Stock valuations are getting into potentially overvalued territory. Bond yields — from government to high yield to corporates — have all fallen precipitously since the financial crisis. Real estate, venture capital and private equity are also likely reaching above average valuation levels.

It’s tough for investors to know what to do in this situation.

Zero Hedge posted an interview conducted by Goldman Sachs with Nobel-prize winning economist Robert Shiller yesterday. You can just tell the end-of-the-world blogger loved highlighting the following passage:

This time around, bonds and, increasingly, real estate also look overvalued. This is different from other over-valuation periods such as 1929, when the stock market was very overvalued, but the bond and housing markets for the most part weren’t. It’s an interesting phenomenon.

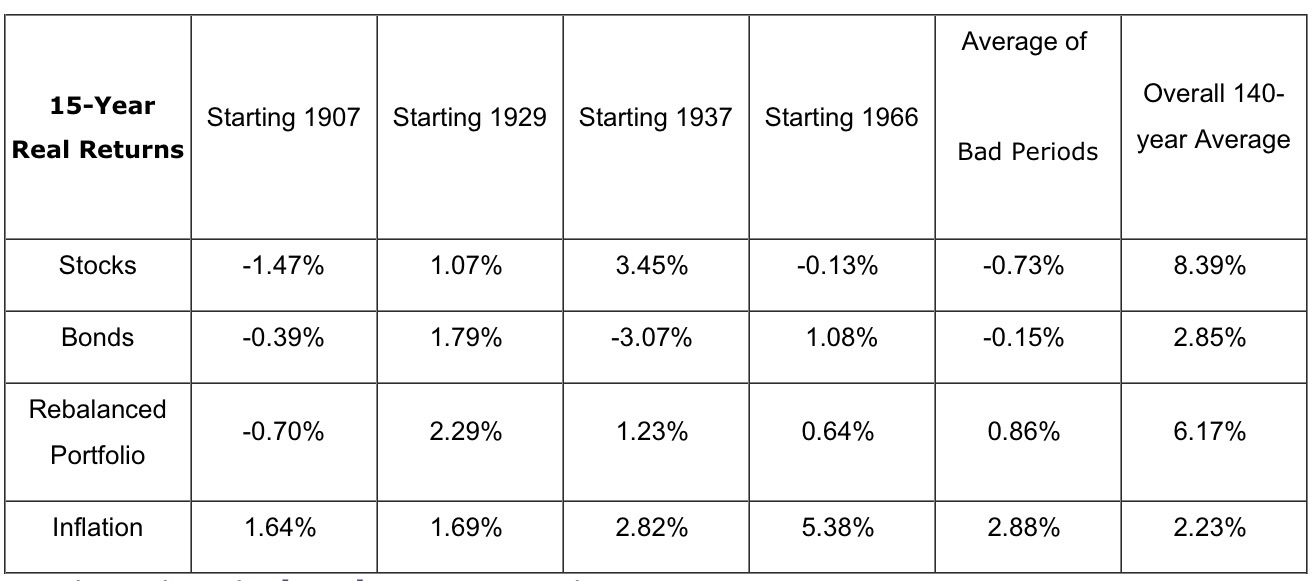

In thinking about the possibility of poor stock and bond performance from these valuation and interest rate levels, it’s worth putting some historical context around this debate even if the past is not prologue. Michael Kitces re-posted some timely data from his blog yesterday outlining the worst case scenario:

Each of these periods align with a catastrophic economic outcome. The Panic of 1907 was a severe depression which saw economic output fall by a third. JP Morgan had to more or less singlehandedly save the entire banking system that year. 1929 marked the start of the Great Depression. 1937 was among the worst recessions of the 20th century as GDP dropped by one fifth. Also, these are after-inflation returns. Even in the 1966 scenario the nominal returns were decent. It was sky high inflation from a commodity price shock at the time that makes the real returns so much worse.

There’s a huge difference between above average price-to-earnings multiples and economic calamities. Elevated profit margins, high CAPE ratios, high margin debt and historically low interest rates are not the same thing as an economic depression. This is not to say that we can’t see a crash or much lower than average returns from these levels, but more times than not these events are triggered by enormous excesses in the economy, not some valuation model.

And remember, bonds can be held to maturity. In a way it’s difficult for the bond market to be overvalued in the same sense as the stock market can be. Fixed income investors have to worry about default and credit risk, but really the biggest risk for high quality bonds is inflation, not an outright crash. Long-term bond market performance is much easier to estimate than the stock market by using the starting yield levels, but this has always been the case. It’s just that with rates so low now there’s not as much of a cushion if inflation picks up in the future, so volatilty will likely be higher than normal in bonds.

It’s also very difficult to say that “everything” is overvalued since investors have to put their money somewhere. There’s no such thing as an equilibrium level that the system gets reset to all at once. You have to consider relatives as well as absolutes in this case. Since most people these days only read the scary headline, many probably missed the fact that Shiller also said the following in his interview (emphasis mine this time):

And as a general principle, I think people should diversify across assets and geographies because there is no way to predict what any one asset will do with any accuracy. I’ve been talking down US stocks because of their high valuation, but I would invest something into US stocks; I would just put a heavier contribution in stocks around the world, where CAPE ratios look lower. I keep coming back to the theme that there are lots of places outside of the US to invest. And I would also own bonds, real estate and commodities.

I’ve probably spent far too much time writing on this subject lately, but I think it’s an important one to think about considering there’s a deluge of prognosticators making some fairly dire predictions. To say that everything is overvalued has more to do with expectations than anything. Investors should expect periods of below average performance to follow periods of above average performance. This is how mean reversion works. But trying to predict a crash, an economic shock or exactly what future stock market returns will be is much harder than it looks or sounds in theory.

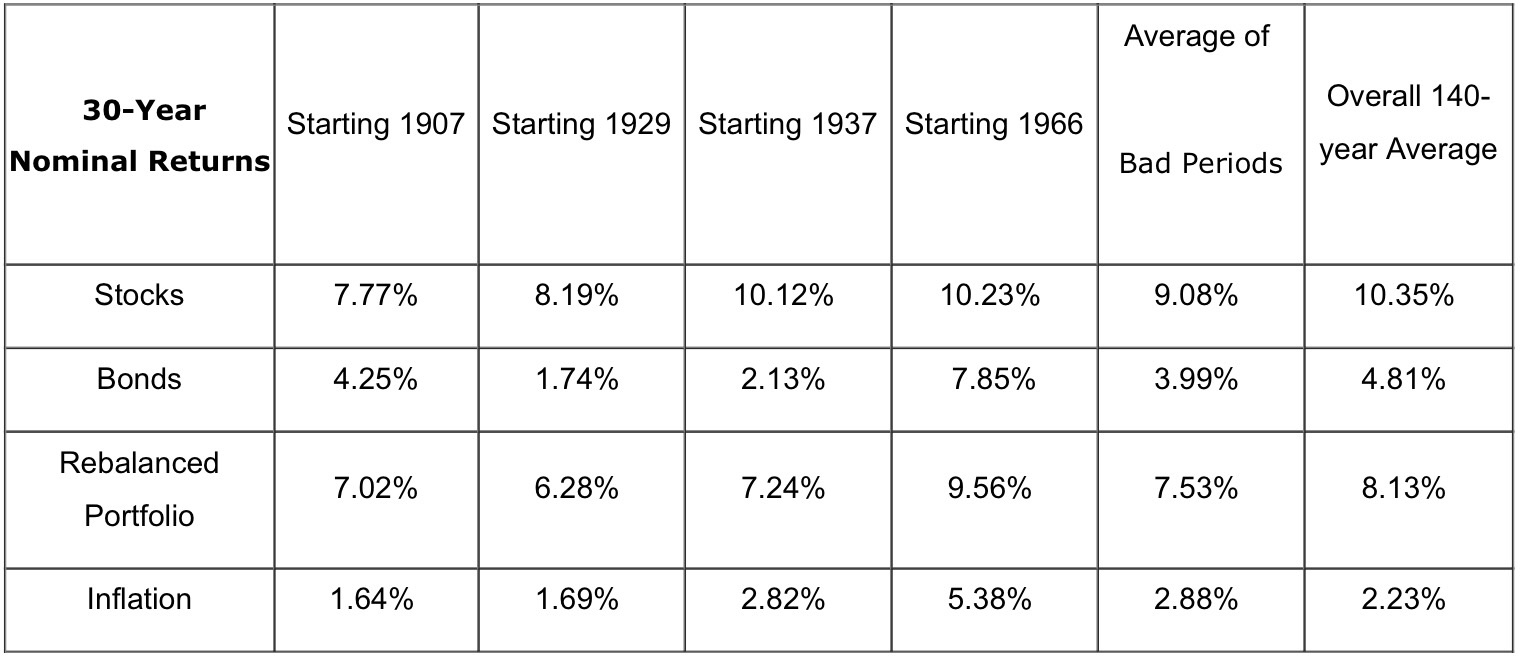

To end things on a more positive note, check out the 30 year return numbers from the same starting points as those dreadful 15 year returns from above (note that these are nominal, not real, returns this time):

Not bad.

Further Reading:

What Does the Bursting of a Bond Bubble Look Like?

Market Returns During Ray Dalio’s 1937 Scenario

What’s the Worst 10 Year Returns from a 50/50 Stock/Bond Portfolio?

Sources:

Robert Shiller: Unlike 1929 This Time Everything – Stocks, Bonds And Housing – Is Overvalued (Zero Hedge)

What Returns Are Safe Withdrawal Rates REALLY based upon? (Nerd’s Eye View)

Ben,

I don’t think you spend too much time writing about this. You can never spend too much time on the fundamentals: have realistic concepts about returns, stay disciplined, and stay diversified.

Thanks for all your articles.

KG

Thank you. I think it helps to hear the basic principles over and over again (for myself as well).

[…] Finally, say you put your only $10,000 to work today and it actually is the exact top? How would you do? According to Ben Carlson who ran the numbers on all the past worst times to invest…not so bad. […]

It is funny that a lot of „experts” predict the exact future returns of the

stock markets referring to the CAPE but Shiller who created it refrain from

any numbers and he is not sure about the direction of the market. This is a difference between proclaimed experts and a wise man.

Of course I don’t refer to Ben as a proclaimed “expert”. He is a wise man too:)

Yup, Shiller is much more nuanced than people give him credit for if you’re just reading the headlines. Here’s some more numbers on CAPE to show you how wide the range of results can be even from elevated levels:

https://awealthofcommonsense.com/cape-ratio-range-historical-outcomes/

I am a regular reader of Your blog (it is in my bookmarks) but missed this article. Thanks Ben! Meb’s book is great I read it.

By the way did You know this site? http://www.starcapital.de/research/stockmarketvaluation

15 years:):

http://www.starcapital.de/research/CAPE_Stock_Market_Expectations

Whenever I see something from a “Professor” discusses investing and the financial markets, an automatic B.S. Siren goes off… as it should…

If you are an investor, you do not worry so much about “Valuations”… When you rent your investments (trading in and out, attempting to time the markets – which is what it is… renting) then I guess valuations might matter (short-term).

The Bond Market is in for some tough years (or a decade)… That is an easy call – when??? Nobody knows…

The when is definitely the tricky part as anyone who’s been screaming about valuations for the past four years can attest to.

Along the same thought, my ear canals close when I see an “economist” quoted. And if I happen to listen on rare occasion, my thought is always that if I took any action based on the economist’s opinion, it would be to take advantage of the opposite outcome.

Yes, and the problem is after all of the economic issues in 2007-09 people assumed economists could help them invest better, which hasn’t worked out too well.

[…] How to deal with overvalued markets. (awealthofcommonsense) […]

[…] asset preservation came from Nobel-prize winning Robert Shiller over the weekend. As pointed out by A Wealth of Common Sense blogger Ben Carlson, one core piece of that advice was diversification. “As a general principle, I think people […]

[…] What If Everything Is Overvalued? A Wealth of Common Sense […]

I beg to differ, Steve. When you’re an investor, you worry always about valuations. The 15-yr annualized return for the S&P 500 Index, including dividends, is less than 5%. You started with a Shiller PE over 40. It was fairly predictable. And that, after a massive 6-yr bull run thanks at least in part to unprecedented Fed stimulus. And you still couldn’t manage 5% in the index.

If you want to go to 30 years to make it look good, that’s fine. But retirees don’t always have 30 years. They only do (in some cases) at the very beginning of retirement.

Shiller PE and Tobin’s Q aren’t perfect. Yes, it’s possible to start at a high valuation and do well for the next 10 or 15 years, but the odds aren’t on your side. And investors should know that. It may mean that an investor doesn’t change his or her allocation in response to that at all. And that’s fine, but preparing investors psychologically and setting their expectations is important. Lying to them isn’t a good strategy.

It’s often said that people should say “I don’t know” more. I’m generally in favor of that. But we do know some things. We’re not totally in the dark about valuation and what it might mean for the next 10 or 15 years. We don’t know exactly, but we know probabilistically. And that’s not nothing.

If investing can be boiled down to one thing, it’s valuation. It’s always about valuation. How much are you paying, and how much are you likely to get given the starting valuation. Never a perfect answer, but I don’t see the validity of putting your head in the sand either.

[…] What If Everything Is Overvalued? – A Wealth of Common Sense […]

[…] What if everything is overvalued? – AWOCS […]

[…] What if all the things is overvalued? – AWOCS […]