A reader asks:

Is it crazy to be 100% in stocks from age 32 to sometime in my 50s for my retirement accounts?

And another reader asks a similar question:

I don’t get why people work a 30+ year career while investing in stocks only to glide path into a heavier bond allocation around retirement. Why not just stay 100% in stocks, benefit from share price appreciation and collect dividends for life?

Both of these questions came about from a recent post I wrote that contained this long-term stock market data:

I’m a huge proponent of long-term thinking when it comes to investing but even over the short-term the results for the stock market hold up surprisingly well historically speaking.

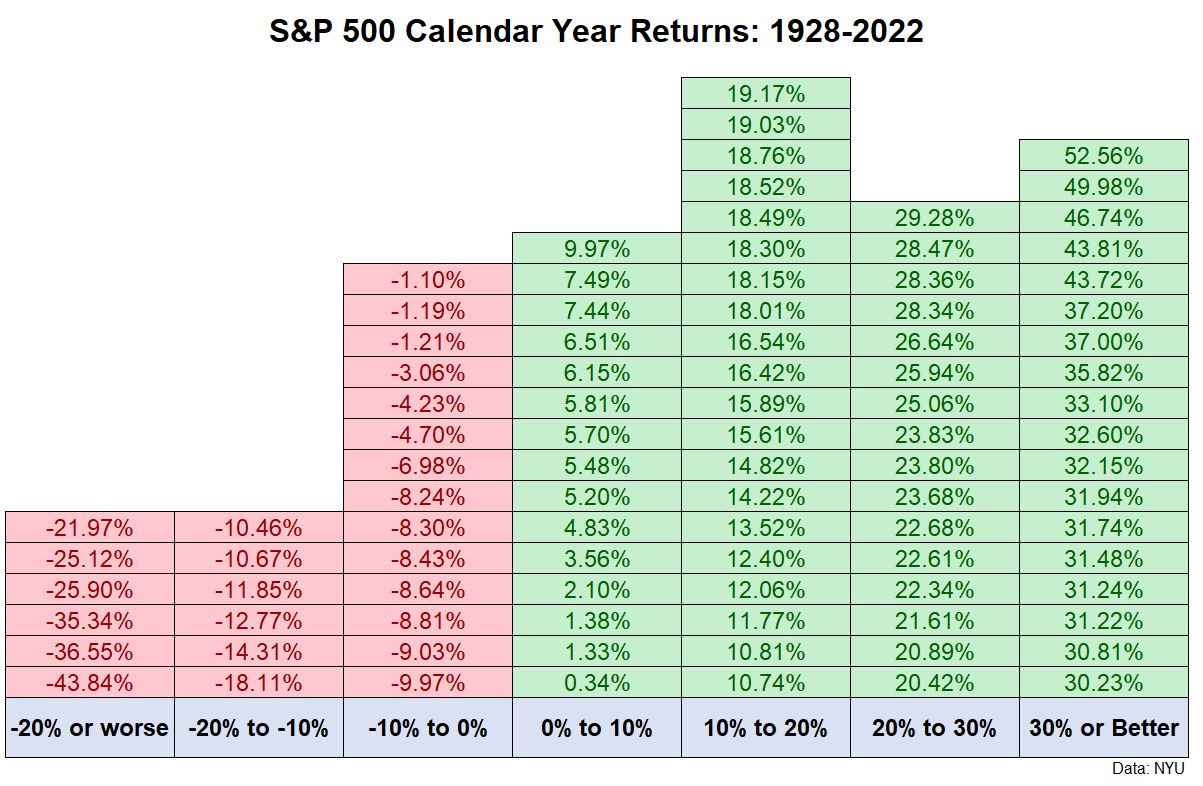

One of the craziest things about the historical performance of the U.S. stock market is you have been more likely to earn a return of 20% or more in a given year than experience a loss.

Over the past 95 years, there have been 34 times when the S&P 500 has ended the year with gains in excess of 20%. That’s more than one-third of the time.

There have only been 26 times when a year ended in a loss or a little more than 25% of the time.

When you combine this with the fact that stocks as an asset class have offered higher returns than bonds or cash, it’s understandable that investors would question why they should allocate to other investments.

So does it make sense to keep 100% of your portfolio in stocks?

Allow me to answer this in the most finance way possible — it depends.

In theory, young people investing for retirement should absolutely have 100% of their portfolio invested in equities.

The biggest risk in the stock market is a crash which brings lower prices.

Your best-case scenario as a young saver/investor is that you get to put more savings to work at lower prices. This assumes you have the fortitude and ability to continue saving when times get tough but your biggest asset when you’re young is human capital (your future earning and savings power).

However, as you age that human capital slowly dwindles and your portfolio eventually becomes your biggest asset.

Most older investors allocate at least a portion of their portfolio to cash or fixed-income assets at this point because they no longer have as much time to wait out bear markets or save more money at lower prices.

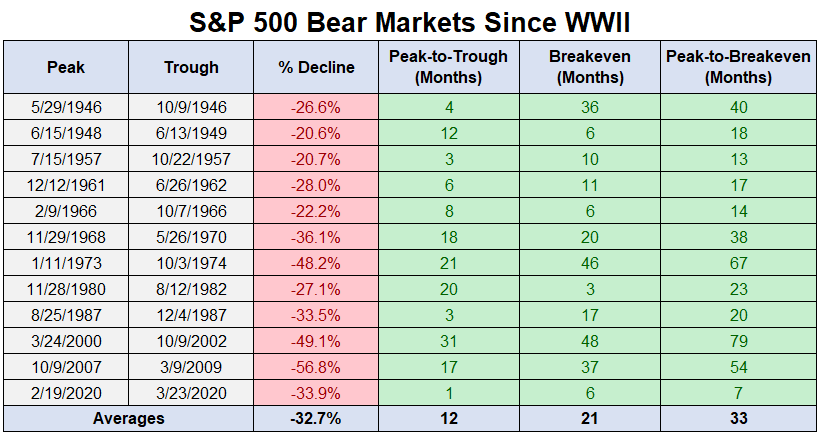

Look no further than the history of bear markets to see why most investors tend to get more conservative as they age and their financial assets grow:

The average bear market lasts about a year from peak-to-trough. But the average time to break even is closer to 3 years.

The shortest bear market in modern times was the Covid crash which took just 7 months to reach new all-time highs again. The longest was the 1973-94 bear market which took almost 6 years.

That is a long time to be selling off your stocks when they are down.

The whole point of switching from a mindset of accumulating wealth to preserving wealth is you don’t want to get into a situation where you are forced to sell at a big loss during a market crash. Cash reserves and bonds can help in that situation to give your stocks some time to come back.

I do understand the desire to continue compounding your assets even in retirement.

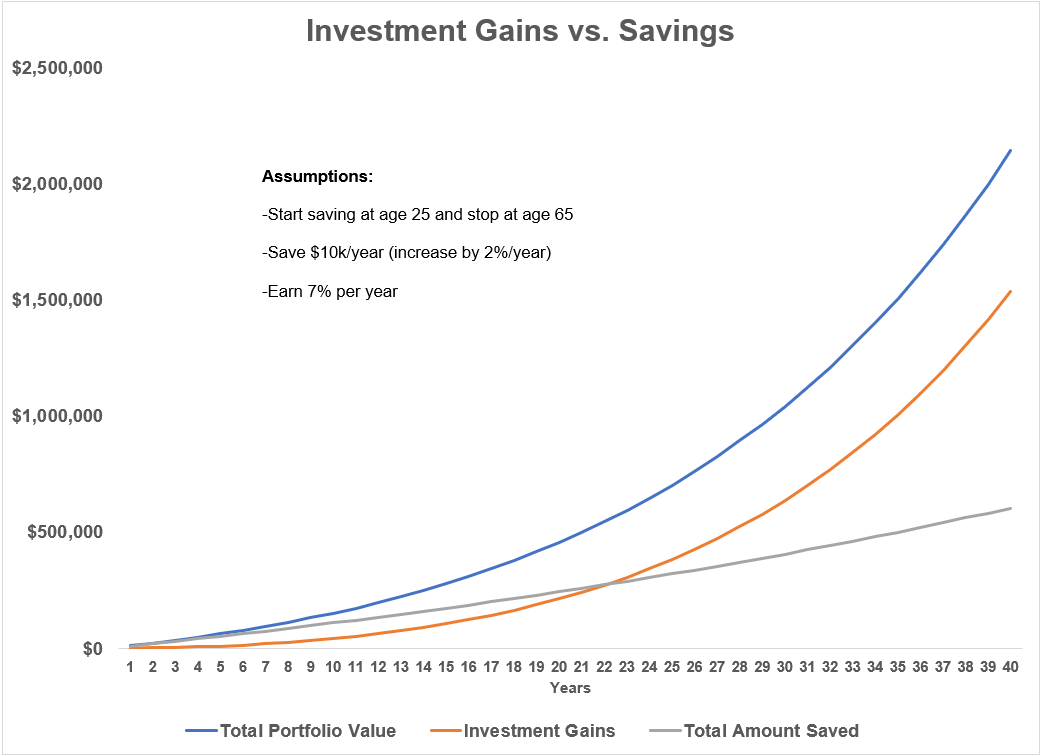

The simple math of compounding shows that the majority of your dollar gains will come later in life once you’ve built up a war chest of assets.

Let’s assume you start saving $10,000 a year at age 25, increase that amount by 2% per year to account for inflation, grow your assets at 7% per year and do so for 40 years when you retire by age 65.

Here’s how things shake out in terms of saving vs. investing in this simple example:

In this example, your investment gains don’t overtake the total amount saved until age 48.

At year 20, investment gains from compounding make up around 45% of the ending value. By age 65, compounding accounts for more than 70% of the overall value.

Saving is far more important the younger you are while investing matters a whole lot more as age and build up your savings.

Obviously, no one’s actual retirement plan works out as neatly as it does on a spreadsheet. But there is something to be said about allowing your assets to continue compounding even while you are retired.

Like most things in life, there are trade-offs involved when thinking through this exercise.

The stock market can rip your face off in the short-term but remains your best long-term bet when trying to beat the rate of inflation over the long haul.

I suppose some investors could live off the dividends from their stock portfolio but those cash flows aren’t set in stone. The 2008 financial crisis saw dividends fall by more than 31% for the S&P 500. That was far less than the 56% crash in prices but would still be painful from a cash flow perspective.

I’m 41 years old. My retirement portfolio is 100% in stocks or equity-like investments with a time horizon of well over a decade.

But I also keep a liquid reserve in cash or short-term bonds for shorter-term goals, spending needs or emergencies.

I would imagine that liquid reserve will grow as I approach retirement and my time horizon changes but I will always have a decent allocation to stocks.

The answer to the question of how much to keep in stocks is more about your emotions than what finance theory says.

Some investors, even young ones, need an emotional hedge because it can be difficult to see your life savings seemingly evaporate before your eyes on occasion in the stock market. Others understand the volatility involved in the stock market and don’t need as much fixed income to survive.

As always, portfolio management requires some balance between your ability, need and willingness to take risk with your money.

There is no universal answer for every investor so it’s important to think through both the upside surprises (long-term compounding gains) and the downside shocks (lengthy bear markets).

We touched on these questions and more on the latest Portfolio Rescue:

Our tax expert Bill Sweet joined the show again to help us answer questions on the tax issues with early retirement, the child tax credit when you have a child and how to use multiple tax-deferred retirement accounts at the same time.

Further Reading:

Some Stuff That Probably Won’t Happen in 2023

Podcast version here: