“The biggest factor impacting investors is no longer our knowledge base, but rather our behavioral elements.” – Barry Ritholtz

There are many factors that we can look at when trying to figure out why the stock market went up or down on any given day.

We can search the economic data for clues. We can also look at what’s happening with different industries and sectors, the level of interest rates, currency fluctuations and what the Federal Reserve is saying and doing.

But when you really narrow it down, the future returns on stocks come from the collective earnings growth of the companies in the market, the dividend yield and the changes in valuations (how much investors are willing to pay for earnings or the P/E ratio).

DIVIDENDS

Dividends for the entire market are actually fairly stable over time. Here are the average annual dividend yields for the S&P 500 by decade going back to the 1960s:

You can see that yields have been on the decline over the past 50 years or so but they haven’t changed drastically.

And most of this decline can be attributed to the fact that companies are now more inclined to repurchase their own shares instead of paying out dividends. At the end of the day this works out as a return to the shareholder, which is a positive for your returns.

So the dividend portion of returns is fairly easy to estimate.

EARNINGS GROWTH

Earnings growth is also fairly stable over time. Take a look at this graph from Vitaliy Katsenelson and you can see that earnings growth pretty closely tracks nominal GDP growth over the long-term:

That makes sense since GDP is simply the market value of all good and services produced within a country. So company earnings more or less track the growth of the economy.

And here is another graph from Katsenelson that shows earnings growth, GDP growth and stock returns by decade going back to the 1930s:

You can see that both earnings growth (EPS) and GDP growth have been fairly stable, yet the returns of the S&P 500 vary greatly. The reason for this divergence is where the valuation part of the equation comes in.

CHANGES IN VALUATIONS (EMOTIONS)

In fact, Vanguard recently released a report stating that the most important factor for predicting future stock returns over the past 86 years has been valuation.

To any casual observer this makes perfect, logical sense. The less you pay for stock earnings (or the lower your P/E multiple) the better your future performance should be. So they basically informed us that it makes sense to buy low when stocks are cheap.

Sounds simple enough but it’s obviously not that easy to put into practice. That’s because the real driver of the valuation piece in stock returns is our emotions. Morgan Housel of the Motley Fool recently had this to say on the subject of valuation:

“Earnings multiples reflect people’s feelings about the future. And there’s just no way to know what people are going to think about the future in the future. How could you?

If someone said, “I think most people will be in a 10% better mood in the year 2023,” we’d call them delusional. When someone does the same thing by projecting 10-year market returns, we call them analysts.”

According to a recent study, most assets only trade at “fair value” about 30% of the time. So the rest of the time they are simply fluctuating between being overvalued and undervalued, depending on current market sentiment.

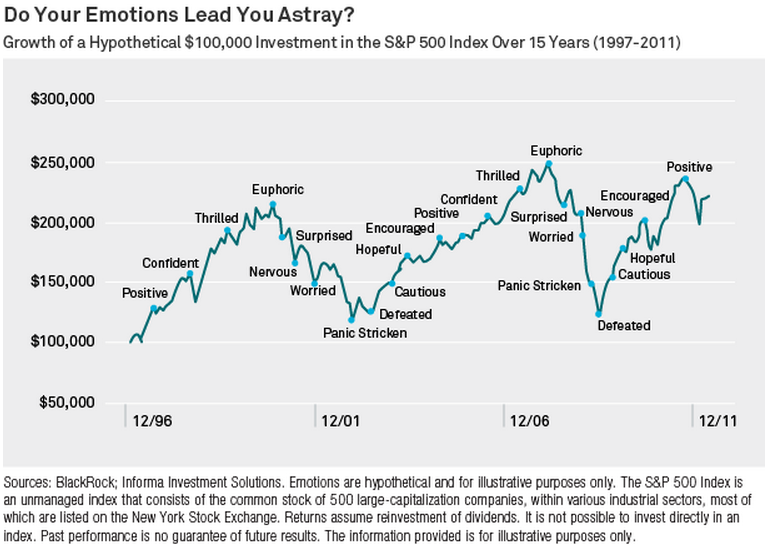

Here is a great graph from BlackRock that depicts the emotional ride that investors went on over the 15 year period from 1997-2011 as stocks went up and down :

FOCUS ON THE LONG-TERM

Accepting that you have no control over the behavior of the crowd is the first step in keeping valuation from making you lose your long-term focus. This is especially true in shorter time frames.

Since valuation depends on how investors are feeling about the market at that particular moment in time and emotions cause those feelings to change at the flip of switch, you need to figure out a way to take advantage of the swings in sentiment and valuation.

Unfortunately, like a pendulum, markets tend to swing from side to side (overvalued to undervalued) and usually overshoot in both directions depending on the mood of the participants or Mr. Market.

That is why setting the correct asset allocation for your risk profile and time horizon is so important. Asset allocation is worthless if you are unable to use it to your advantage through diversification and rebalancing.

This allows you to benefit in those times that the market becomes overvalued by selling to take some profits and also when the market becomes undervalued by buying when stocks become cheap.

You must also be honest with yourself about the amount of stock market exposure you are willing and able to accept in your portfolio. If you can’t handle the wild swings in price or the fact that stocks will go down periodically then you need to reassess how stocks fit into your portfolio.

Stock movements are the usual suspect that cause us to change our plans at the absolute worst times.

Over the long-term stocks will reflect the dividend yield, earnings growth and long-term average multiple investors are willing to pay for those earnings and dividends.

In the short-term, who knows how the market will react? That’s why Benjamin Graham said the in the short run the market behaves like a voting machine, but in the long run it acts like a weighing machine.

Try not to get caught up in valuation extremes. Make a plan, automate good behavior and stick with it over the long term. Be content to earn your dividends and enjoy the earnings growth of the stock market and don’t try to make sense of changes in the market’s valuation.

Sources:

Are We There Yet?

If You Only Know Five Things About Investing, Make It These

The Little Book of Sideways Markets

The Emotional Investing Roller Coaster

NYU

The Little Book That Still Saves Your Assets

[widgets_on_pages]