My colleague Josh Brown had an excellent piece in the most recent Fortune Magazine that asked a simple, yet loaded question:

Are You Ready for the Next Bear Market?

As we’ve seen from the seemingly never-ending market crash predictions over the past few years, no one really knows when the next bear market will hit. But we do know that bear markets are a natural outcome when you mix an uncertain future with human emotions that tend to take things to the extremes on the greed and fear spectrum.

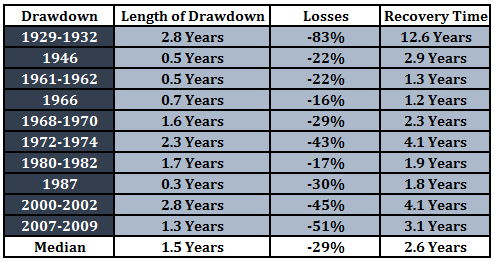

Here are ten of the worst bear markets* since 1926:

I’m a huge proponent of thinking and acting for the long-term to be successful as an investor. But to be able to take advantage of the long-term you have to be able to make it through the short- to intermediate term. As you can see from this chart, the time it takes to round-trip from some of the worst drawdowns, which can last for a number of years. On average, it has taken the stock market roughly 4-5 years to recover back to the prior peak. In my experience, these periods are where the majority of mistakes are made by investors.

One of my biggest realizations from working in in the institutional money management business during the financial crisis is that far too many organizations were unprepared for a severe market disruption. They didn’t understand what they owned. It turned out that many of their portfolios were operationally inefficient. They didn’t have sufficient liquidity to survive or even take advantage of opportunities from the brutal bear market. And the worst part is many organizations were forced to cut back their spending distributions from their portfolios. Many charitable organizations had to lay people off because of it.

One of the things I’m most excited about in my new role with Ritholtz Wealth Management is that I get to help institutions create investment plans that will give them a high probability for success during these situations. That means not only achieving their long-term goals, but also surviving severe market disruptions without compromising the organization’s mission.

Financial markets are a complex adaptive system, so the automatic response by the majority of institutional investors is a complex investment structure. These complex portfolios basically work until they don’t. And when they don’t work it’s usually at the most inopportune times. With private securities, fund lock-ups and gates on investor redemptions there is no diversification benefit because you can’t rebalance to take advantage of market volatility. You become a forced seller elsewhere in your portfolio, which is a position you never want to find yourself as an investor.

My experience has been that the best risk controls an institution can implement to survive these serious market disruptions exist within a straightforward, transparent and sufficiently liquid portfolio. So what’s an investor to do with the knowledge that a bear market will hit some day, but we don’t know when?

In the words of Howard Marks, “You can’t predict. You can prepare.”

Our team spends a lot of time and effort thinking through this eventuality. Next month I’m going to be meeting with prospective clients who would like to hear some of our thoughts on how we position our investment plans to survive the next bear market. If you’re involved with an institutional fund in any capacity or are an individual investor who would like to learn more about out process, we’d love to meet with you.

I’ll be giving presentations in our New York City office on November 18th and 19th.

Email to info@ritholtzwealth.com or you can contact me directly for more information. Or you can call 212-455-9122 and ask for Erika. Learn more about our institutional practice at Ritholtz Wealth Management here.

*I used monthly total returns on the S&P 500 in this data series from Returns 2.0.

“On average, it has taken the stock market roughly 4-5 years to recover back to the prior peak.”

Your data (and up to 2015) shows there to be a downturn every 8.5 years on average. Which could mean that a buy-and-hold stock-heavy portfolio might be underwater 50-60% of the time. Yikes!

Makes sense, though, as most market gains are achieved in shorter periods than are spent down or sideways.

Any info on the peak-trough-peak timeline? How long was the actual downturn vs the recovery?

The market goes up most of the time (7 out of every 10 days with a new high ever 18th day since 1928 is my understanding; correct me if I’m wrong). The amount of your investment will almost certainly be higher at the start of a new bear market than the amount at the start of the previous bear market. So you aren’t really underwater (which I interpret as less than your initial investment).

Also most people are dollar-cost-averaging over time in their retirement plans and bear markets should be viewed as sales days in stores. Unless you lose your job but hopefully you have enough to tide you through. I had a 9 month period in 1994 where I was unemployed but got thru with unemployment benefits, savings, reduced spending, military reserve drills, some increased debt but did not touch retirement funds. Ended up with a better job too.

I should have specified this — the ‘Length of Drawdown’ is the peak-to-trough. ‘Recovery time’ is trough-to-peak.

See my Cash Reserve Method. Also, once the market or market segment has dropped into bear territory, start buying into it in relatively small increments via dollar cost averaging over at least a 1.5 (average length of a bear market per your stats) year period.

The losses since the early ’80’s have been deeper each bear market…from 17% up to 51% in the most recent bear market. Interesting.

Yes, more spread out than in previous years but also more severe.

[…] Surviving the next downturn – meet with Ben Carlson in New York! (A Wealth Of Common Sense) […]

Im surprised, the 1937 bear market is not here.

These were peak-to-trough losses until the market completely recovered back to the prior peak. By 1937 the market still had not gained back all the losses from 1929-32. More on 1937 here:

https://awealthofcommonsense.com/market-returns-during-ray-dalios-1937-scenario/

Thank you Ben, great catch.

Can lockups and illiquid investments sometimes be a blessing in disguise? I wonder if they don’t prevent some investors from panic selling in the depths of a crisis?

That’s valid. They could act as a behavioral helper. The problem is the denominator effect — when stocks fall big and PE or VC is not marked down for quite some time it takes on a much bigger portion of your portfolio. If you’re following asset allocation policy guidelines you’ll be way overweight those investments, but you won’t be able to rebalance out of them when you need to.

Am I correct in concluding that you are not saying you will help clients avoid bear markets, but will help them survive them? This doesn’t mean they will not experience losses, right? In 2008 all asset classes went down.

Great article. I always appreciate your charts and the insight that they bring. It seems to put bear markets into perspective with their length and recovery. I also like how you don’t presume to fully understand every nuance about the complex bear markets. Thanks. I think i am ready for when it hits . . . . http://www.13monthsecuador.blogspot.com

Ben this is great work. I wish there are some analysis like this for some international markets like Aust, UK with long history. I am a Singaporean and i know its unfair to do it for a small country. the objective is to see if these time period is only for USA only

[…] Surviving the Next Downturn by A Wealth of Common Sense […]

[…] Reminder: I’ll be meeting with potential clients in NYC in a couple weeks (AWOCS) […]

[…] Also, I’ll be in NYC next week if any prospective clients are interested in going over this presentation […]