“Beware of geeks bearing formulas.” – Warren Buffett

Research Affiliates puts out some of the most interesting and thought-provoking research in the investment industry. Founder Rob Arnott’s work on fundamental indexing is especially innovative.

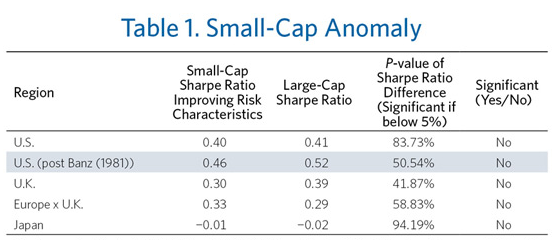

The firm’s latest piece looks at smart beta and a host of factor investing data. One factor they looked into was the small cap anomaly. Past research has shown that small cap stocks have outperformed large cap stocks over longer time frames. Research Affiliates determined that this actually isn’t the case:

Using the Sharpe Ratio they showed that on a risk-adjusted basis there was no small cap anomaly. The research used here is interesting for data junkies, but it’s tough to say if it’s useful for investors when creating a portfolio.

It also begs the question about whether or not the Sharpe Ratio really makes sense as a way to gauge investment performance. More to the point — do risk-adjusted returns matter? Or should they matter to investors?

The Sharpe Ratio is a formula created by William Sharpe that compares returns per unit of risk by dividing excess performance over the risk free rate (cash or t-bills) by the investment’s volatility (standard deviation).

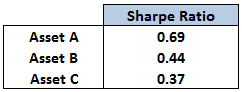

Take a look at this data on three different investments ranked by their Sharpe Ratios:

These results are based on the return history of actual mutual funds. Using risk-adjusted returns alone, you would choose Asset A in this case because it has the highest Sharpe Ratio.

Now here are the same three investments from the Sharpe Ratios listed above with actual performance numbers, volatility and the growth of investment dollars since 1993:

As you can see, basing an investment decision exclusively on the risk-adjusted returns could turn out to be problematic if volatility isn’t the only risk factor that matters for a given investment.

The only reason the Vanguard Total Bond Fund has the highest Sharpe Ratio is that fixed income funds have much lower volatility than equities. But that lower volatility comes with lower returns.

Although this data doesn’t go all the way back to the early 1980s the Sharpe Ratios are similar for large and small cap stocks. Yet the performance numbers and ending balances aren’t even close.

When comparing different asset classes or types of investments it’s difficult to see how the Sharpe Ratio can be relevant to average investors. It would be hard to explain to an investor that they should be indifferent to large or small-cap stocks based on the risk-adjusted returns over this 20+ year period when looking at the growth of a $10,000 investment.

Risk-adjusted returns are mainly used by academics and quant funds when comparing historical simulations. Certain strategies are able to create very low volatility returns using leverage so there has to be an understanding of the structure of the volatility as well.

It all depends on your definition of risk. Volatility isn’t a one-way street. It works on both the downside and the upside as many investors that missed the huge rally have found out the hard way over the past five years. Investors really only care about downside volatility (aka losing money). Unfortunately, it’s difficult to get upside volatility without downside volatility.

There are other ratios that capture losses only such as downside deviation or the upside/downside capture ratio. Luckily, investors aren’t forced to choose between asset classes based on risk-adjusted measures.

What really matters is how each investment is used within the framework of a total portfolio structure. Individual volatilities aren’t as important as how they’re paired together and what the returns are for the overall portfolio. This is why most investors use large caps, small caps and bonds together, regardless of their Sharpe Ratios.

There’s never going to be a single variable investors can use to choose between two or more securities, funds or asset classes. They’re all backward-looking and tell us nothing about the future risk premium.

There’s no formula or ratio that’s going to be the ultimate determining factor that provides a yes or no answer. When formulas are used in this manner they only end up creating a false sense of precision. If only there was a way to measure future risks.

As with all forms of performance or risk measurement, the best we can do is use them to consider potential or expected risks and rewards.

Source:

Finding smart beta in the factor zoo (Research Affiliates)

[…] Risk-Adjusted Returns Matter? […]

Ben,

Once again, you’ve nailed it with more great articles since our last correspondence a few weeks ago.

Question: Would you consider allowing one of your articles to be published in our quarterly newsletter that I’m about to re-launch in conjunction with our new website. Many of the subjects you cover are in many ways “timeless” — just like this one on risk-adjusted returns. I have felt the same way about this for years, but you have captured the essence of why you can’t build portfolios that way.

Of course we would list you as a guest contributor & give you full credit for any articles we re=publish in our newsletter. I’m guessing it would bring a whole new group of followers to your blog. We currently have 2527 subscribers, but the newsletter would be going out in the pilot/flight attendant lounges at Delta Air Lines — 12,000 pilots and 20,000 flight attendants.

I am only reaching out to you & Josh Brown with the same request. In my opinion, you both are leading the pack with your choice of content and writing styles that I think are most attractive to most readers/investors.

Let me know what you think.

Respectfully, Mike Stark

(770) 977-2434 Office

(678) 480-0441 Cell

Thanks Mike. Shoot me an email on this.

[…] No single measure of risk tells us all that much about our investments. (A Wealth of Common Sense) […]

When I first started tracking my dividend growth portfolio it had only 14 stocks and still had a higher Sharpe ratio than the 62-stock ETF benchmark that I was comparing it to. My takeaway was, I don’t really understand the Sharpe ratio and how it applies to my individual portfolio.

It all depends on your definition of risk. But it needs to be an apples to apples comparison and even then it might not tell you very much.

Hi Ben,

(Another) great post re Sharpe Ratio.

For risk-averse investors I focus on the fund’s lowest COV – is there a significant difference with this method instead of using Sharpe?

“I believe in a reasonable rate of return” (Le Chiffre, Casino Royale)

best,

DDH

Remind me what the COV is…

Hi Ben,

Sorry. Coefficient of Variation (CV)

CV = standard deviation/expected return

“CV allows you to determine how much volatility (risk) you are assuming in comparison to the amount of return you can expect from your investment – the lower the ratio of standard deviation to mean return, the better you risk-return tradeoff. ”

best,

DDH

Gotcha. Yes, this makes sense to me as we all build portfolios in this way in one form or another by using implied volatilities in stocks, bonds and other investments.

This is why diversification is so powerful because putting together a handful of investments, all with different vols, can actually reduce overall portfolio vol.

[…] Do Risk-Adjusted Returns Matter? (A Wealth of Common Sense) • Swedroe: Is The S&P 500 Actively Managed? (ETF.com) • Yields on 10-Year Treasuries […]

[…] Monetary Equivalent to Schrödinger’s Cat (Alhambra) Do Risk-Adjusted Returns Matter? (A Wealth of Common Sense) Taxes don’t lie (Scott Grannis) The Bottom Line by Carl Icahn (Yahoo Finance) 50 Million New […]

[…] Are Risk-Adjusted Returns Helpful for Building a Portfolio? from Ben Carlson […]

[…] Do risk-adjusted returns matter? – A Wealth of Common Sense […]

[…] Do danger-adjusted returns matter? – A Wealth of Common Sense […]

[…] Do Risk-Adjusted Returns Matter? […]

[…] Further Reading: The Lollapalooza Effect in Active Management Do Risk-Adjusted Returns Matter? […]

[…] Further Reading: The Lollapalooza Effect in Active Management Do Risk-Adjusted Returns Matter? […]

[…] John Maynard Keynes’s investment performance for King’s College (which includes the Great Depression & WWII) Do Risk-Adjusted Returns Matter? […]

[…] Further Reading:The Lollapalooza Effect in Active ManagementDo Risk-Adjusted Returns Matter? […]

[…] John Maynard Keynes’s investment performance for King’s College (which includes the Great Depression & WWII) Do Risk-Adjusted Returns Matter? […]

I agree. Risk adjusted returns have limited value in general. After all you can only eat returns, not risk adjusted returns.

Exactly. Maybe they can be helpful when comparing to very similar funds or investments but using risk-adjusted returns alone as the deciding factor is not a great idea.

[…] Reading: Do Risk-Adjusted Returns Matter? Two Finance Phrases I Could Do […]