“By choosing to place asset allocation at the center of the investment process, investors ground the decision-making framework on the stable foundation of long-term policy actions. Focus on asset allocation relegates market timing and security selection decisions to the background, reducing the degree to which investment results depend on mercurial, unreliable factors. Selecting the asset classes for a portfolio constitutes a critically important set of decisions, contributing in large measure to a portfolio’s success or failure. Identifying appropriate asset classes requires focus on functional characteristics, considering potential to deliver returns and to mitigate portfolio risk. Commitment to an equity bias enhances returns, while pursuit of diversification reduces risks. Thoughtful, deliberate focus on asset allocation dominates the agenda of long-term investors.”

– David Swensen

Asset allocation, the way you split your funds into different asset classes (stocks, bonds, cash, etc.), is one of the most important decisions that you can make with your investments. After you determine how much work you really want to put into your portfolio, you need to look at some historical allocations to determine what weights you should assign each asset class. Even if historical results don’t give you all the answers on how investments will perform in the future, they can be a useful framework for determining your risk profile and time horizon.

Long-term investing seems to be a thing of the past and shorter term attention spans are affecting the investment markets more and more each year. In a short time frame (since the year 2000) we have been through two recessions and had two separate drops of over 50% in the stock market from peak to trough. One of the few positives about this situation is that we have had numerous cycles with which to test out our tolerance for losses.

A great way to gauge your tolerance for risk and losses is to stress test your portfolio to see how it would have performed through a number of scenarios. By looking at the performance of certain asset allocation strategies you can determine how the losses and gains over these cycles would have made you feel. You can get a better handle on your emotions and investment decisions if similar circumstances arise in the future.

For investors under the age of 45, a rule of thumb in the past has been that a portfolio made up of 80-90% in stocks and 10-20% in bonds is an ideal mix. In this case, you have a long time until retirement and can usually make up for short-term volatility in the stock market while still getting the long-term returns that you need.

Someone that is approaching or in retirement is more likely to have a 50/50 mix of stocks and bonds in their portfolio because they have current and future spending needs and must draw down their investment funds for that spending. Having a higher weighting in bonds and a lower weighting in stocks has, in the past, lowered the volatility in your portfolio while also providing some downside protection against large losses.

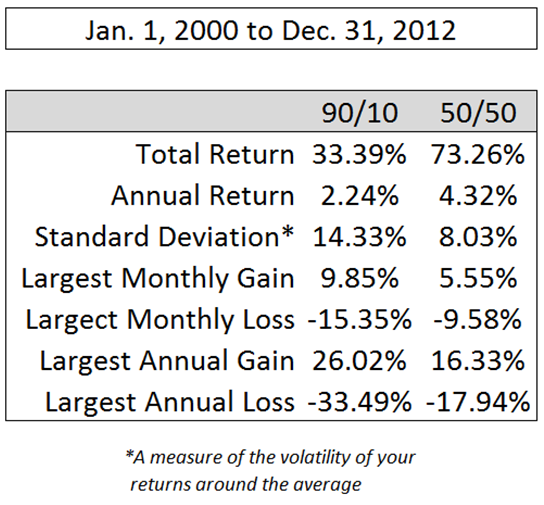

So on one end of the risk spectrum we have a 90/10 portfolio and on the other end we have a 50/50 portfolio. It should be helpful to determine your tolerance for risk by looking at how these portfolios have performed in the recent cycles and over the long-term. Let’s take a look at how a portfolio with a 90% weighting in stocks and a 10% weighting in bonds performed in the boom and bust period from January 1, 2000, until December 31, 2012.

For the stock portion let’s use the S&P 500 since it tracks the largest, most liquid stocks in the market and is right in line with the overall stock market in the U.S. The bond portion will be tracking the Barclays Capital Aggregate Bond Index which is a good proxy for the entire U.S. bond market. It is made up of government, corporate and mortgage bond securities. Here are some statistics on how those two strategies look against each other going back to the year 2000:

As you can see the 50/50 mix has actually outperformed the 90/10 mix over this time frame. The returns are higher and the volatility (as measured by the standard deviation of returns) is lower. A $10,000 investment on January 1, 2000, would have been worth $13,339 with the 90/10 mix by the end of 2012 and $17,326 for the 50/50 mix. The gains are larger when the markets take off for the 90/10 allocation but the losses are smaller for the 50/50 mix when things fall apart.

Granted, there have been two drawdowns of over 50% in equities in that time frame so you would expect bonds to outperform, but this is still a good exercise to see how things worked out in a tough investing environment.

Now let’s go back even further to see how these asset allocations would have performed on a longer term basis going back to 1990. Again, here are the same relevant statistics:

This time the 90/10 mix outperforms, but only slightly. The volatility is still lower for the 50/50 selection again with lower gains in the up years but smaller losses in down markets. A $10,000 investment on January 1, 1990, would have been worth $65,239 by the end of 2012 for the 90/10 split and $59,116 for the 50/50 split.

Going back even further the historical annual returns for stocks from 1928 until 2012 were 9.31% per year. Bonds came in at 5.10% per year. No one knows what the returns for these asset classes will be in the future but looking at their historical track records can give you a sense of how they have performed over difference market cycles in the past.

What conclusions can you take away from these numbers? The longer your investment horizon the higher your returns have been in the stock market. But over shorter time frames bonds actually can outperform stocks. Adding bonds to your portfolio can dampen your volatility and lower your losses in down markets. The closer you are to retirement, the higher your allocation should be to bonds to avoid the possibility of large losses. If you can’t stomach the risk of the higher potential losses in stocks, lower the amount you have in stocks and increase your allocation to bonds.

Remember that the goal is not to have the very best asset allocation that will outperform all others. No one knows what that will be going forward. You want to choose the one that has worked well over various scenarios and will help you sleep at night without stressing over your portfolio.

Start with the baseline of a 90/10 mix as being high-risk tolerance and 50/50 for low-risk tolerance. If you can think really long term and don’t mind taking larger losses then you should be comfortable being closer to the 90/10 allocation. Just move closer to 50/50 as you age and get closer to retirement.

But if you aren’t comfortable seeing large losses in your portfolio lower the amount you have in stocks and get closer to the 50/50 mix right now. You could try 80/20, 70/30, 60/40 or any combination in-between. Find the one that fits your risk tolerance and time horizon.

This is a simplified example of just two broad domestic asset classes. Once you make the common sense decision about how you are going to allocate your money between stocks and bonds you can get more creative with your investments if you would like to be more hands-on with them.

In your stock allocation, you could add small-cap, mid-cap, international, emerging markets, REITs or many other varieties of sectors and styles. Within your bond weighting, you can add treasuries, high yield, international, emerging markets or even safer investments like money markets or a stable value fund.

If you don’t want to micromanage your investments, keep it simple and stick with the broad indexes that I used in my examples. You could do much worse than those two options. This list of strategies at MartketWatch also has the common sense stamp of approval if you would like to see some other choices: Lazy Portfolios. Only get more complex if you have the time and motivation to do your homework.

Everyone’s situation is different. There is no one-size fits all asset allocation for each investor. You have to take into consideration many factors like your job security, future earnings power and the amount of time you have to save until you retire to come up with the correct mix that works for you.

This exercise should give you a better idea on the amount of risk you are willing to take with your investments and will help you better synch that risk with your time horizon. Get these two factors right and you have taken care of one of the single biggest determinants of your future investment performance. Simply rebalance back to your target weights once or twice a year to keep yourself honest and within your risk parameters and you have an investment portfolio tailored to your specific situation. Rebalancing your portfolio is one of the best the best moves you can make in your investment plan because it forces you to sell some of what’s expensive and buy some of what’s cheap.

*The quote at the top of this post comes from the book Pioneering Portfolio Management. David Swensen is one of the greatest investors of all time, generating annual returns in the range of 15% annually for over 2 decades with the Yale Endowment Fund. He credits asset allocation decisions for much of that success.

[…] off setting up a simple common sense investment plan that focuses on your strategic goals with an asset allocation process at the center of that […]

[…] You Do Control – Asset Allocation: This is most important investment decision you can make. It helps shape the risk profile & time horizon of your investments. You can really learn who you are as an investor through your asset allocation (hopes, fears, biases, tolerance for loss, psychology). Learn more about how to spread out your mix of investments between stocks, bonds, cash and alternatives here. […]

[…] with your desired asset allocation mix (read more about setting up your asset allocation here and here). I would advise that you do this at least annually but monthly, quarterly or semi-annually would […]

[…] being risk averse and a 100% stock allocation as being very aggressive on the risk spectrum (read here to see how these strategies have performed over time). You can then make changes to your allocation […]

[…] disciplined investment process that includes periodic rebalancing to a well thought out asset allocation reduces your risks even […]

[…] is a natural extension of a well-balanced asset allocation plan. There is no reason to set your mix of assets with a defined risk profile and time horizon if […]

[…] is why setting the correct asset allocation for your risk profile and time horizon is so important. Asset allocation is worthless if you are […]