Investors have had plenty to deal with since 1999: the technology bust, a real estate crash, failing banks, a weak economy, the near-collapse of the European Union, endless doom and gloom talk of “geopolitical risk” and the usual market fluctuations.

Yet from 1999 to 2013, the Wilshire Small Cap Value Index was still up a total of 371% or 10.9% a year over that time. In comparison the S&P 500 was up just 97% in total or 4.6% per year.

The academic research on the small cap value premium is fairly well-known in investment circles at this point. The theory is that the riskier smaller companies which trade at lower valuations will tend to outperform the broader market over the long-term.

The evidence of the small cap value premium is clear looking back at historical returns, but it’s not always easy to earn those returns. This is the whole point of a risk premium. Riskier stocks should reward investors with higher performance over time, but it comes at the cost of long periods of lagging returns.

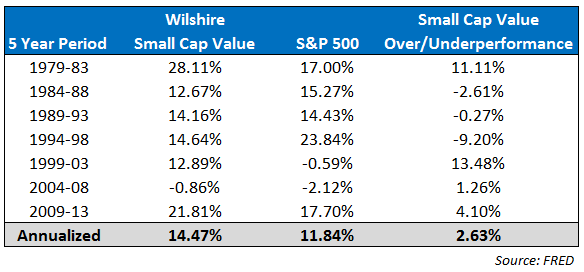

Here’s the annual return data in five year increments going back to 1979:

The performance numbers show the small cap value premium was strong over this 35 year period, but it didn’t happen like clockwork. You can see the swings in over and underperformance throughout the different periods. SCV owned the 1979-83 five year period, but from 1984 to 1998 large cap stocks delivered a total return of 1063% while small cap value returned 597%. The S&P 500 outperformed by 4% per year over that stretch.

Basically the outperformance by large cap stocks in that 15 year period is the reason small caps have done so well ever since. This is how it works in these markets. One asset class shows significant outperformance, investors end up chasing those high returns even higher, which causes an overshoot that makes them too expensive, thus leading to future underperformance.

It works the opposite way for the underperforming asset class as mean reversion is a powerful force in the broader markets.

The biggest growth stocks in the S&P 500 were in high demand by the end of the 1990s as valuation multiples moved into the stratosphere. This paved the way for the small cap value dominance ever since.

Of course the pendulum has now swung in the opposite direction as small caps are now looking a bit stretched. This has led to the huge rollout of smart beta funds in recent years. Smart beta is basically small and mid cap value but with higher fees. These factor investing strategies can work but not always.

Factor investing requires discipline when it’s not working so you don’t bail out at the wrong time. The biggest risks involved in these types of strategies come from investors try to pinpoint the big moves before they happen and go all-in or all-out of an asset class.

I’ve been hearing intelligent investors make the case for high-quality large cap stocks in favor of small caps since early 2010. Large caps stocks have performed fairly well over that time, but on a relative basis, small caps have continued to dominate. This can’t last forever.

If you’ve completely missed out on the stellar small cap returns over the past 15 years or so, now is probably not the time to pile into the space. You don’t want to get into the habit of timing these moves as it’s impossible to predict which corners of the market will perform the best over the next few years. This is especially true if you let recent returns dictate your decisions by chasing performance.

Most investors will be better off choosing a reasonable allocation they cal live with to riskier sectors like small caps and periodically rebalancing.

That means, on a relative basis, selling small caps to buy large cap or international stocks that haven’t done quite as well would make sense to control for risk if you haven’t done so already. Small cap value could continue to outperform if the animal spirits really take over but eventually these cycles run their course.

As always, sticking with a long-term asset allocation plan is a much better option than trying to precisely time these asset class moves.

Further Reading:

You Should Hate Some of Your Investments

A Lesson in Diversification and Regret Minimization

[…] Small Caps […]

[…] going to borrow from a recent piece from Ben Carlson at A Wealth of Common Sense titled “The Small Cap Value Cycle.” In it, Ben dives into the outperformance of small cap value strategies over […]

[…] we’ve discussed previously, value investing has been shown to outperform over longer cycles historically. Here’s a nice […]

[…] small cap stocks don’t always outperform (see The Small Cap Value Cycle), this example is a nice illustration of the risk-reward relationship we would expect to see in […]