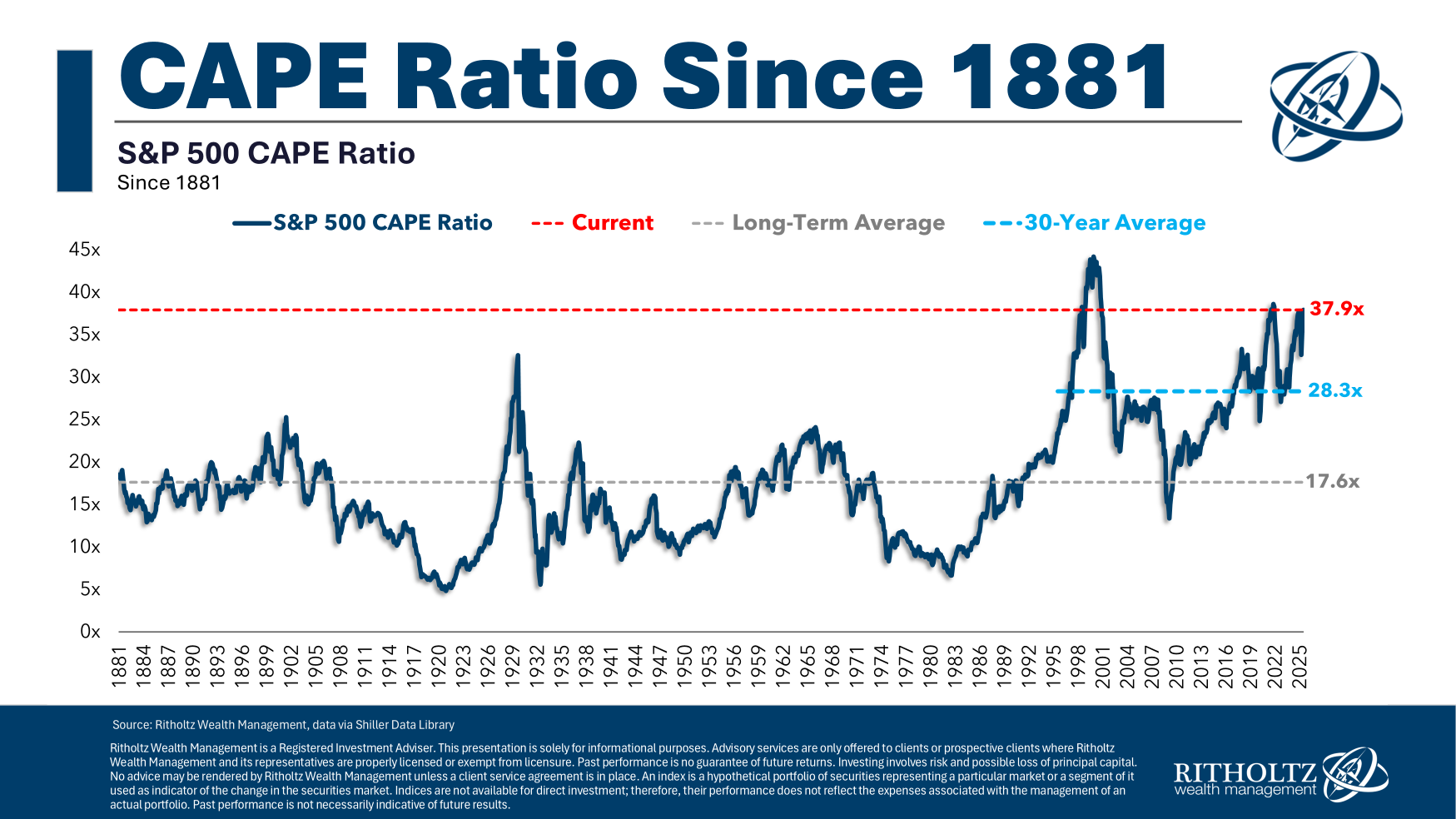

This is the CAPE ratio going all the way back to a time when Francis Galton was still alive:

What’s more relevant here — the 150+ year full history or the past 30 years? Which average is more relevant?

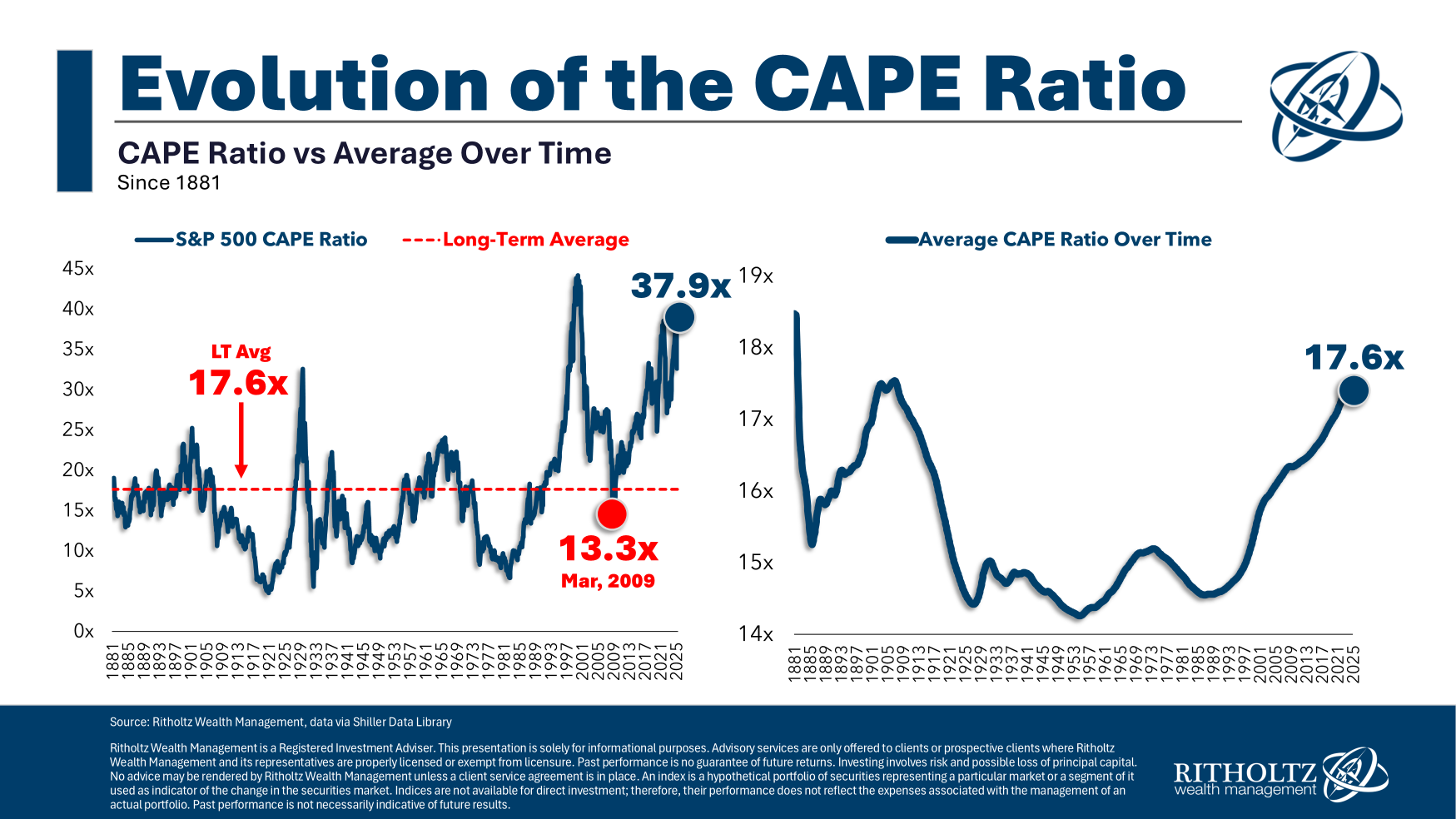

Here’s another way of looking at the evolution of valuations over time:

There was some mean reversion at the bottom in 2009 but it was brief. Valuations have been trending higher for decades now.

One of the main reasons to keep an open mind about valuations being a moving target here is the companies have evolved so much over time.

Last week I wrote A Short History of the S&P 500 which looked at the composition change to the index over time in terms of the types of stocks. The S&P 500 was full of capital-intensive industrials and railroad stocks for much of its history. These were relatively low-margin businesses that required a large number of employees and lots of physical assets that needed to be replaced over time.

Today’s companies have more intangible assets and are far more efficient.

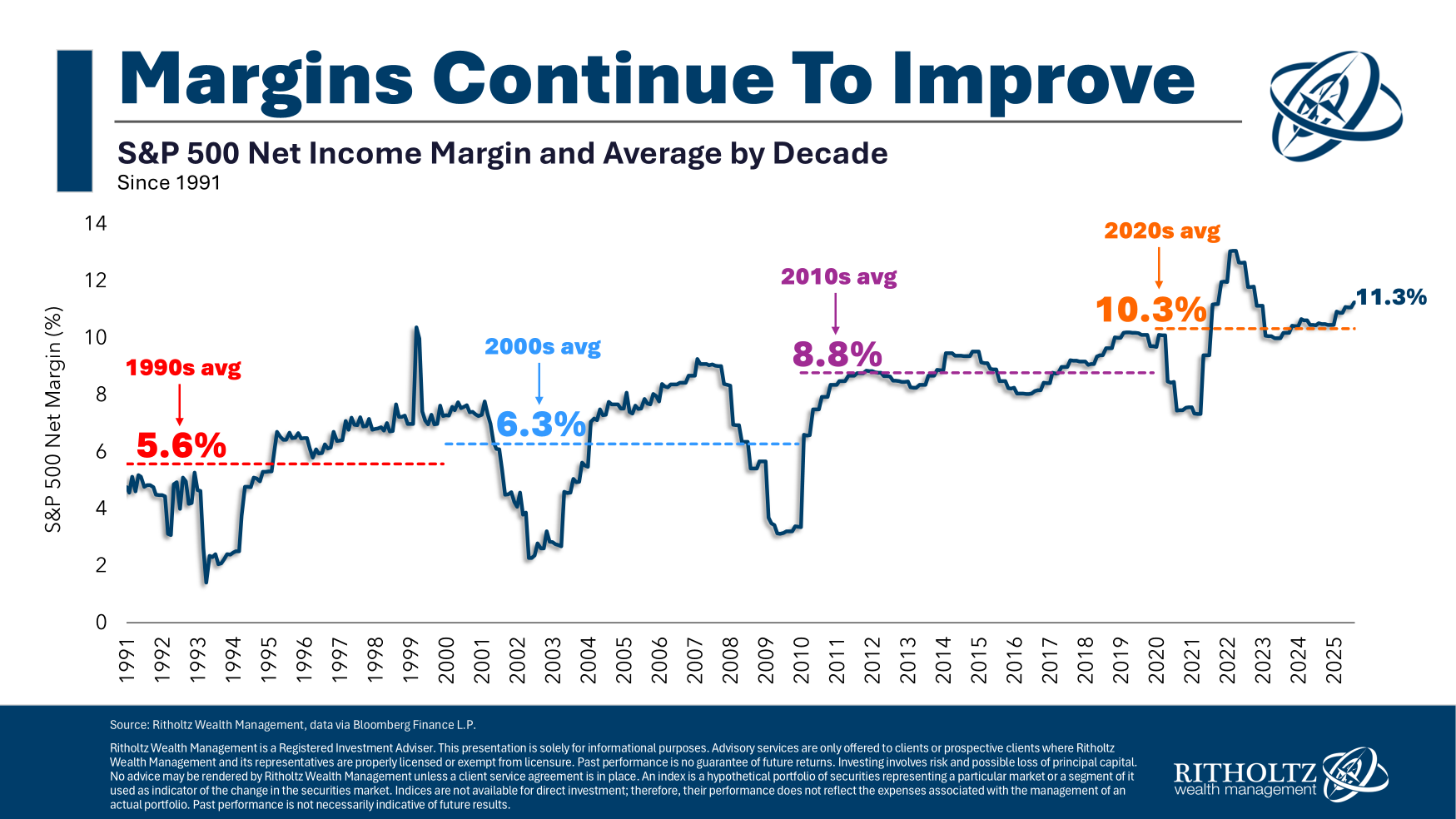

Take a look at average margins by decade going back to the 1990s and you can see this shift happening:

Every decade the average moves a little higher.1

This was supposed to be the most mean-reverting series in all of finance. Market historians have been shouting it from the rooftops for the past 15 years. And they were wrong.

This time really was different. The companies are different. The business models are different. The technology is different.

It’s a new world.

However, even if we agree the past 30 years are more indicative of stock market characteristics, even today’s valuations require some context.

The JP Morgan Guide to the Markets has some really great charts that do just that.

This first one looks at the current environment with respect to forward PE, dividend yield and 10 year treasury rate and compares them to prior peaks before the most recent bear markets:

It’s interesting to note that the biggest crash on this list–the Great Financial Crisis–started at relatively muted valuation levels. Stocks were not insanely overvalued heading into the fall of 2007. It’s just that no one saw earnings were about to fall off a cliff.

Picking tops is not easy.

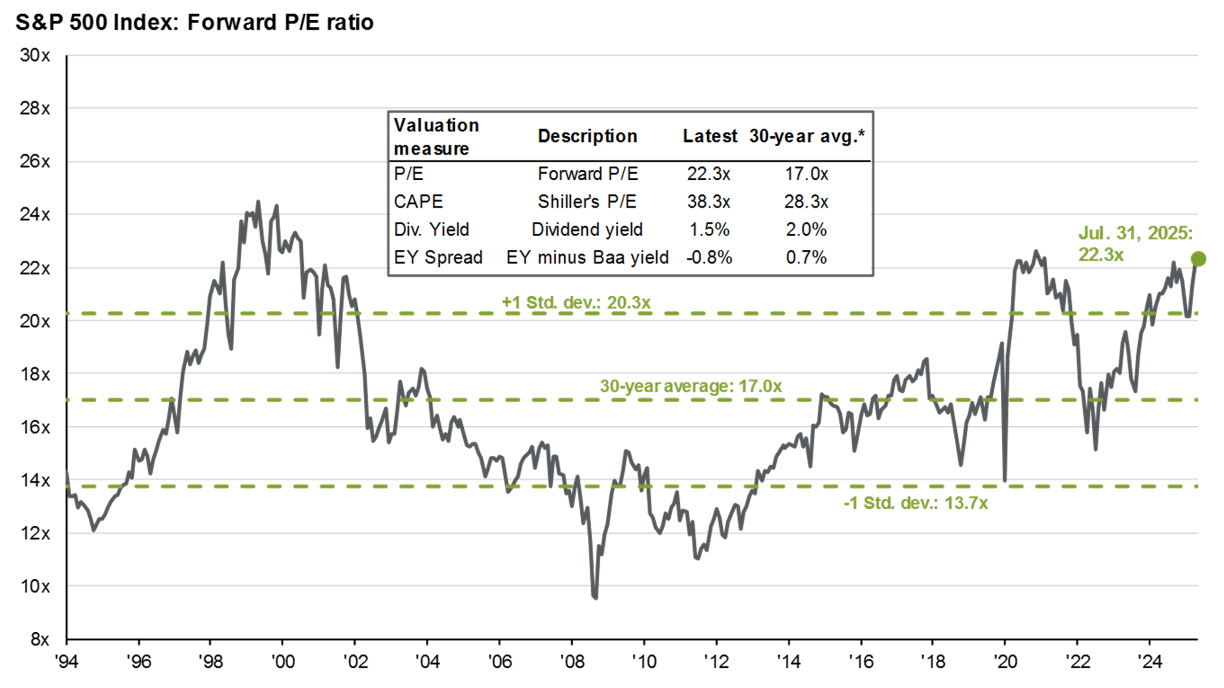

The next chart compares various valuation metrics to their 30 year averages:

They’re all elevated compared to the past 3-decade averages.

And it should be this way!

We have the biggest, best companies. We’re on year 16 of an epic bull market. It would be strange if the stock market weren’t overvalued given the performance of the stock market this cycle.

However, it should be noted that most of this overvaluation is concentrated in the megacap tech stocks.

Here’s one more from JP Morgan that shows the valuations of the top 10 stocks vs. the S&P 500 overall and the remaining stocks in the index:

Valuations outside of the top 10 are elevated as well but not nearly as much as the hyperscaler tech stocks.

Where I stand on this question is that yes this time is definitely different. We have never seen companies like this before that are this big and efficient with such high profit margins. But the market knows this and it sure seems like it’s more or less priced in at this point.

Just look at the earnings and revenue surprises from Nvidia over the past few years:

Fool me once…

Analysts have ramped up their expectations, as they should.

If these companies continue to grow and meet or exceed expectations, things should be fine.

But there is little margin for error if they stumble or fail to meet the now lofty expectations.

This time is different but trees still don’t grow to the sky.

Good luck predicting how high they can get before they fall.

I did a deep dive into this question on the newest episode of Ask the Compound:

Everyone’s favorite tax expert, Bill Sweet, joined me on the show as well to discuss questions about Roth IRAs, winning the Powerball lottery, income-based investment strategies and when to do a Roth conversion in your workplace retirement plan.

Further Reading:

Is This 1996 or 1999?

1It’s crazy that we’ve dealt with a pandemic, supply chain shocks, 9% inflation and now tariffs yet margins have moved higher this decade. Good luck betting against corporate America. They do whatever it takes to protect their profits.