Institutional investors made a huge push into hedge funds following the bursting of the dot-com bubble.

It was the perfect environment because you had a situation where expensive stocks crashed while cheap stocks were a wonderful hedge. Going long cheap and short expensive allowed them to win in both directions.1

The S&P 500 got clobbered so it wasn’t hard to sell hedge funds to all of the pensions, endowments and foundations. Investment committees ate this stuff up.

The number of hedge funds around the global tripled from around 3,000 in 1998 to more than 9,000 by 2007 heading into the Great Financial Crisis.

Institutions were hopeful hedge funds would replicate their success from the early-2000s during the next crisis. It didn’t happen. The industry did about as well as a 60/40 portfolio with worse liquidity and higher fees.

Sure some hedge funds knocked it out of the park but most were disappointing during the 2008 crash. As Ray Dalio once observed about hedge funds, “There are about 8,000 planes in the air and 100 really good pilots.”

I witnessed this firsthand. The endowment fund I helped manage had roughly 10% allocated to hedge funds. We had a managed futures fund that was up in 2008 but other than that every other hedge fund we owned didn’t hedge all that well in 2008.

Then coming out of the crisis every hedge fund went directly into the fetal position. They all turned defensive because the institutional investors all turned defensive.

One of the long/short funds we invested in exemplifies this phenomenon.

The manager told us in 2009 he would be more defensive going forward because the bulk of his net worth was invested in the fund. Skin in the game is great and all but in this case it caused the portfolio manager to miss out on a massive bull market because the financial crisis left so many scars.

Plenty of hedge funds couldn’t get out of the crisis mindset in the 2010s to their own detriment. It sounds like legendary investor Seth Klarman is one of those hedge fund managers.

Bloomberg had a story this week on the struggles of Klarman’s Baupost Group:

Clients of Seth Klarman’s Baupost Group pulled roughly $7 billion from the hedge fund in the past three years, losing patience with the famed value investor after a decade of lackluster returns.

Baupost, once among the best-performing hedge funds, gained only about 4% a year since 2014, according to investors.

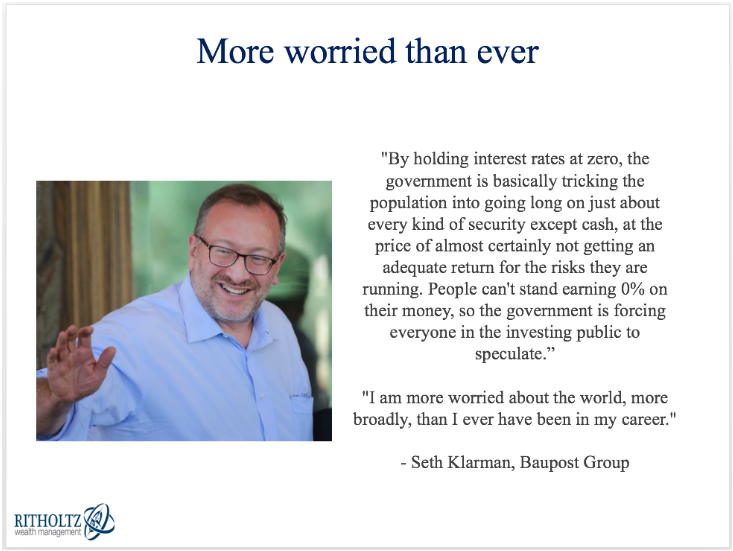

Klarman is a legend but I can’t say I’m surprised. Here’s a slide I used in a presentation a number of years ago:

Heading into the 2008 financial crisis Klarman has compounded his fund at 20% per year for 26 years! When an investor of that stature says he’s more worried than he’s ever been in his career, alarm bells start going off.

Klarman made this dire proclamation to Jason Zweig all the way back in May of 2010. The U.S. stock market is up almost 600% since his warnings.

It sounds like Klarman has regularly kept something like 20-30% of his fund in cash throughout the bull market.

I don’t know the exact reason for his defensive posture. Career risk. Fighting the last war. Value investing has been severely out of style. Maybe it’s some combination of a variety of factors.

It’s also possible he made a boatload of money over the years and entered capital preservation mode.

I don’t write all of this to put down a legendary investor.

Either way Klarman will be fine. He’s already a billionaire. And despite earning cash-like returns for a decade during a hard-charging bull market, he probably still made a killing on hedge fund management fees from his investors.

It is important to understand how your experiences, track record and place in your investing lifecycle can impact your perception of risk.

Coming out of the Great Financial Crisis, many investors were far too cautious because of how scary that environment was.

It will be interesting to see if the opposite is true if the current cycle ever turns and certain investors become enamored with too much risk.

Further Reading:

The Golden Age of Hedge Funds

1I’m generalizing here because there are far more types of hedge funds than long/short.