As discussed a couple weeks ago, it’s been over nine years since the Fed has raised interest rates. ZIRP has also now been in place since late-2008. Anyone who’s tried to earn interest in a money market fund, savings account or CD should understand the impact that these zero interest rate policies have had, as yields are basically non-existent.

The common argument from many commentators is that the Fed has been punishing savers these past few years with their policies. A recent article from Quartz made this exact same argument to show how difficult it’s been for investors to earn a risk free rate of return when compared with the past:

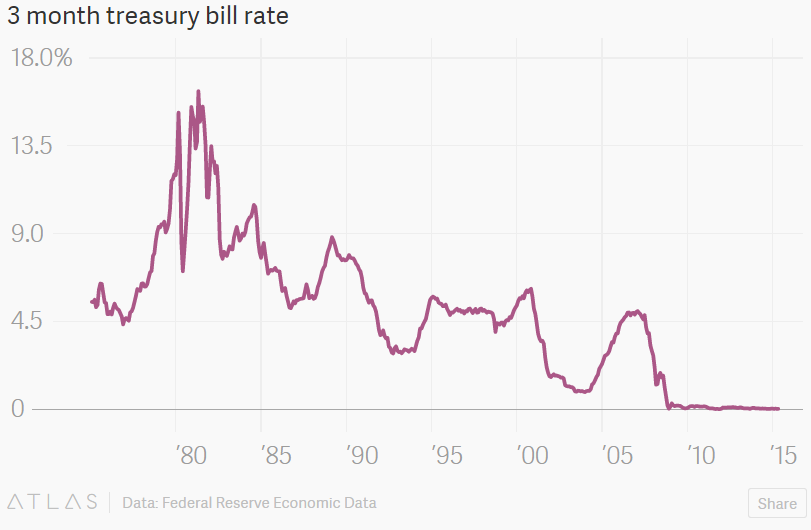

For decades savers could get both returns and safety. The figure below is the three month-treasury bill rate (which closely follows other liquid short-term rates) over the last 40 years:

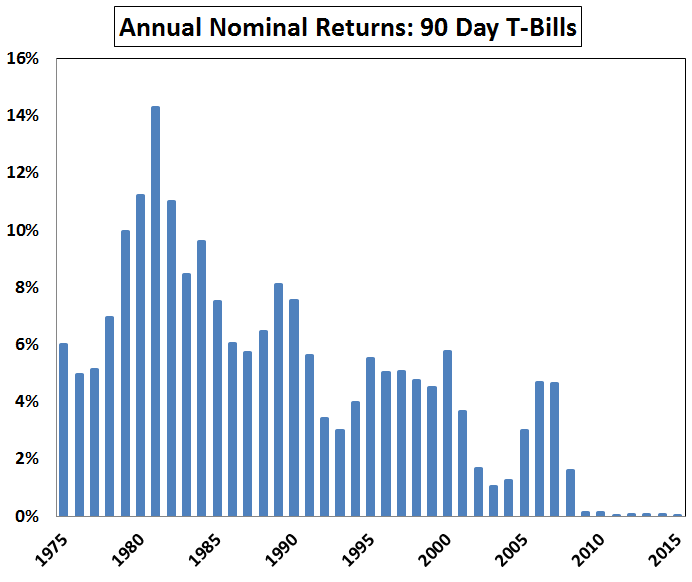

For the uninitiated, the 90 day t-bill is very short-term treasury debt that’s the industry standard for cash equivalents. The t-bill yield is a decent proxy for the interest rate you’ll earn on a savings account at a large bank. They’ve basically earned you nothing for each of the past five years. Here are the annual returns for t-bills going back 40 years, which you can see lines up nicely with the graph above showing the annual interest rates:

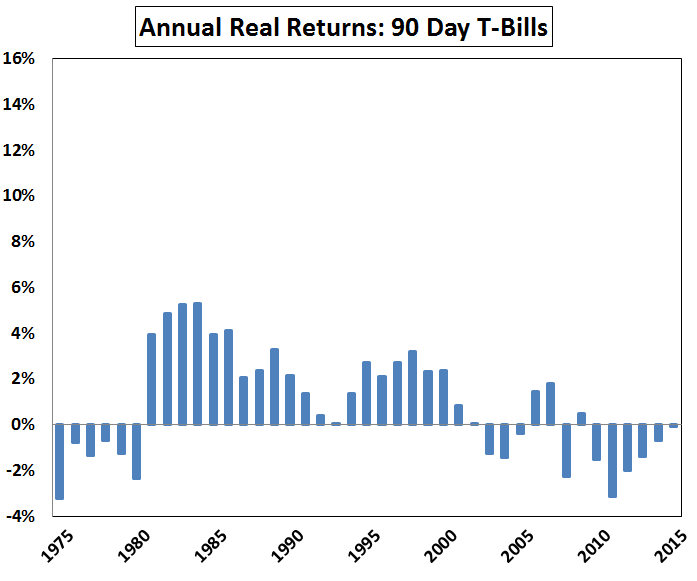

These “safe” returns look quite impressive before the recent financial crisis. In fact, from 1970 to 2007, t-bills returned 5.9% per years (go all the way back to the late 1920s and the annual cash return is closer to 3.5%). But, these are nominal returns. Investors should always think about real, after-inflation returns, especially when viewing an asset such as cash that will barely keep up with inflation over time. Here are the real returns on t-bills, taking into account the annual rate of inflation:

Not quite as impressive anymore. Over the entire period, after-inflation returns were just 0.8% per year. Real returns have been negative in recent years, which you would expect with near-0% yields and even a hint of inflation. But look at the late-1970s and early-1980s. Those too were negative on a real basis, even though interest rates were in the 5-10% range at the time.

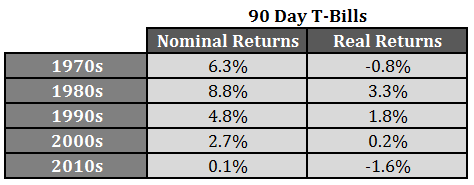

Now look at the returns by decade on both a nominal and real basis:

Things were better in the 80s and 90s, but it’s not nearly as bad as nominal rate differential would suggest. Savers have definitely been punished by the Fed to some degree as t-bills have seen negative real returns this decade (nominal returns are slightly positive at 0.3%/year). But it’s not nearly as much as some would have you believe.

It’s also worth noting that the S&P 500 is up nearly 17% per year over the past five years. Anyone who’s allocated even a small piece of their savings to the stock market has more than made up for any shortfall from their paltry savings account yields.

Source:

Why U.S. Savers Shouldn’t Get Too Excited About Higher Interest Rates (QZ)

[…] Fed has been hurting savers (@awealthofcs) […]

Bottom Line: Cash/Money Market Funds are not designed as an “investment” – cash is for emergencies, not for investment. Real Rate of Returns on Cash are zero… and when you factor in taxes, a Negative Real Rate of Return – ZIP.

I totally agree. I think of cash as an asset and not an investment. There’s a big difference between the two but now many people realize it.

Cash can be an investment when rates are what they are now. An alternative to fixed income allocation. With cash, you will lose to inflation today but with fixed income, you will lose principal…you will lose it forever in bond funds and bond ETF’s.

True, I know many investors who have switched to cash in their fixed income allocation for fear of rising rates. The problem is always when to make the switch back.

This reminds me somewhat of a comment a client made to me years ago when we were touting our above average performance in a falling market: “Terrific, but I can’t eat negative returns.” I suspect ordinary savers mostly ignore inflation and would view a 3.5% cash flow in hand favorably, even if the “real” value of these monies was negative. After all, you can “eat” a 3.5% return, but a 0.01% return not so much, even if the latter represents a higher real return.

Exactly. And things only get worse when you factor in taxes too.

I think it depends on what someone is saving *for*. If it’s just an emergency fund intended for daily expenses like food, gas, etc. in case of a layoff then yes, low inflation helps offset the low nominal return of the money in your savings.

But if you’re saving for a house, or college tuition, prices of those continue to climb 5-10% per year regardless of the CPI, making it pretty much impossible for what you’re saving to keep up unless you take on risk.

That’s true. Although you don’t earn much there are some ways to use an asset-liability match to try to earn something on those intermediate-term goals. A few I like are online savings accounts, CDs with early withdrawal penalties (so no interest rate risk) and even short-term bond funds, which could have some duration risk but not much.

[…] Just how badly has the Fed been punishing savers this decade. (awealthofcommonsense) […]

I wouldn’t be so quick to dismiss the cost to savers of negative real interest rates. By my calculations, it could be well over $1 trillion. And counting …

http://scottgrannis.blogspot.com/2014/07/the-1-trillion-tax-on-cash.html

Don’t you have to net this out with the trillions of dollars gained in the stock market? Also, savers were not restricted to money markets or t-bills. A simple FDIC-insured online savings account like Alley yields around 100 bps right now. That doesn’t make up the difference but it’s better than nothing.

[…] punished by a Fed to some grade as t-bills have seen disastrous genuine earnings this decade,” Carlson adds in his post, though “it’s not scarcely as most as some would have we […]

[…] punished by a Fed to some grade as t-bills have seen disastrous genuine earnings this decade,” Carlson adds in his post, though “it’s not scarcely as most as some would have we […]

What was the return on stocks when interest rates were 18%.? Another point that you’re missing out on is the return was guaranteed, the average American simply doesn’t trust the market,but they trust CD’s. This whole zero rate policy/money printing policy has sent our economy into one disastrous bubble after another. If you look at a stock chart from 1980 and match it up to an interest rate chart,it’s almost an exact inverse. That makes me believe that the returns are going to be much slimmer from this point forward.Maybe it’s time to give the public some confidence and raise rates,and maybe deflate a few bubbles in the process.

Actually the highest point on the interest rate graph turned out to be the greatest buying opportunity ever in stocks as it was the set-up for the 80s and 90s bull market. One of the reasons stocks were so cheap in the early 80s is because people thought high interest rates and inflation would continue. You could place all the blame on the Fed here, but they’ve had zero help in terms of fiscal policy from Congress. They’ve basically been on their own in trying to revive the economy. Higher rates would be nice for savers, but hopefully it happens because the economy is picking up steam.

[…] punished by a Fed to some grade as t-bills have seen disastrous genuine earnings this decade,” Carlson adds in his post, though “it’s not scarcely as most as some would have we […]

[…] punished by a Fed to some grade as t-bills have seen disastrous genuine earnings this decade,” Carlson adds in his post, though “it’s not scarcely as most as some would have we […]

[…] punished by a Fed to some grade as t-bills have seen disastrous genuine earnings this decade,” Carlson adds in his post, though “it’s not scarcely as most as some would have we […]

We can’t have a recession until we have an economic boom. The U.S. has not experienced that in over 15 years. I think the economy, within the next couple of years, will grow faster than it has since the ’80’s. With that, we will have inflation. With inflation, rates will rise higher and faster than anyone is predicting. We will get back to a decent 3 mo T bill rate within next couple of years…at lest 3%.

I recall being a teller during the summer of ’81…my college years. Arkansas S&L in North Little Rock, AR. Opening 5 year CD’s for around 14 or 15%. Amazing time back then.

That is the one thing that all the crash predictors fail to mention…we have yet to get a huge boom in the economy. It’s hard to imagine a crash (outside of a 1987 scenario) without excesses in the economy. Hasn’t come close to happening yet. I agree with you and actually think higher inflation rates in the coming years is a big possibility that most have completely written off.

I assume you have seen this:

http://www.marketwatch.com/story/here-are-the-staff-forecasts-that-the-fed-accidentally-leaked-2015-07-24?siteid=nwhpm

I am not in the least surprised. Typical gov’t.

Mark i strongly disagree with your growth forcast. The main driver of the U.S economy has been declining interest rates. these declining rates literally changed the way americans live. It’s been a boom for the stock market and housing.Refinancing has bought millions of cars ,payed of countless credit card bills, and have created the consumer culture that we live in today. So now that rates have bottomed the main driver is gone. That doesnt have to be the end of the world if the economy is growing,well 10 minutes before I’m writting this i read Janet Yellens interest rate /growth forcast for the U.S. The fed is expecting the economy to grow 1.74 % in the year 2020 (an appaling number). So put 1 and 1 together Stable interest rates and no growth (1.74%) = Slim pickings,and no inflation. As far as no recession till an economic boom ,well maybe this is the boom with 18 trillion of debt.? In 1981 i was was only 16, and I remember how cheap real estate was. there was inflation ,BUT CASH WAS KING ,everything was onsale.Now you borrow money cheaply To PAY TOO MUCH. Oh how I wish i could get a 15% CD now that I have money to invest.Sorry for Rambling on and on.

jp: Fist of all, the Fed has no clue what the economy will do next year or in 2020. And speaking of $18 trillion of debt, how do you think the gov’t will get that paid down? With inflated dollars. A new President along with a Republican congress will make it easier for corporate America and its citizens to prosper. Therefore, the economy will flourish, rates will move up, and inflation will increase.

No the exact opposite,you can’t pay the 18 trillion debt with those kinds of interest rates. Second ,can the fed create inflation ,yes ,but unfortunately they can’t always make the inflation be broad based or go where they want it. AKA BUBBLES. Well i guess we agree to disagree,but take my word for it a 7% mortgage is doomsday for this economy.,or a 6%CD to the stock market.? It’s Gary Shilling Vs Peter Schiff ,. CIAO

And you can’t make a dent in this huge debt with a strong dollar and little to no inflation. The gov’t needs cheaper dollars in the future to pay on its debt. My first mortgage loan in 1990 was around 9.5% – 10%. 7% rate on a mortgage loan would be just what the doctor ordered for paying down the federal debt.

[…] We’ve noted before that savers – at least the “in the bank” kinds – have been treated poorly in the low interest rate environment. Ben Carlson at a Wealth of Common Sense picks up the torch with some hard numbers. […]

[…] on savings have been “basically non-existent” since 2010, financial blogger Ben Carlson wrote in July. While the nominal return on 90-day Treasury bills has been around 0.3 percent, Carlson pointed out […]

[…] yields on savings have been “basically non-existent” since 2010, financial blogger Ben Carlson wrote in July. While the nominal return on 90-day Treasury bills has been around 0.3 percent, Carlson pointed out […]