A reader asks:

100 Years is a heartbeat in terms of the scale of human history. What are the odds that capital might become so bountiful and technological innovation so fast that stocks fall and stay underwater forever? I never hear mainstream (keep buying) advisors even entertain this possibility.

This question was in response to one of the many market studies I’ve done over the years.

I get variations of this question all the time — what if stocks for the long run isn’t meant to last?

There’s plenty to cover here but first a history lesson.

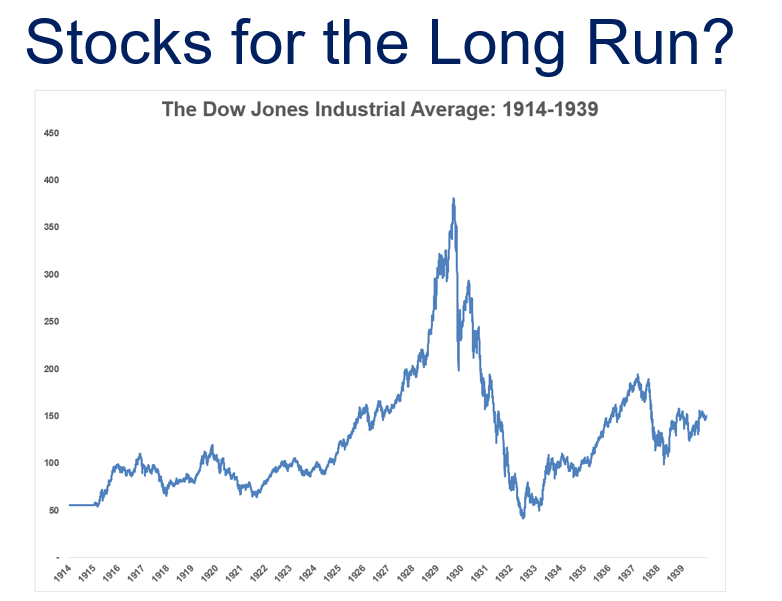

The entire idea of stocks for the long run is still relatively new. Investors certainly didn’t feel that way in the 1930s and 1940s after witnessing the stock market fall 85% during the Great Depression. Can you blame them?

Plus, very few investors knew what the long-term returns in stocks even were before the 1960s.

No one had the data.

That is, until a VP at Merrill Lynch named Louis Engel stepped up to the plate. Engel was tasked with figuring out the long-term returns for the stock market so he could give Merrill’s brokers some ammo when talking to clients and prospects. No one really had the data in one place so Engel went to the Chicago School of Business who said they would perform the historical study if Merrill would fund the research.

A group of professors were able to put together a dataset of NYSE-listed stocks from 1926-1959. The process took nearly four years to complete, which created what is now known as the Center for Research in Security Prices (CRSP).

They now had a long-term historical record of U.S. stock market returns, which were much better than most investors assumed.

Despite that gargantuan crash in the depression, the U.S. stock market was up more than 2,700% in total from 1926-1959. That’s 10.3% per year.

Just for fun I decided to look at the annual returns in the aftermath of that study:

Pretty close.

We have about 100 years of good stock market data, but we’ve only known about it for 65 years. I completely agree that this is a drop in the bucket in terms of our history as a species. Everyone would feel much more confident about historical market data and relationships if we were working with 1,000 or 10,000 years of data.

However, even if we had a much longer history to study, the future would always have the same exact level of uncertainty. There is always the chance of a paradigm shift no one sees coming.

Historical data is not perfect but what other choice do you have? The old saying, “I would rather be approximately right than precisely wrong,” seems to fit here.

I’ve had plenty of people ask me about a Japan-like situation where stocks go nowhere for decades but this question sounds more like a Star Trek situation. I’m not a Trekkie but my general understanding of the series is that technology solved many big problems through abundance — poverty, disease, work, the environment, etc. — which allowed them to explore new galaxies and civilizations.

Anything is possible, although I find it hard to believe that the biggest corporations in the world would sign up for technologies that essentially put them out of business.

I understand why certain investors worry about the stock market breaking. It’s a scary possibility, but I don’t think it makes sense to waste your time worrying about it.

Whatever the reason is, if the stock market doesn’t go up over the long haul you’re going to have much bigger problems than your portfolio. Your investments won’t matter.

Also, let’s say you are trying to hedge against this doomsday scenario. What’s your plan? Bury your money in your backyard? Hoard bullets and gold bars?

My baseline assumption is that human beings will strive to earn more money and better their station in life. Corporations will innovate and look for ways to increase profits. The economy will grow. Bad things will happen but the long run will see progress.

Maybe these baseline assumptions will prove to be wrong in a dystopian future but I don’t see how you could possibly prepare for that situation short of building a bunker under your house.

What’s the point of investing if you don’t think the future will be better than the past and present?

The only way to ensure you will fail as an investor is to avoid investing in the first place.

I did a deep dive of this question on this week’s Ask the Compound:

Bill Sweet joined me again on the show this week to discuss questions about putting all of your retirement assets in a Roth IRA, how to make a career shift to finance, how to save for your child’s future, tax considerations when moving out of Florida and more.

Further reading:

Risk Free S&P?