“Sixty/40 is anchored in a really important existential point—the benefit of diversification. So, to say that 60/40 is dead is basically to say that diversification is dead—at least as far as it goes between stocks and bonds.” – Nicholas Colas

The 60/40 stock/bond portfolio is often used as a simple benchmark for a balanced asset allocation. Historically, this portfolio mix has been shown to offer solid returns with a nice risk profile over the long-term.

You could do much worse than a 60/40 portfolio as a base case scenario for a moderately conservative investment strategy.

Obviously, personal circumstances have to be taken into account, but it makes sense as a good starting point for those near retirement age or looking for a balance between growth and income.

Not everyone is a huge fan of the 60/40 mix.

Brett Arends of MarketWatch had this to say last year on the 60/40 portfolio:

Chances are, when you cut through the jargon and the spin, they’re all based on one big assumption: that a balanced portfolio of stocks and bonds, rebalanced regularly, will see you through whatever comes next.

Here’s the ugly truth. Contrary to what you are being told, this 60/40 portfolio of stocks and bonds comes with no guarantees. There have been long periods during which it has done very badly.*

He is right, up to a point.

Financial markets make no guarantees to anyone, especially in the short to intermediate term. No strategy is so infallible that it works at all times.

But this has always been the case.

You earn returns on risky assets over the long run because they occasionally go through long stretches of poor performance. You get your rewards by taking your risk, which is as it should be.

The old school 60/40 portfolio of U.S. stocks and bonds could have an uphill climb over the next decade or so. You could make the case that based on lower interest rates and higher stock prices that future performance could be lower than it’s been in the past. Who knows.

Yet Arends doesn’t mention the fact that investors now have access to a broader set of investment choices these days than we’ve had in the past.

You can create a highly diversified global portfolio in a number of different asset classes and sub-strategies with only a handful of low-cost funds.

In fact, I would argue that investors should be looking to allocate their portfolios much more globally these days to increase the benefits of diversification.

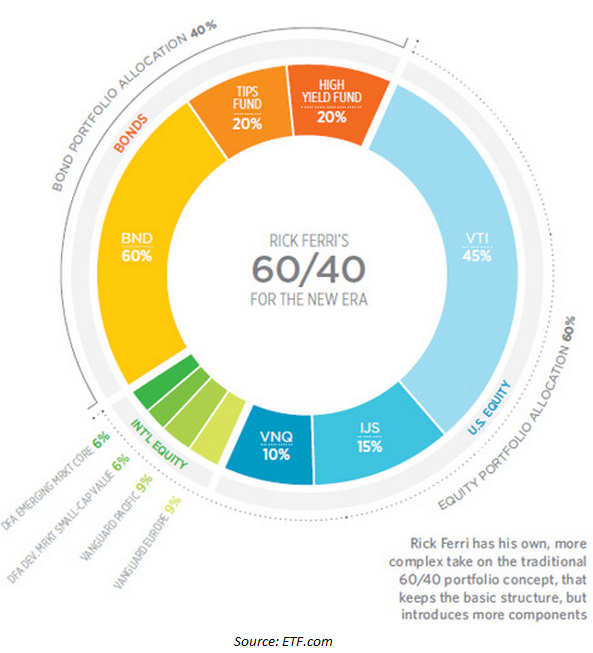

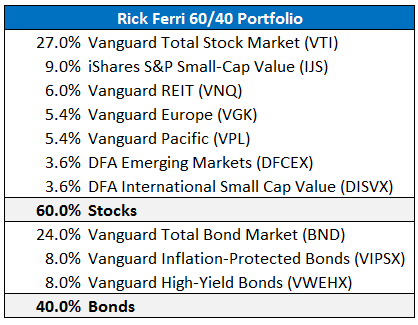

Rick Ferri of Portfolio Solutions shared his take on a globally diversified 60/40 portfolio in a recent interview with ETF.com. Here’s what Ferri came up with:

Ferri’s portfolio mix still uses the basic 60/40 stock/bond weighting but breaks down each asset class even further by including value stocks, mid-caps, small-caps, REITs, international developed markets, emerging markets, TIPS and high yield bonds.

Here’s a further breakdown of this portfolio including the various fund tickers:

I ran the numbers on this portfolio and compared them to the old school 60/40 mix of the S&P 500 ETF (SPY) and Vanguard Total Bond ETF (BND) from 2002-2013.**

Assuming an annual rebalance, the old school 60/40 portfolio returned a respectable 6.2% per year. Not bad.

But by making the portfolio more global and adding in the sub-asset classes, the Rick Ferri 60/40 portfolio returned 8.1% annually over the same time frame. Even better.

This is just one period so I wanted to see how the portfolio held up in different environments.

I used my favorite new backtest website, Portfolio Visualizer, to go back even further with this analysis using the indexes for these asset classes (since many of the funds haven’t been around long enough).

This analysis went back to 1985. I looked at the 15-year annual returns on the strategy at the end of each year. The average 15-year annualized return was 9.4% (the median was 9.6%) with a high of 13.2% and a low of 7.3%.

All the usual caveats of past performance apply here. Most long-term diversified asset allocation strategies look great on paper or in a backtested simulation.

It also helps that most of these returns occurred during the go-go years of the 80s and 90s when stocks and bonds both had excellent performance.

I think is the point Arends was trying to make. The old school 60/40 portfolio had a nice tailwind past decades, but may be facing a headwind from here (again, we’ll see what happens).

Yet even if you look at the 15 year stretch from 1993-2008 which includes the emerging markets crisis of 1997-98, the tech bust in 2000 and the financial crisis of 2007-08 you would still get returns of 7.3% per year in Ferri’s portfolio.

That’s pretty good considering U.S. stocks had two separate losses in excess of 50% during that time.

Here’s Ferri’s take explaining the 60/40 portfolio:

“Sixty-40 is sort of like Adam Smith’s ‘Invisible Hand,’” Ferri said. “We don’t know exactly why it works, it just always seems to work. In the end, when you look back over a 15-year period of time, it works.”

Notice the time horizon Ferri references here — 15 years. That’s an important distinction from saying the next few years could see lower than average performance.

These types of strategies generally work if you are patient and let them work by staying with your plan, rebalancing and ignoring the short-term noise of the cyclical nature of the markets.

Diversification is still the most consistent way to extract value from the financial markets over the long run.

Sources:

‘60/40’ Portfolio Down But Not Out (ETF.com)

Why a balanced portfolio may not work (MarketWatch)

Further Reading:

Rick Ferri’s aha moment (Vanguard)

*Arends offers a portfolio of 20% stocks, 30% long-term treasuries, 30% TIPS and 20% commodities as an alternative. I’ll try to look more closely at this asset allocation in the future but my first impression is that it’s extremely light on stocks. It also closely resembles a risk parity approach which doesn’t perform all that well when interest rates rise, as they are expected to do in the coming years.

**Many of these ETFs started 2002, but a few of didn’t go back quite as far so I had to use the corresponding mutual funds to fill in the blanks.

What would be very helpful would be a graph of yearly returns over the last 15 years. The comparison of volatility would be both instructive and indicate potential investor tolerance for the approach.

Going back to 1985 the st dev of the Rick Ferri portfolio was 11.6% (vs. 11.3% for the old school version). Here are the annual returns starting with ’85: 29.9. 24.3, 5.9, 17.8, 18.3, -5.7, 26.1, 8.0, 18.7, 0.5, 20.2, 12.9, 14.7, 9.1, 16.5, 0.6, -1.5, -5.4, 25.2, 13.9, 7.6, 14.2, 5.3, -23.6, 23.5, 14.3, 1.0, 13.0, 14.1.

Remember this is for illustrative purposes only. This says nothing about the future.

What would be even more instructive would be a graph of yearly returns for the last 15 years. That view of volatility would help indicate potential investor tolerance. Averages are nice in theory but real volatility affects people nonetheless. Thanks.

That is true. I have those numbers, but just need to run the analysis.

I do agree with you that volatility affects people’s behavior. I think the beauty of a long-term analysis like this is that short-term volatility shouldn’t be the main focus of the investor…it’s the long-term results that matter. Of course, that doesn’t help much when you see a larger, drawdown but investors must realize that volatility can used to their advantage, not something to necessarily be afraid of.

But yes, I will run an update with the annual numbers and some useful stats as well.

Ben,

Enjoyed the article. I agree, the much-maligned 60/40 portfolio is a very good default allocation for most investors, with younger folks or those with long time horizons looking to maximize returns might go 80/20 or 100/0, and those without any legacy aspirations or with minimal withdrawal needs and a serious aversion to volatility might go 40/60.

In my opinion, though, you cannot write an article about 60/40 portfolios without mentioning the “DFA Normal Balanced Strategy”, which has been around in some form for 20+ years in DFA’s yearly Matrix Books (almost completely unchanged). As a matter of fact, the simple but excellent book “The Investment Answer” used various risk/return versions of this portfolio (from 100/0 to 0/100) as allocation examples throughout the book.

The true merit of this approach, IMO, is that it targets risk and expected return the RIGHT way – moderate tilts to small cap and value stocks globally on the equity side so one need not take much risk in fixed income, where returns are hard to come by over a full interest rate cycle from either credit or term risk. If you think about it – this is the entire rationale for holding a “balanced” 60/40 allocation: part of the mix provides in good times, the other part when times are not so good (economy stalling, credit spreads widening, interest rates/inflation risk risking, etc.).

Indeed, despite a bond bull run for the ages from 2002-2013 (which disproportionately benefited longer-term bonds and TIPS as well as junk bonds and held back portfolios with short-term bonds), the Normal Balanced Strategy still bested the ETF mix above with less volatility and downside risk — the ‘keep it safe’ bond portion of the allocation more than absorbed the greater risk/volatility stemming from increased small and value exposure.

Of course, if we learned anything from recent markets, it’s that if you are using bonds as a portfolio ballast (as you should), unless you are 100% nominal treasuries (inadvisable), then you want to stay short term and high quality. As you know, a component of dependability and liquidity is something even the “smart money” institutional investors failed to account for. Same here: Vanguard TIPS actually lost -2% in 2008, and Vanguard High Yield lost -21%. In the later case, you’d obviously be better off just buying stocks where expected returns are higher if you are taking those kind of risks. The bond component of the DFA blend above in 2008? +5%. You can bet that kept more than a few people from bailing on the 60% of their portfolio that was tanking, and maybe even rebalancing.

Keep up the good work!

Eric

Eric, thanks for the comment. I’ve read a number of your pieces and appreciate your long-term thought process.

I’m unfamiliar with the DFA Normal Balanced Strategy you mentioned, but I will be sure to look into The Investment Answer. Sounds interesting.

I do agree with you that a small cap and value tilt makes the most sense for long-term investors. I actually think that mid cap value is on of the most underutilized and forgotten asset classes of them all.

Also agree with your assessment on fixed income. Take your risks with equities and use fixed income as your anchor. No reason to reach for yield/duration in your low risk bucket and get unwanted volatility. I think the barbaell approach of taking lots of risk in stocks and little risk in bonds is the way to go. No need to get stuck in the middle where most investors get into trouble.

HY should probably be considered part of the equity allocation considering the risk profile. I look at HY as being similar to convertibles. A hybrid investment with an income element but with equity-like risks.

I really wish DFA would make their product available to the general public, but I understand why they go through advisors (and obviously the strategy is working for them).

Thanks again for stopping by. You’ve given me some interesting ideas to look into.

You bet Ben, thanks for the thoughts.

I don’t think there is a one-size fits all allocation, even at a given stock/bond split such as 60/40. That being said, basic principles such as “take your risk in stocks” while “keeping bonds safe” work for a variety of different investors be they individual or institutional. Of course, during the unpredictable and short periods when bond risk is “working” (as interest rates decline or credit spreads contract), this approach feels stodgy and outdated. Until it doesn’t, as the long-term evidence shows.

There’s no magic to the DFA portfolio I referenced above, it’s just been around for a while so it’s become sort of a standard. Most of the asset classes are available from Vanguard or in ETF form over shorter periods of time, so someone who reads “The Investment Answer” and decides to go it alone can get reasonably close. It’s the doing it/staying the course why the advisor may be needed (along with coordinating investments with other aspects of the wealth picture), not the access to DFA funds.

On Mid Cap Value – the last 10 years have been good to the middle of the market, and the watered down nature of retail large value and small value indexes do make it look a bit better by comparison. But longer term, it appears as though mid value does about what we’d expect: smack dab in between large and small value. Going back to 1986 (inception of Russell Mid Value Index), we see the DFA US Large Value Index returned +11.7%, the Russell Mid Value Index did +12.3%, and the DFA US Small Value Index produced +14.2%. Actually a bit disappointing for mid cap if you were expecting it to literally be 50% between large and small (+12.9%). And one other reason to stick with a large/small barbell – there is a diversification bonus when you rebalance the two annually. Per above, the annually refreshed mix of DFA US Large Value and US Small Value Indexes actually earned +13.1%, for an extra 0.2% per year.

Eric

Right, nothing special about the DFA style of investing except you need to see it through the peaks and valleys for it to work the way it’s supposed to.

Time frame matters, of course, but I found that the S&P mid-value has outperformed the S&P small value index by almost 1% since the small index was instituted in 1994.

Although I’m sure certain value indices are calculated differently than others. Either way, like you said, the benefits come from periodically rebalancing the more volatile small/mid stocks to take advantage of the fluctuations.

[…] 60/40 works, but even more diversification works better. (A Wealth of Common Sense) […]

All of you folks torturing the historical data should be able to hear it “confessing” the desired truth as a scream every time you run one of those “analyses”. But the unfortunately problem with all such backtests is that the future may not look like the past.

The biggest swing factor has been the 30 year interest rate and inflation cycle falling, plus a massive expansion of equity market P/E ratios at the same time (I won’t assume causality here, but they are likely to be related).

If you want to take this data torturing to its logical extreme, have a look at all of the so-called “risk parity” approaches being pushed around the market, especially with tags attached saying “forecast free returns!”. Except of course that they context of falling interest rates boosting bond returns is relegated to the fine print.

My point is a simple one: without an explicit focus on investor objectives, no advisor can possible say that a 60/40 fund, old style or new, OR ANY OTHER TYPE OF PORTFOLIO ALLOCATION for that matter, is appropriate for their clients. And discussions about “well Fund X is better than Fund Y” are most often without context and therefore without meaning too.

You’re right, but if you would have bothered to read the entire post you would have seen that I made all of the same points you just made. Obviously you need to take into account your own risk profile and time horizon.

Of course the future will be different from the past because it’s always different. Investors must learn about the history of financial market returns to understand how different long-term and short-term cycles work. Markets are always and forever cyclical, but if you have a long-term perspective you will likely do much better than most.

The point is that since the future will be different, being even more diversified will help so you aren’t beholden to treasury interest rates or S&P 500 PE multiple expansion.

Cranky,

As best I can tell, I agree with your points insofar as the last 30 years (since 1982) of DECLINING interest rates has resulted in asset class returns (esp. long-term bonds) that are not at all possible going forward. And, of course, we are ignoring how we got to those really high rates in the early 1980s – through an unprecedented period of high inflation and RISING rates.

However, I just think we come to different conclusions. I don’t throw out history because I think the future will be different, I use the longest data possible to include these different periods for stress testing purposes. For example, lets look at the asset class data for the period from 1973-1981.

Inflation = 9.2% (!)

S&P 500 = +5.2% (-4.0% real)

Long-Term Corporate Bonds = +2.5% (-6.7% real)

“All-Stock Balanced Strategy” = +13.0% (+3.8% real)

“Normal Balanced Strategy (60/40)” = 11.1% (+1.9% real)

S&P 500/Aggregate Bond (60/40) = +5.6% (-3.6% real)

So if we ignore the last 30 years of falling rates and multiple expansion, instead focusing on a painful period of rising rates and inflation, we see that traditional large growth-oriented stocks (S&P 500) did poorly, long-term bonds did poorly, and traditional S&P 500/Aggregate Bond 60/40 mixes did poorly. The risk parity approach you mention would have been taken out back behind the woodshed and put out of its misery very quickly (can you imagine borrowing money at 10% to leverage up long-term bonds whose principal value was falling?). So I agree here, risk-parity approaches are short-term data mining exercises at their worst.

No, the best defense would have been an all-stock allocation with global diversification and liberal amounts of small cap and value exposure (see “All-Stock Balanced Strategy”). But if you had to add bonds, sticking to high-quality, short-term (5 years or less) would be the way to go, as evidenced by the “Normal Balanced Strategy”, that managed a 2% per year real return…no small feat in the face of 9% per year + inflation.

Gold, by the way, from 1975-1981 (first year it was legal to own it) earned +11.6% (2.8% real) – less than the globally diversified all-stock asset class index and only marginally better than the 60/40 version with much greater risk (and a 20 year period that followed with -50% real returns).

The lesson? Don’t throw out history, just don’t cherry pick the periods you like to prove a point. A mistake, I believe, a lot of investors are making when they hold large growth-oriented stock portfolios coupled with excessively risky bond allocations to juice yield. Sure, the expense ratios maybe low, but you’re picking up pennies in front of a steam roller.

Eric

FWIW,

Anyone who wants to study the really long-term behavior of global asset classes and diversified portfolios should give this tomb a look:

http://www.ifaarchive.com/pdf/dfa/matrix_book_us_2013.pdf

The diversified portfolios (including the 60/40 “Normal Balanced Strategy”) begin on page 37.

Eric

Great resource. Thanks for sharing Eric.

You’re also right to point out the 70s period (50s & 60s weren’t great either) of terrible real bond returns. This is why you need to be a historian as an investor. Not many people have experienced a bond market where rates weren’t falling. Should be interesting going forward, as always.

[…] Enhancing the 60/40 portfolio – A Wealth of Common Sense […]

[…] received a decent amount of comments and questions on my recent post on the 60/40 portfolio. Some were constructive, but others missed the point so I thought I would take the time to clarify […]

If anyone is interested, here is a link to latest version of matrix book:

http://www.robasciotti.com/docs_information/The%20Matrix%20Book%202014.pdf

This is great. Thanks for the info.

[…] Reading: The Rick Ferri 60/40 Portfolio Back-Testing the Tony Robbins All-Weather Portfolio Looking Beyond Interest Rate Risk in […]

This is really good analysis . . . and interesting Ben. I’ve been using that same tool and have wondered about how to think about “risk adjusted return” (a phrase I hear C. Roche use a lot). Using assets classes in Portfolio Visualizer I see that a 60/40 (large cap growth/total bond) since 1972 has a CAGR of 9.33% with a standard deviation of 12.97%. Compare that to the same asset classes distributed 15/85 and you see a CAGR of 8.14% and std deviation of 6.8%.

So how do we talk about that? Is it fair to say that one gives up 1.19% on the average annual return while taking on less than half the volatility?

That’s interesting. That also shows how strong the bond bull market has been over the past 30+ years. Bonds have been an risk-adjusted asset class in that time. Hard to believe investors will have the same luck going forward. See here:

https://awealthofcommonsense.com/back-testing-tony-robbins-weather-portfolio/

[…] An blog post on the 60/40 portfolio […]

This allocation appears to mimic the Wellington Fund composition.

Interesting. I hadn’t looked into that before. I’ll take a look.

[…] 3. The Rick Ferri 60/40 Portfolio, Ben Carlson, A Wealth of Common Sense […]